This will be the fastest demand collapse in U.S. history...

"The economy is very strong and inflationary pressures are high, and it is therefore appropriate in my view to consider wrapping up the taper of our asset purchases, which we actually announced at the November meeting, perhaps a few months sooner,” Powell said in testimony before the Senate Banking Committee.

In a sign that elevated inflation could persistent for longer than expected, Powell conceded that it was “good time to retire that word [transitory].”

I was wondering today how many GOP Senators pounding the table for a tighter Fed right now are about to get wiped off the map financially? All of them. And the other side of the aisle won't be spared either.

Which raises the question, how DO we measure success under this form of casual fraud? I suggest this will be a Pyrrhic victory.

To be sure, Zerohedge is the Jim Cramer of financial blogs. They are ad-sponsored entertainment and they reserve the right to change their mind with every trading day to ensure they are always "right". They are not per se "macro tourists", they are macro tour operators, because why pay for the ride when you can be the one leading it?

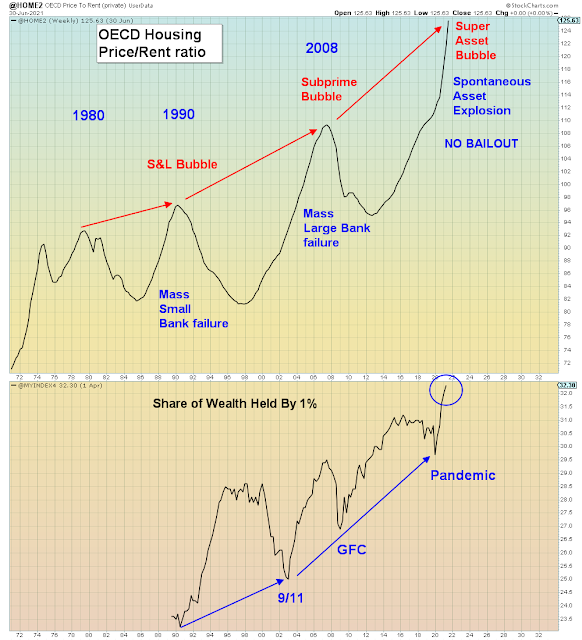

Unfortunately, this type of casual deception is now commonplace across the financial culture due to the fact that capitulating to this tsunami-magnitude mega bubble and ignoring risk is by far the most lucrative path forward. Which unfortunately leaves the sheeple ONCE AGAIN at the mercy of known con men. History will say that in the year Bernie Madoff died, the sheeple having been skeptical of markets since 2008 then crammed two decades worth of cash into stocks at the end of the cycle. Proving that in 2008 policy-makers took down Madoff's petty theft while bailing out the much bigger crime. The magnitude of which will now be revealed in biblical fashion to a society assiduously ignoring "corruption as usual".

Not only is inflation transitory, but all real-time indicators show that it has already peaked and is very quickly receding. The CPI that so many bloggers today refer to is stale data, weeks and months old. There are several indicators that track much more closely to inflationary trends.

First and foremost is Treasury inflation expectations themselves.

These have already peaked and they are starting to head in the direction of EM currencies which are collapsing like a cheap tent.

Pundits appear to forget that it was EM currency collapse - led by China that caused the Fed to pause their tightening campaign in September 2015. Then they raised rates in December and exploded global markets.

Here we see Brent Crude is deja vu of Q4 2018. Earlier on Twitter I showed Nat Gas getting monkey hammered the most since December 2018. This is the longest weekly losing streak for Brent since December 2018.

And why is December 2018 important? Because that is the last time Powell was forced to reverse policy and stop tightening because markets were imploding.

He will ultimately be forced to do the same thing all over again, but today's events just doomed bulls trapped in the casino unknowingly.

The correlation between oil and inflation is lock tight:

Here we see Gold / CPI. Is this a good time to buy?

According to those who believe in inflation...

YES it is!

The Baltic Dry Index is another leading indicator of inflation.

We just got news that Black Friday in-store sales were down -28% versus pre-pandemic and we also got news that online sales for Cyber Monday fell for the first time in history.

Which means it's becoming clear that the consumption orgy that fed back into inflation via the fake wealth effect, was merely demand pulled forward at the behest of con men looking to make sales.

Consumer sentiment has only one way to go.

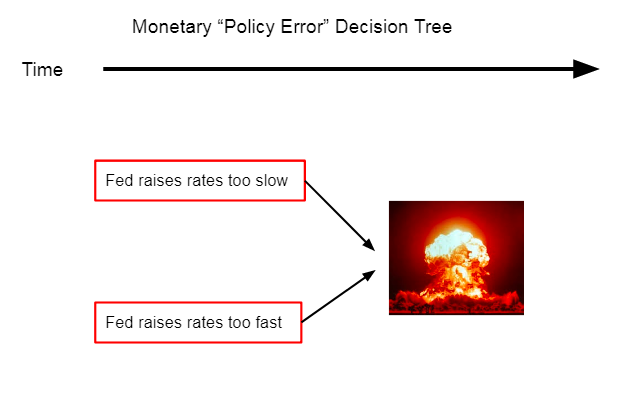

In summary, the Fed and the majority of consensus pundits were wrong last time when it hurt the most. The question is will their strength in numbers come through for them this time?

Or, will the sheeple FINALLY learn that the REAL policy error is trusting proven psychopaths.

"The transcript for that meeting contains 129 mentions of “inflation” and five of “recession.”