Those who know their history know that the U.S. Navy was on high alert for imminent attack in the days before the Pearl Harbor attack. Which is considered one of the greatest Black Swan events in history. But, the Navy didn't expect the attack in Hawaii they expected it in Indonesia. Similarly, during the lead up to the 2020 pandemic, global markets melted up even as the pandemic grew larger and more lethal in scale. At the beginning it was a RISK ON event.

Complacency reigned supreme:

Rewind to February 26th, 2020:

Via Emerging Markets, we can see that where Suze Orman said to rejoice at the buying opportunity was that first dip down ~10%. Which was followed by a three day oversold rally and then explosion lower. Whether that sequence repeats again remains to be seen. This market is so far still significantly overbought.

As of this past week, the Nasdaq was enjoying its biggest January up month since 2001. Which happened to be the beginning of the post-Y2K recession.

This is a headline from TODAY:

"Traders are rushing to profit from the January rally in the stock market, sending call options trading to one of the highest levels ever. More than 33 million calls changed hands on Friday, the fourth-highest level on record"

The Nasdaq VIX shows there is not even the slightest sign of fear in this market. The volatility algos are working overtime to monetize put options and otherwise prevent a RISK OFF event.

In order to be a true contrarian investor and survive the entire economic cycle, one must be able to endure times like these when the herd is stampeding off a cliff. I can tell from my Twitter stats, that many bears capitulated in January and joined the stampeding bulls. That's what happens at the end.

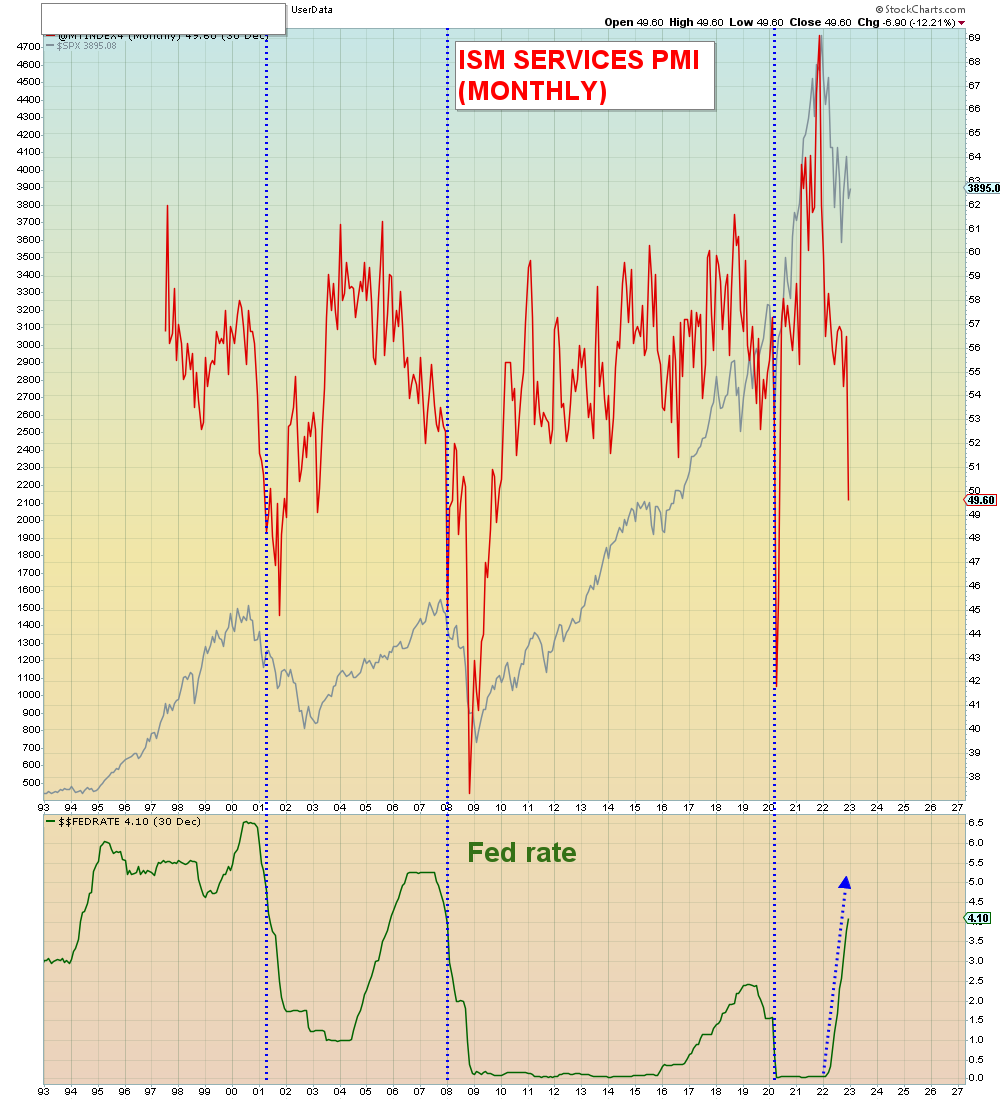

In the lower pane below, we see the the Nasdaq Market Thrust , which equals (Nasdaq advances * advancing volume) - (declines * declining volume). Basically it shows the amount of buying or selling pressure.

This level of speculation has only been seen three times in the past decade. February 2021. March 2022. And now. The last time it was this high (March 2022), the Nasdaq fell straight down to the 200 week moving average. Where the Nasdaq is now.

"Earnings from high-profile technology companies last week ranged from uninspiring to downright disastrous. But that didn’t stop traders from scooping up tech stocks ahead of more potential land mines"

Almost everywhere you look in the stock market, fear is vanishing"

Which gets us to option skew, which measures investor fear:

"The October 1987 crash sensitized the market to the possibility of large downwards jumps in the S&P 500. The distribution of S&P 500 log-returns (“S&P 500 distribution”) is unlikely to be normal if there are large jumps in returns. Jumps fatten the weights of the tails and asymmetric jumps skew the distribution. The standard deviation of returns is then insufficient to characterize risk and the probability of returns two or three standard deviations below the mean is not negligible, as it is under a normal distribution"

To paraphrase, in English - crashes are far more common than a normal aka. random distribution would have us believe. However, recall that in "Fooled By Randomness" when Nassim Taleb introduces the Black Swan event he calls it a RANDOM event. Hence the name of the book. However, the problem is that as the CBOE admits, crashes are NOT random. They are highly correlated to WELL KNOWN risk factors such as over-valuation, interest rates, positioning, lack of hedging, and SPECULATION. In the Minsky Hypothesis, crashes are inevitable and usually caused by monetary tightening in an inflationary economy such as the one we are in right now:

"Over a protracted period of good times, capitalist economies tend to move from a financial structure dominated by hedge finance units to a structure in which there is large weight to units engaged in speculative and Ponzi finance. Furthermore, if an economy with a sizeable body of speculative financial units is in an inflationary state, and the authorities attempt to exorcise inflation by monetary constraint, then speculative units will become Ponzi units and the net worth of previously Ponzi units will quickly evaporate. Consequently, units with cash flow shortfalls will be forced to try to make position by selling out position. This is likely to lead to a collapse of asset values"

Be that as it may, hedging is expensive. And under Wall Street's heads I win, tails you lose, no one hedges anymore. Why would they, when they have the "Fed put". Under today's bullish hyper fantasy, the Fed can both implode markets AND then rescue markets at the same time. Like a baseball pitcher catching his own pitch.

Here we see option skew was very high at the stock market's all time high, but subsequently it has collapsed as hedge funds monetized their hedges. In other words, they don't use hedges for hedging they use them to generate income. Which means when they see fat premiums they sell into it. Similar to how hedge funds were selling subprime CDS contracts in the burgeoning risk of 2008.

In summary, this event will be highly predictable but highly unpredicted. The herd is currently stampeding into risk and skeptics have been getting run over. All that means is that there will be far more carnage on the other side of this unforeseen collapse. The problem of course is that the RISK OFF "event" is invisible right up until it takes place. Hence, it is subject to plausible deniability of the likes we are witnessing right now.

Few people will see this coming, and far fewer will be positioned for it. Therefore we should expect SERIOUS dislocation.