The bullish thesis is that all younger people will get wiped out due to their misallocation of capital, to the sole benefit of older generations doubling down on their Ponzi investments. In other words, no generation in U.S. history has been fooled as often as this one...

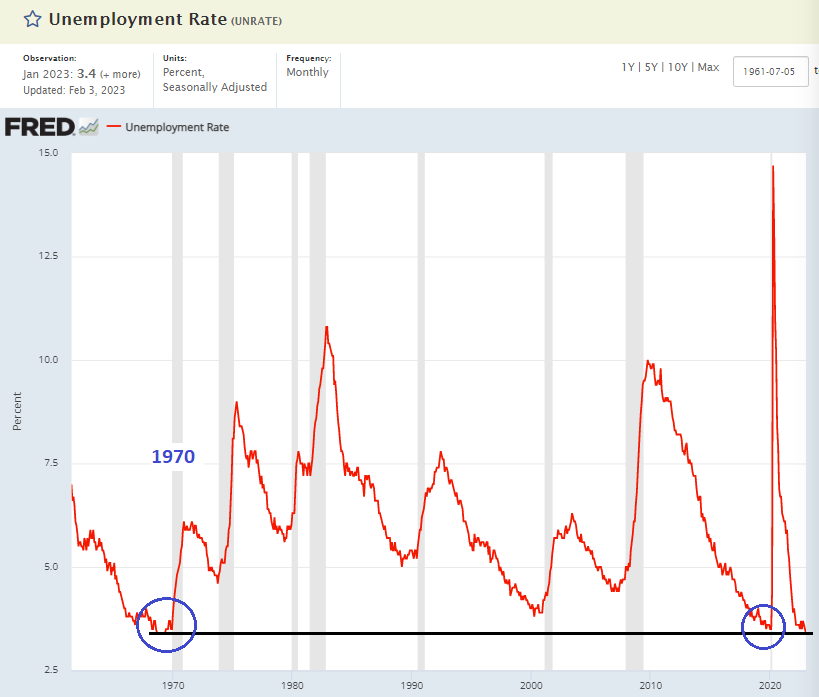

It took ~15 years but over time retail investors have totally forgotten the pain of 2008. After the 1930s, the generations that endured that pain NEVER forgot, even decades later.

Today's financial media is wholly derelict in their duties, as they have been for decades amid an ever-growing debt bubble heading for inevitable disaster. The individual investor has now been throw to the wolves of Wall Street. What was Occupy Wall Street a decade ago is now trust the fairy tale of the never-ending financial/economic cycle - the belief that the pandemic bear market lasting one month corrected the longest bull market in history.

Below is what the ratio of bull market to bear market would look like if that were actually true. The 2009-2020 bull market would be ~130x longer in months than the bear market that followed:

Gen-Z is now totally under the bus. Two years ago the Gamestop pump and dump frenzy brought record newbies into the market where they were unceremoniously obliterated.

The media called it "The democratization of markets". They even made a Netflix documentary about it called "Eat the Rich". It turns out the rich were not the ones who got eaten. It was a totally false narrative and yet largely unquestioned.

Millennial investors are in the 30-45 age range and they are now trapped in the housing market. They didn't believe all of the stories that emanated from 2008 about the risk of housing bubbles, so they went ahead and made the same mistake a mere 10 years later.

So far, global housing prices - with some regional exceptions - are holding up, but sales volumes have collapsed. A precursor to major price decline.

Soon the combined impact of $2 trillion student loan debt, epic housing collapse, stock market wipeout and mass layoffs will land on them like a ton of bricks.

The good news is that younger people who get wiped out by this global Ponzi collapse can recover from this debacle and eventually get themselves back on track financially. Time is on their side. The older generations who SHOULD know better than to trust Ponzi markets, don't have that kind of time.

So far retirement gamblers are doing the exact same thing GEN-Z dunces did - they are "HODLING" meaning holding on with the belief that markets will come back. They look around and see other generations making the exact same mistakes they made in Y2K and 2008 and just assume they alone will be spared the consequences of the pandemic bubble.

Which is where it gets interesting:

As things go on the domestic side of markets - a case of survivor bias, so it is on the global markets. A massive case of survivor bias. There is this recurring false belief that U.S. markets are a safe haven from global dislocation.

Global central bank tightening has been collapsing Emerging Markets since 2021 while capital retreats to the safety of the U.S. The belief is that they will continue to implode to the benefit of the U.S. We saw this same cycle play out between 2018 and 2020. And it all imploded in this EXACT same timeframe.

It's the "It can't happen to me" trade on a global scale:

Ironically, just as the financial media were lying to newbie investors two years ago during the Gamestop debacle, so too are they lying to older investors right now.

Why? Because in the end media bulls and Wall Street analysts will be spared the consequences of their specious advice.

But, at some point it's not the liar who is the problem, it's the person willing to believe the liar who is the real problem.

Who benefited from this pandemic?