Panic buying in autos, homes, durable goods, commodities, cryptos, and Tech stonks is the overwhelming cause of today's "inflation". It's called the trickle down fake wealth effect and that premium is going to come out of markets via margin call.

Lower prices are coming, and when they do liabilities will exceed assets and the sheeple will quickly realize they are bankrupt. At that point EVERYONE will understand the difference between inflation and deflation, however that lesson will have arrived 40 years too late...

This week the money printing cargo cult is going late stage euphoric on news that their Kool-Aid serving cult leader Jerome Powell has been re-nominated to lead money printing operations. On the one hand they embrace everything he does for them in casino markets, on the other hand they excoriate him constantly for economic inflation. You can't turn on the TV or radio these days without hearing about the "inflation" crisis. These people are plowing their life savings into the most overbought and overvalued asset markets in human history and yet all you hear about is the price of eggs going up 50 cents.

No question, at the bottom of the wage scale, a combination of factors have made even relatively small price increases seem insurmountable. However, maybe it's time to consider the fact that working wages have been suppressed by mass outsourcing and mass immigration for forty years straight. As I showed in my last post, wages are going up the LEAST of all other types of prices. Which in aggregate is deflationary.

Now we learn that Biden is following Trump's (mistaken) lead in releasing oil from the Strategic Petroleum Reserve. Which is ironic, because it's highly likely that oil prices have already peaked. Any blind man can see below that oil is far lower today than it was in 2014, 2011, and 2008, none of which times oil was released from the SPR. Meanwhile, Trump released oil from the SPR in September 2019 which was only a few months before oil crashed the most in history - going negative in April 2020. I predict that will very likely happen again.

More importantly, note that oil demand is STILL only at 2013 levels (lower pane).

Brent crude was down five week straight as of last week, which is the longest losing streak since March 2020 and before that Q4 2018. So far this week, it's bid as of Tuesday close.

So far, the Q4 2018 analog continues to loom large. Back then fiscal AND monetary stimulus were waning and global markets were rolling over.

This chart shows BOTH India and China getting in synch to the downside.

This chart shows that through Monday, there were five Nasdaq Hindenburg Omens in a row, which is the most since Q4 2018.

Yesterday, new lows at an all time high (lower pane) set a new record going back to 1978:

Here is Nasdaq breadth relative to Q4 2018:

How's that for bullish?

Of course this implosion will make Q4 2018 seem like a good time by comparison.

Why? Because three years ago, positioning was cautious compared to today's absolute faith in printed money.

In summary, the cure for higher prices is coming. However, I suggest that most people won't be in a position to take advantage of them when they arrive.

Here we see that the U.S. aggregate bond index is highly correlated to Chinese risk assets:

Which makes THIS is a far more relevant Q4 analog:

Momentum is building towards the day of reckoning. The magnitude of fraud in this era dwarfs any other period in history since 1929. It's clear that the Casino class is fully euthanized by the virtual simulation of prosperity and its acolyte QE. And so it is apropos in the year of Madoff that Michael Burry of "The Big Short" fame has just now capitulated. Whereas in 2008 waiting for subprime to explode he had adequate patience, this time around, history's largest bubble forced him to submit to central bank obeyance. The ultimate irony would be if THIS is the top...

Two Hindenburg Omens on the Nasdaq in the past week as new lows are accelerating each day. Today was the second highest number of new lows attending an all time high in Nasdaq history going back to 1978. The highest number (so far) was in July of this year.

I've been pounding the table recently on this Ponzi reflation theme. Retail sales out today indicate there is no way to explain this level of consumption based upon wage gains alone. It's clear that the fake wealth effect is feeding back into the economy on an epic scale. That combined with "shortage" hysteria is creating a feedback loop of accelerating demand, which I call the Ponzi Hype Cycle. In order to understand this diagram first we must revisit the wealth effect:

"The wealth effect is a behavioral economic theory suggesting that people spend more as the value of their assets rise. The idea is that consumers feel more financially secure and confident about their wealth when their homes or investment portfolios increase in value. They are made to feel richer, even if their income and fixed costs are the same as before"

The central banks create the bubble, the bubble creates the wealth effect, wealth-driven consumption inflates earnings, and inflated earnings accelerate the stock rally. THIS is what is driving today's "inflation":

This chart I created indicates that wages in no way explain the level of super-normal spending taking place right now. Everything is up across the board, EXCEPT wages, which are up the LEAST and below the rate of CPI.

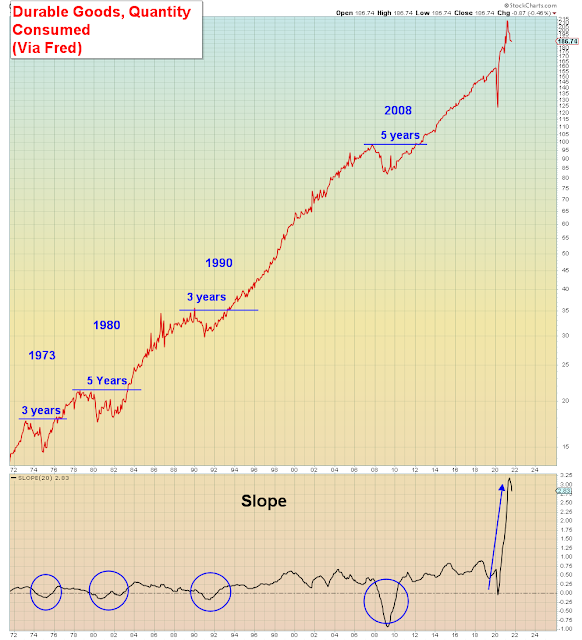

We now have simultaneous pull forward in demand across retail sales, durable goods, housing, autos, and technology. ALL at the same time.

It gets worse.

Economic opportunism and inflation hysteria has triggered panic buying and thereby pulled forward consumption from 2022 into this fourth quarter. Consumers have been told to expect "shortages" during the holidays, and they have responded by panic buying. Ironically, they have made shortages a self-fulfilling prophecy. Which is a disaster waiting to happen.

One would think that economists would realize that wages in no way explain this level of consumption, but they don't. Instead they are wed to their traditional models which link the unemployment rate to the level of inflation. Due to the high level of long-term unemployed following the pandemic, the official (U3) unemployment rate is artificially low right now. In addition, the combined effects of mass outsourcing, mass immigration, and mass automation have lowered capacity utilization to all time lows for this point in the cycle. While the trade deficit is record wide.

Meanwhile, the collapse in consumer sentiment taking place in broad daylight has been assiduously ignored. Today's pundits are more interested in using stale economic data from last quarter than to look at what consumers are saying now.

Got that?

The outlook is bright, just as it was in 2007/2008. These people have a history of being wrong when it hurts the most, so why stop now?

In summary, this is now officially the Big Long.

Wall Street already has one foot out the door on this gong show vis-a-vis their "policy error" narrative. Meaning no matter what the Fed does, if it implodes they will just blame the Fed. Nevermind that this approach leaves their clients death trapped in the casino hoarding inflation trades.

There is no point in being overly academic at this juncture. The policy error was believing that printed money is the secret to effortless wealth. Binary outcomes that turn from extreme inflation to biblical deflation overnight are the domain of proven con men.

The common investment theme for 2021 is rampant fraud. Below I delineate the stocks/ETFs/sectors/assets that are most likely to implode the market. Any one of these alone would not likely be enough to create a meltdown, but if they all roll over at the same time the HFT algos masquerading as market makers will go critical mass. Today's pundits are sanguine because markets are at all time highs and the Dow/S&P in no way convey the risk that lurks beneath the surface. Whenever markets are going up, everything is bullish. But, what's the "catalyst" for meltdown? The catalyst is "Sell"...

First place of course goes to Tesla, EVs, green Energy and the entire auto sector, all of which are hyper overbought.

The melt-up started three weeks ago with Tesla's third quarter results which beat expectations (Oct. 20th). Then it got a boost when Hertz announced they were buying 100k Tesla's for their rental fleet (Oct. 25th). All of that sparked a Reddit-driven options "gamma squeeze", which is a short squeeze using call options. That melt-up in all things EV/Auto continued up until the COP26 conference this past week and the passing of the Clean-Energy infrastructure bill which gets signed tomorrow. In my opinion all of these catalysts are capping off a mega melt-up in Tesla that started two years ago in Fall 2019 and went parabolic during the pandemic.

If Tesla folds back below the blue line then this entire blow-off top is a bull trap that will get fugly. Note that the clean energy ETF is three wave corrective.

On a related subject, as I've shown many times the entire auto sector - including Ford, GM, Auto Nation, Car Max, and of course Avis is ludicrously overbought.

This is all driven by the "car shortage" fraudulent narrative:

Next, the semiconductor sector has also seen a late stage melt-up. The leading stock is Nvidia which is a heavy hitter in terms of market cap and daily dollar trading volume. Nevertheless, the entire sector is now massively overbought.

This sector has been melting up due to the "semiconductor shortage" false narrative. This era has seen record semi demand now conflated as a supply shortage. I also believe this to be the blow-off top phase of a decade long rally:

Also on the topic of Tech stocks, yesterday I showed a chart of "TRINQ" on Twitter indicating that there has been no RISK OFF in Tech for the past decade since the 2011 debt ceiling. Ironically, another debt ceiling debacle is only weeks away. That long-term chart is by no means a precise timing indicator.

Nevertheless, here we see Microsoft the most valuable company in the market right now is the most overbought since the Feb. '20 high:

Transports are also hyper-overbought. Some say it's because of Avis, but Railroads are at new all time highs and below we see the Trucking sector is parabolic. Meanwhile, I showed a chart on Twitter yesterday indicating that this is the largest coincident melt-up between Tech and Trucking since the January 2018 blow-off top.

No discussion of meltdown risk would be complete without a discussion of the $2.8 trillion crypto sector which now equals 2 x 2008 subprime in magnitude. Roughly half of that market cap consists of shitcoins which everyone KNOWS are pump and dump schemes.

The other half is Bitcoin which has now seen widespread adoption, institutional buying, and multiple ETFs. I showed a chart on Twitter yesterday indicating that Bitcoin is highly correlated to the NYSE Composite. And yet, these cryptos are all getting bought with both hands under the fraudulent "inflation hedge" hypothesis. If there is one asinine hypothesis that this society must live with for the rest of time, it's that one. And many other dumbfuck ideas these morons accept without question.

This article in National Affairs magazine argues that Bitcoin is safer than gold and should be considered by the U.S. Treasury. You can't make this shit up. I will not rebut the entire article because he includes some currency history which I happen to agree with, however, I will say that the author has never heard of Japan, their record deficits and record money printing and their currency which 30 years later is STILL viewed as the global safe haven. All due to the power of deflation which is about to get far worse before it gets better.

The main problem with Bitcoin is that it can't scale. It has the carbon footprint of Pakistan. Every Bitcoin transaction consumes $100 in electricity, even just buying a cup off coffee. Yes, you read that right:

For the record, the top performing sector year over year is the fossil fuel Energy sector. Ironically, these stocks languished under Trump who was pro-fossil fuel and then they sky-rocketed under Biden's green energy plan. Mostly of course due to the pandemic unlockdown. Year over year most Energy ETFs are up well over 100%. However, there are few if any Energy stocks at all time highs since they were the worst performing sector in 2020.

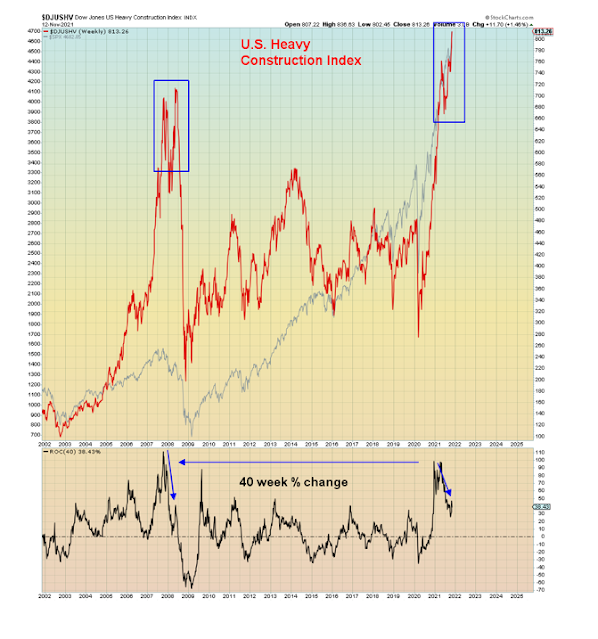

Therefore, instead of showing oil stocks I will show the construction/infrastructure sector which is the most overbought since the Fall of 2008:

Finally, I show the Nasdaq with breadth and down volume. The market is Jan. '18 overbought, breadth is the worst at an all time high in history. And as we see, down volume has been increasing with each selloff since 2018.

In summary, 2021 will forever be known as the year when fraud and criminality were "democratized" amid rampant cynicism, greed, and denial.

Capping off over a decade of non-stop monetary bailouts for the rich.

It's been a long time since I baselined my predictions and assumptions, therefore in this running post I will document my overall hypothesis towards the economy and markets. These assumptions and predictions are not bounded by any specific year/timeframe unless otherwise noted. Therefore I will continue to revisit and refine them over time. My use of charts will be sparse if any, since the goal is to document my underlying assumptions. If people don't want to believe them that's their decision. If it's one thing I've learned all these years it's that no amount of facts and data can overcome denial...

First off, it's already been a crazy year and it's not over yet. The second stage post-pandemic melt-up began a year ago when Joe Biden was elected. Year over year, the S&P is up 48%, which compares to Trump's 38% melt-up into late January 2018. Then as now, the pot of gold at the end of the rainbow was fiscal stimulus - tax cut v.s. infrastructure bill. The market is equally overbought now as it was at the end of Trump's rally. However, for most of Trump's rally the Fed was tightening short-term rates and QE, whereas for the past year the Fed has been pedal to the metal on both ends. They are just starting to taper this month and that will continue through May 2022 at -$15b reduction per month.

The Ameritrade IMX positioning indicator is equally RISK ON now as it was at the end of the Trump melt-up. Although it's been at the same extreme level now since July.

CHINA:

I believe China is the new Japan. They've had their supernova real estate melt-up and now they are morphing into a dwarf star emitting continuous deflation. Unlike Japan however, the Chinese government is making serious and painful reforms to their economy instead of merely relying on fiscal and monetary stimulus ad infinitum. So far only their stock market has imploded, but I believe it's only a matter of time before their property market explodes as well. Evergrande being the canary in the coalmine. I believe that China is leading the world towards what they are calling "Common prosperity". Which means that bailing out rich people is a thing of the past. China's nascent Evergrande response is to attempt to protect small investors and households while allowing their oligarchs to go under the bus.

Meanwhile, wealth inequality in the U.S. is reaching its zenith amid the largest global asset bubble in history. For now U.S. policy-makers are ignoring the political risk of this equation. It's only a matter of time before they follow China's lead.

GLOBAL REAL ESTATE:

I believe the global real estate super bubble is on the verge of final explosion. In each cycle it has grown larger and required more stimulus to bail it out. Nevertheless, in keeping with the "Common Prosperity" theme, I believe this crash will be sufficiently large to convince people enough is enough. Of course if I am right then there will be many more dominoes to fall as global central banks which are currently in the process of tightening, will be forced to reverse.

U.S. ECONOMY AND FED POLICY:

I doubt the Fed will ever increase rates in this cycle. They are now between a rock and a hard place. The lagged data is coming in hot, however consumer demand is likely on the verge of collapse. My deflationary hypothesis - as everyone knows - is that this post-pandemic consumption binge is end of cycle and it's obscuring economic weakness. The middle class is over-leveraged and recent wage gains are not keeping pace with prices. For the moment it's "stagflation" - stagnant economy with inflation. However, this is not an equilibrium state. It will soon morph into outright deflation amid asset collapse. The common belief that wages will spiral out of control is part of the Supply Side mythology that has held this country in a deathgrip since 1980. High debt, low employment, low capacity utilization, record trade deficit, and extreme overinvestment in technology are all structurally deflationary.

On the long end, the Fed will be forced to reverse their recent taper decision, but they will be (too) slow to react. Back in 2018 Trump forced the Fed to reverse. Biden won't intervene this time.

Bad news for bulls, Powell isn't going to stop mass margin calls.

U.S. FISCAL POLICY

No surprise, I view this gridlock in Washington as being deflationary. The economy is now dependent upon continuous and ongoing combined fiscal and monetary "GDP". Without both, it will collapse back into deflation. The parties are at ideological loggerheads, however, during crisis they usually come to some short-term agreement. And that's what it will take. Crisis.

STOCKS AND RISK ASSETS

In keeping with the theme of no bailouts, the pain in markets will be like nothing we've ever seen before. Most Millennials will be wiped out financially. Robinhood will be sued out of existence. Liquidity will be non-existent. Confidence in markets overall will collapse.

I predict that Tesla will lose 90% of its value, as will Bitcoin. The idea of a crypto Ponzi scheme being a safe haven from inflation is the height of asinine. Then again, we will never find out, because it's extremely highly correlated to stocks and other risk assets on the downside. These people are ALL looking the wrong way down the tracks for inflation, but the freight train of deflation is coming from the other direction. But it's only been 40 years straight of Supply Side economic failure, so how would they know?

My last prediction: The sun will still rise, life will go on.

This society now believes that printed money is the new El Dorado. Recessions and bear markets have been banished to the dustbin of history, replaced by consumption binges and effortless speculative profit. The only question is why didn't anyone try this sooner? What fools! Pundits are basing their current views of the economy upon recent widespread panic buying encouraged by ubiquitous industry pimps; which will be a swan dive into pavement when panic buying turns into panic selling...

Let's begin with this just ending climate conference COP26. The conference has just barely ended and yet people are already realizing that it was just another load of false promises. Which is more cynical, to NOT believe in man made climate change, or to believe in it but not do nothing about it? This climate conference is an analog for the global economy. It's a massive false promise for the future predicated upon the favoured approach of doing nothing. We have discovered the new El Dorado, printed money. Now featuring consumption orgies and speculative manias where there used to be recessions and bear markets. The only question today's pundits have is why didn't anyone think of this sooner? When the false promises around this consumption orgy explode, then the forced downsizing will do more to reduce carbon footprint than any ten bogus climate conferences.

Here we see the pandemic was the first recession in U.S. history in which consumption INCREASED:

But at least we know why the entire $Green energy sector has been on fire lately. Not only was there a climate conference, but also Biden's clean-energy infrastructure bill just passed, and the largest (EV) IPO of the year. ALL in the same week. And the world's richest man rang the cash register several times.

"KA-CHING!!!"

Recapping the economic situation - the pandemic caused a global supply shock which led to higher prices. The initial response was for demand to INCREASE especially for durable goods, cars, and houses. The question is what happens next? Inflationists believe we are in a wage-price spiral that will continue to drive prices higher until the Fed is forced to move or the bond market spontaneously implodes. However, if they are wrong, then we are merely pulling forward consumption from the future and therefore on the verge of the largest and fastest demand shock in U.S. history.

The current "inflationary" view is quite convenient for Wall Street and other industries that are benefiting from panic buying: No one knows when this will end, but it will end badly. Plausible deniability is also the convenient view to ride this year -end melt-up through bonus payout. So, there is tremendous conflict of interest taking place right now.

This article from the former head of India's central bank summarizes the tightrope central banks are walking:

"Former Indian Central Bank Governor Raghuram Rajan highlighted the tightrope that policymakers have to walk with monetary stimulus, warning that one false move may lead to a global “wealth shock” that could scare consumers"

What we notice is that ALL of today's pundits, including Rajan, believe that central banks are STILL in control over global markets. Therefore, they alone decide when this party ends. However, I am not of the belief that they are in control anymore. I believe they have the illusion of control.

In addition, I believe that this recent panic buying has fed into their backward looking data model and is giving them ALL a false sense of economic confidence. In other words, these are misleading indicators for the future. When we see that consumer confidence has now reached a decade low in this most recent reading, understand that these pundits can't afford to be wrong this time.

Case in point, Jim Cramer says he is going to use this week's retail earnings to get a "feel" for the consumer. What he is going to see is that sales and profits are up this past quarter, and therefore he's going to assume that consumer confidence is solid.

Whereas we already know it's collapsing. We also know that wages are not keeping up with prices. Which is very likely why the bond market is not reacting to the latest inflation news.

In summary, this era reminds me a lot of 2007. It's an industry game called "Dance while the music is playing" aka. Musical chairs.

"The Citigroup chief executive told the Financial Times that the party would end at some point but there was so much liquidity it would not be disrupted by the turmoil in the US subprime mortgage market"

As it was last time, the inflationist view is a mere RISK OFF event away from turning into a steaming pile of bullshit.

Slavish adherence to Supply Side Economics made it inevitable they would not see demand collapse. What this mass delusion is leading to is an inevitable super glut and overinvestment in everything. For today's true believers in Fed bailouts, calling this crash a "policy error" will be cold comfort...

If you notice, there isn't one pundit right now saying this is the end of cycle. To even say that is strictly verboten and could cause massive panic. These people all believe that central banks have permanently banished the business cycle. To be sure, the past 13 years of deflationary Japanification have been the longest uninterrupted debt accumulation cycle in U.S. history. Hyman Minsky never predicted the depths of deflation that would allow interest rates to remain pinned at 0% indefinitely.

Be that as it may, the bet right now is that this largest of all debt/speculation cycles continues forever.

It's as simple as that.

Those who are in the "inflation" camp are of the belief that there will be no Minsky Moment to pop this asset bubble and force mass de-leveraging. And yet ironically it's inflation that NORMALLY causes the Minsky Moment to occur. Were it not for the continuous importation of deflation, this runaway fusion reactor would have exploded a long time ago. Way back in late 2014, hedge fund manager Hugh Hendry predicted the day would come when central bank managed Disney markets would explode, but he also predicted that few pundits would see it coming. He believed they would be "drugged by the virtual simulation of prosperity and its acolyte QE".

And he was right.

My opinion and the opinion of very few others is that not only is the Minsky Moment at hand, but that the inflationary bias of today will make the outcome far worse. Why? Because the inflationary instinct is to hoard assets and accumulate debt. Whereas the deflationary mindset is to shed assets and shed debt. This inflation hysteria which is reaching a crescendo right now has the masses panic buying everything. Which is a colossal mistake. They should be raising cash right now. We are on the verge of a super glut. In everything.

Again, this mistake was made in 2008 and few seem to remember the outcome. Back then, the Fed initiated QE for the first time in history. This time they are already pumping liquidity at the highest rate in history. Back then they had 5% interest rate buffer, this time they have 0% interest rate buffer. In addition, this asset bubble has levitated not only the traditional economy, but it has simultaneously inflated the virtual economy Tech bubble.

What we are witnessing is the Pyrrhic victory of the virtual economy which began in the 1990s with the Dotcom bubble and Web 1.0 and went into final overdrive during the pandemic. Which is why I am calling this late stage melt-up the hyper asset bubble. Ironically, technology and automation are highly deflationary factors, because they increase supply without increasing demand.

There are many sub-sectors within Tech that saw a one-time extraordinary burst of demand during the pandemic: Cloud-based systems. Streaming content platforms. Crypto currencies. Electric Vehicles. Video games. And at the center of it all semiconductors. And all of that Tech demand was further super-charged by record amounts of cheap capital to fund all of the various Silicon Valley start-ups predicated upon the "internet of everything". The idea that we could all sit at home and have the world catered to our front doorstep. The only problem is this limitless growth fantasy has a last mile problem. It requires humanoids to physically deliver the merchandise. And unfortunately there are only so many of those to go around.

There is only ONE real supply chain shortage that won't easily be solved by this supply side hyper-growth model, and that is the labor supply. For ALL the reasons - early retirement, inflated 401ks, crypto Ponzi gains, work/life balance - the humanoids are going offline. Which gets us to peak Amazon. That company is now the largest employer in the U.S. and they can only continue to grow by bidding employees away from other Tech companies. Which means that they face slowing growth AND declining profit margins at peak valuation.Which is what they warned about in their most recent quarter two weeks ago.

But no bubble is quite as ludicrous as the electric vehicle bubble. EVERY car maker in the world produces electric cars already or coming to market in the next few months. Car and Driver lists every electric vehicle coming to market. There is nothing new or unique about electric cars anymore, they are commodities now. The only thing that's unique is the ludicrous market premium accorded these electric car companies. Today, the largest IPO of the year Rivian went public at a $100 billion valuation. They have $0 revenues and are running well over $1 billion in annual losses. Compare that to Ford which has $135 billion in revenues and several electric cars ALREADY in the market. And a lower market cap of $80 billion. There will be a massive glut of electric cars on the market a year from now.

And a massive glut of everything else as well.

Today we were told that the market tanked because of the 30 year high CPI print. But guess which sector was down the most?

Oil stocks.

Why? Because inflation is always highest at the end of the cycle.

Gamblers sitting on record unrealized gains at all time highs, now face the ticking time bomb of a Fed and Congress that will continue to remove monetary and fiscal stimulus until the market explodes. Why? Because the delusion implied by record asset prices is that everything is going fantastic. Therefore today's strategy of waiting for reality to catch up with fantasy isn't going to work this time...

This entire endgame gambit is compliments of the enduring economic myth of the jobless consumer. Now featuring record low total employment. Denialists are of the belief that the middle class can be plundered relentlessly without consequence, which has led to today's record divergence between asset prices and the economy.

Yes, I realize that prices have risen at a fast pace year over, just as they fell last year at a record pace. Although I don't recall hearing too much concern when that happened. Oil negative? Awesome. Much of what passes for today's "inflation" is due to one-time effects such as post pandemic inventory re-stocking, Christmas panic buying, rampant profiteering/price gouging, and of course record speculation in everything.

Case in point, "high" gas and oil prices are a total fabrication. Nominal prices of gasoline and oil are back at 2014 levels, far below the 2008 all time highs. CPI-adjusted prices are even lower. Using year over year price increases to describe "inflation" is highly disingenuous, and therefore unquestioned.

What would you rather have a 200% increase in oil to $150 or a 700% increase to $85? Based upon today's logic, the majority would find the former far preferable.

What it all points to is the fact that this Third World aspirational society has conflated a declining standard of living for "inflation". The critical question on the table when recognizing inflation versus deflation at the macro level is: are debt burdens rising or falling? Inflation benefits borrowers at the expense of lenders. Whereas deflation benefits lenders at the expense of borrowers. We are clearly in the latter paradigm as liabilities both on balance sheet and off balance sheet for households are increasing. The collapse in consumer sentiment is an indication that price elasticity is high and therefore demand is highly sensitive to changes in price.

The lethal question is whether or not this is sustainable. Because if it IS then inflationists are right. But if it's not, then it points to recession amid record asset values.

No wonder they're in denial.

Which gets to the primary risk we now face: Monetary policy is no longer functioning. We are now witnessing a record divergence between asset prices and the economy. Which means that the long-term outcome of monetary policy is exactly what one would expect: Lowering short-term interest rates to 0% has incentivized maximum debt accumulation. While lowering long-term interest rates to 0% has incentivized maximum risk exposure. Which is why we now have a massively leveraged economic time bomb with an asset market fuse attached to it.

Inflationists can be "right" so long as the bomb never detonates. And then terminally wrong from that point forward. All the while blaming "policy error" for their lack of foresight.

Which gets us to the casino.

What I see is a blow-off top within a blow-off top. This latest ramp from the early October lows is the blow-off top for the COVID rally. The COVID rally is in turn the blow-off top for the entire post-2008 rally.

But really, who would know better about these risks than the people who created them in the first place?

"The central bank also said that fragility in China’s commercial real-estate sector could spread to the U.S. if it deteriorated dramatically"

What gamblers need now is a time machine. Because once they realize they doubled down on a decade worth of risk landing in the fourth quarter, they will be competing with algos to get out the door into a bidless market.