My euphemism for market crash is "Policy error". Meaning forty years of failed Supply Side economics, ending in rampant denial with NO WAY OUT...

I don't normally seek affirmation for my point of view, because I am usually disappointed at what I find. However, from time to time in a moment of weakness I will head over to John Hussman's site for validation. This past week his post was called "The Motherlode".

"Across four decades of work in the financial markets, and over a century of historical data, I’ve never observed as many historical indications of a market peak occurring simultaneously"

Emphatically – and this is important – my intent here is not to “call the top” of this bubble"

So let me get this straight, we have the most concurrent indications of a market top in decades, but you are NOT calling the top. Why? Because to do so would risk credibility if the melt-up continues, that's why.

To be fair, Hussman has been consistent in his view that this is the most overvalued market in history and hence the least investable long-term. However as we see, he is far too circumspect with respect to describing the current level of market risk. His viewpoint is almost entirely directed at market valuation and technical indicators. He scant mentions the economy, nothing on China, nothing on global currencies, nothing about crypto, nothing on the housing market, nothing on corporate debt and where we are in the cycle, nothing about consumer sentiment and no mention of inflation hysteria.

He is not alone. Most of today's stock market pundits are blogging in a vacuum. Without considering these other factors one would conclude this is a stand-alone stock market bubble, not so risky after all. When the Dotcom bubble burst, recession began a full year later. On the other hand when the housing bubble burst, recession began immediately. This time we have both - a stock bubble and a housing bubble. However this time the Fed is ALREADY AT 0% on the Fed funds rate. So they have no dry powder to resuscitate the economy.

Worse yet, he gets defensive about being a “perma-bear”. He apologizes for not taking part in this festival of idiots. Make no mistake, I may be a perma-bear now, but I will gladly use the buy order when valuations return to earth. I call it buy low and sell high. It’s an old fashioned concept that today’s speculators have never heard about. What it comes down to is that no money manager would ever say “sell”, because as they always say if you get out you don’t know when to get back in. Hussman asserts that a universal sell order is not possible since all shares must be owned by someone. Every seller has a buyer. I suggest that is not true. Most share issuance over the past decades was corporate issued stock to cover options dilution. So no, the sheeple didn’t need to plow their life savings into human history’s largest pump and dump scheme. Of course everyone can’t sell in the middle of a meltdown.

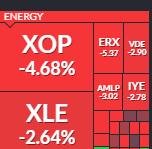

Which is why on Black Friday yesterday there were blue light specials in aisle 11 of the Dow, but no takers. Cyclicals were bidless as there were concerns over a new mutant virus. Remember COVID-2019? That was two years ago. Two years later and we still can’t find our ass with both hands. At present, the people who are fully vaccinated want everyone to wear masks and lockdown at a moment’s notice. While the people who are unvaccinated don’t believe in masks or social distancing. It’s the full retard approach to pandemic management.

And remind me again the last time the market was melting up into a pandemic lockdown and got monkey hammered? Oh right February 2020.

Deja vu.

You cannot be too bearish right now nor too critical of this festival of idiots. But you can put your capital and credibility at risk by having ANY part in it.

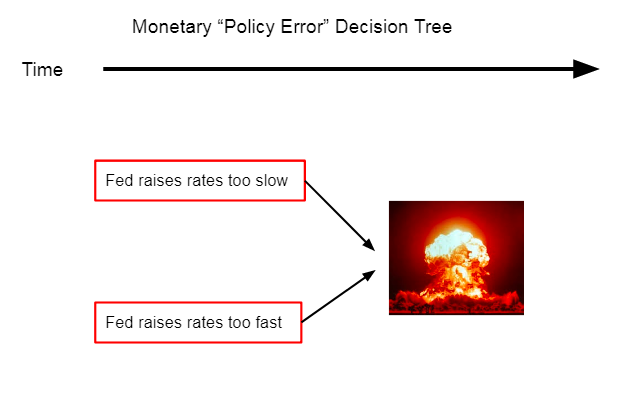

It’s clear that the Fed has fully euthanized this society and now even the bearish are complacent. Ironically what this inflation hysteria has done is to take another Fed bailout off the table. The FOMC minutes this week indicated many Fed members believe QE should be rolled off FASTER. In 2018, the S&P was down -20% before the Fed reversed policy. This time the market will be down a multiple of that amount. Meaning way too late.

And then the REAL acrimony will begin. Record inequality will ensure that policy-makers are highly constrained from implementing a 2008 style bailout.

Another massive risk that is in no way priced in.

The worst approach of course are those pundits who claim we have runaway inflation but caveat every single article with asterisk “policy error”. Meaning this can all end suddenly and abruptly, and hence economic reflation is binary. Which is what we saw on Friday with the Dow down 1,000 points.

What all pundits have in common is that they are ignoring the reverse wealth effect and how it will impact already collapsed consumer sentiment when the air comes out of the bubble. They’ve been ignoring the role of the wealth effect on the way up and its effect on consumption. So no surprise they are ignoring what will happen on the way down.

In summary, today’s market commentary is fucking pathetic. Weak and idiotic. Grade F all around. A festival of idiots with the only concern being left behind.