We are just a global margin call away from extreme deflation.

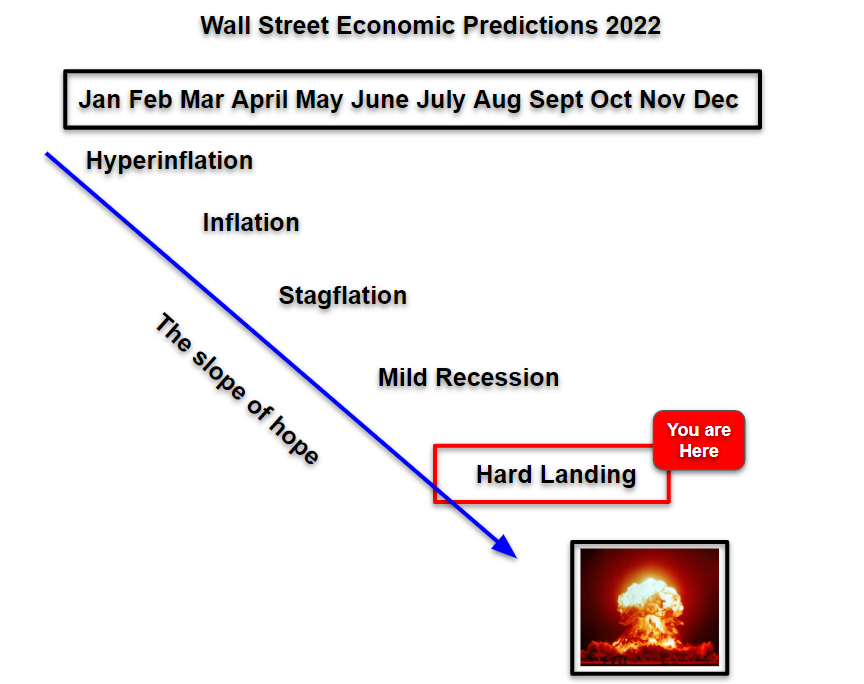

Wall Street's economic predictions for 2023 are science fiction:

The majority expect a mild recession or NO recession. A couple of banks expect a moderate recession. No one sees a hard landing on the horizon:

Friday's jobs report further fueled false hope that the economy could pull off a soft landing:

The problem with the "soft landing" delusion is that Fed tightening has caused every recession since World War II. The only soft landing (non-recession) took place in 2018 when Trump demanded the Fed pivot. It turns out he was right to do so, because the Fed ended up cutting rates three times in 2019. Unfortunately, this time around there are ALREADY signs everywhere that a hard landing is unfolding in real time.

What we are seeing across the economy is that unit sales have collapsed, and only prices are lingering at higher levels.

First off, this article from a few weeks ago confirms that an earnings recession has arrived as the spread between Morgan Stanley's profit model and analyst consensus is the widest since August 2008:

“We often hear from clients that everyone knows earnings are too high next year, and therefore, the market has priced it,” he wrote. “However, we recall hearing similar things in August 2008 when the spread between our earnings model and the Street consensus was just as wide.”

There were many profit warnings in 2022, but each time they occurred Wall Street analysts lowered the bar so the next quarter it appeared that profits were improving, when in fact they were going lower. That game has been playing out in every major sector. Neverthless, this past week Tech bellwether Samsung shocked markets with a staggering -70% drop in profit to eight year lows. The problem is that the Tech sector overall is still overvalued, however Tech earnings growth is now falling below the market average and going negative.

The same thing happened in 2000. The Y2K date change had pulled forward demand which was then accelerated by the Tech investment bubble itself. When the bubble burst, demand collapsed below the economic baseline, however company (over) valuations remained too high. This time around, the pandemic pulled forward Tech investment which was accelerated by hundreds of new Tech startups which are now imploding.

For all of 2022 there were 181 IPOs compared with over a 1,000 in 2021. Yes you read that right.

This week we learned that new car sales were the lowest in over a decade during 2022. Car prices remain elevated because car companies are still playing the "supply chain shortage" card.

Here we see the 12 month moving average of total new auto sales is the lowest since 2008 and before that 1992. Note that the recession after Y2K doesn't even register on this chart.

In my last post I indicated that pending home sales have collapsed to a record low. This is how that looks on a chart with housing stocks.

Deja vu:

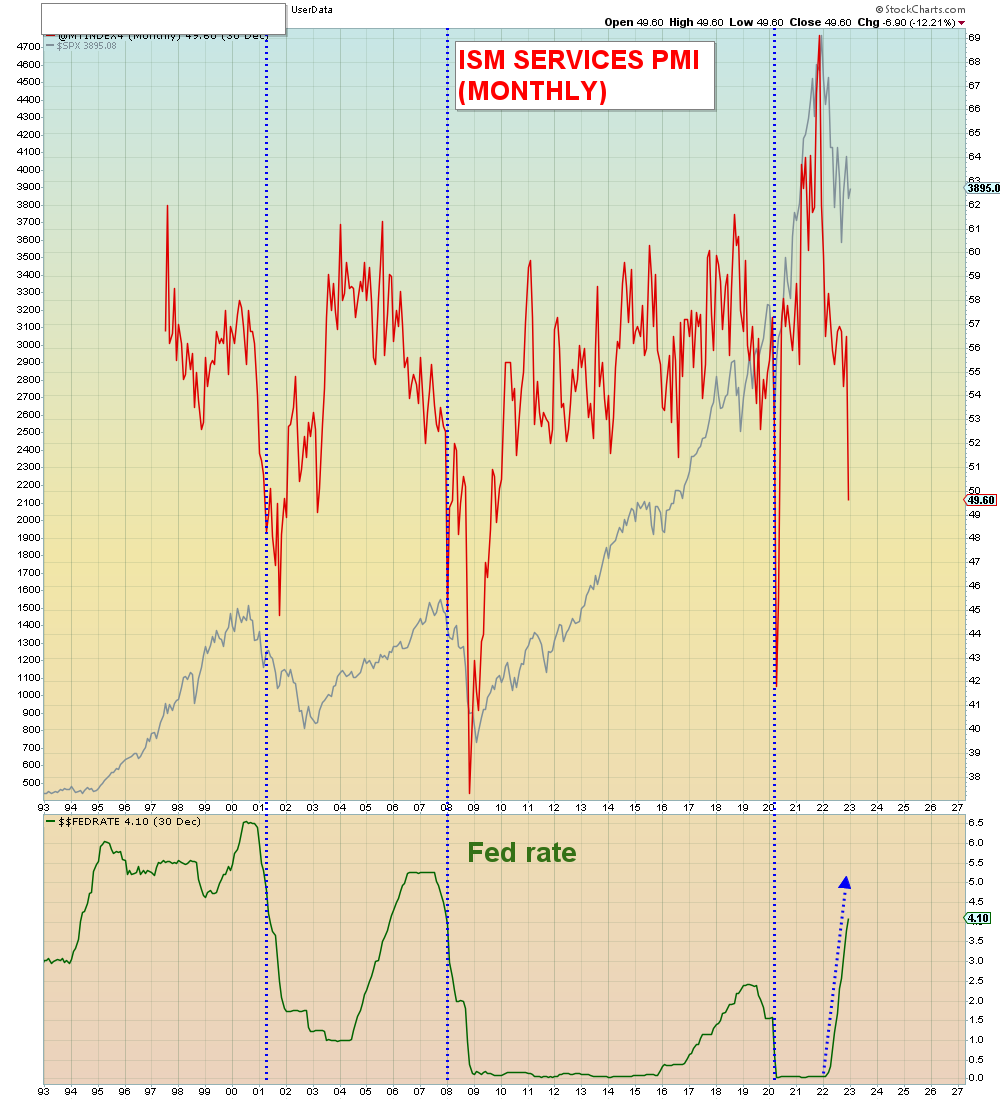

The real shocker this week came on Friday when the Services ISM fell below 50, indicating recession. Up until now we had been told that the services sector is strong. In three decades the Fed has never tightened with the Services ISM this weak. Every other time they were easing.

What we are witnessing is the largest policy error in history getting bought with both hands by the usual bagholders.

Retail and airlines imploding. And commodities imploding. The only time you see Airlines (Transports) collapsing along side oil is during a recession:

In summary, one would have to be totally delusional to believe in a soft landing, hence it's largely unquestioned.

Retail investors are heading for a deep burial at the hands of serial psychopaths.

THE END.