I have long asserted that Disney markets will implode everyone who believes in them. Now that prediction is coming true in broad daylight while well conditioned gamblers tighten the noose for the bungee jump off the cliff...

"One of the decade’s most successful quant strategies is poised for a dramatic March makeover that threatens fresh volatility for a stock market already reeling from the turmoil in technology shares"

“The violent downdraft (and subsequent rally) of last March is poised to create the most turbulent rebalance ever for momentum-based strategies”

Since Thursday afternoon, the S&P 500 crashed 120 points, rallied back 90 points, crashed 90 points and rallied back 120 to unchanged. That's a 10% round trip in one day. If you stepped out to have a life, you missed it.

"Net issuance of Treasury bonds and notes are set to hit an all-time high of $414 billion in March, almost the twice of the previous record"

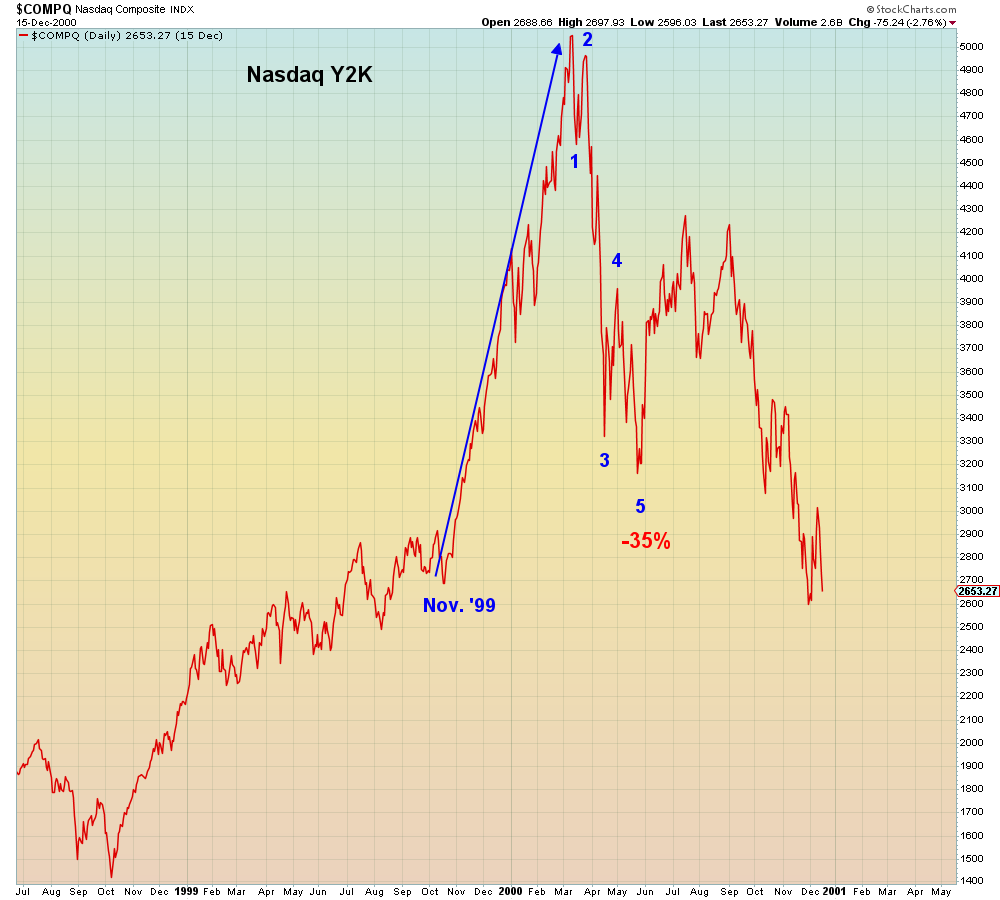

We were told back in the Y2K era that end of cycle value rotation could hold up the market, they were wrong -50%. We were led to believe in 2008 that value rotation would hold up the market, they were wrong again -55%. Now we are told that end of cycle value rotation will keep the market from imploding. They are wrong. The entire energy sector has a market cap less than Tesla.

In other words, don't worry, this is just getting started:

The Nasdaq is massively oversold and therefore due for a bounce. However, there is no sign of capitulation and no reach for protection which is why Tech stocks keep going lower:

Volatility scalpers don't realize yet that there has been a regime change:

The jobs report came in today at DOUBLE analyst expectations. Not what the bond market and Tech trades wanted.

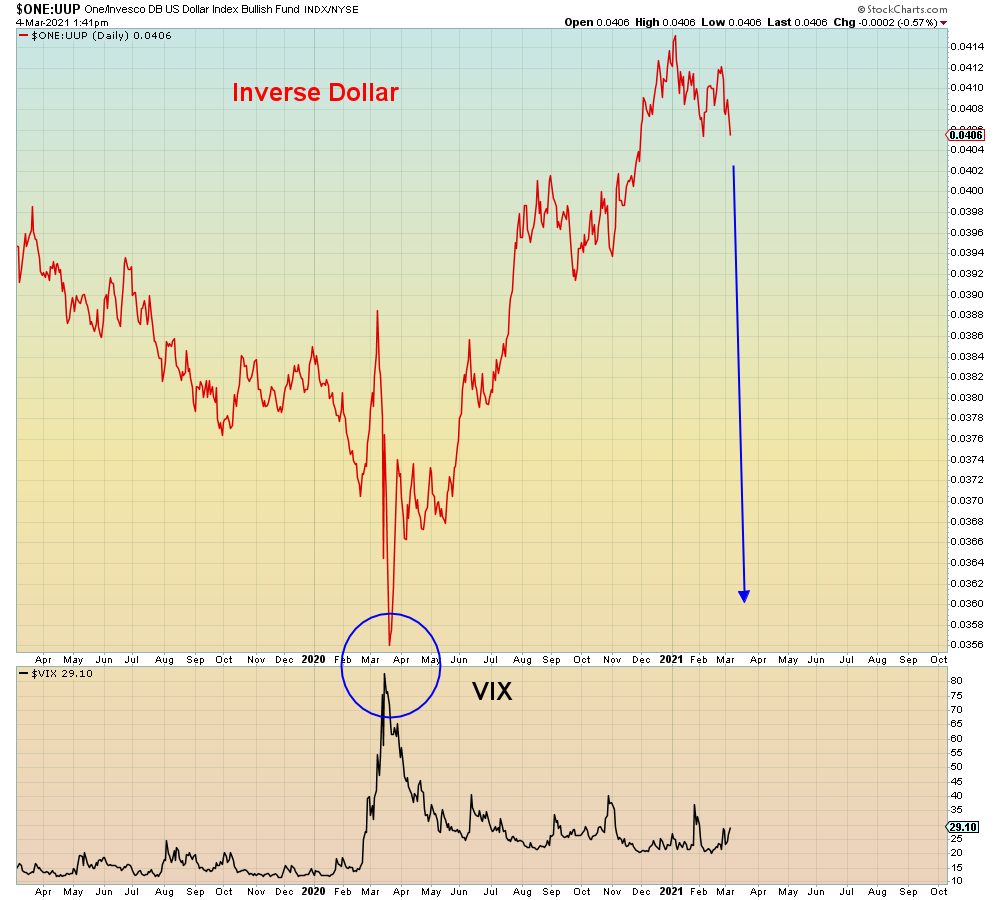

Also, EM currencies not happy:

Here is where it gets interesting going into next week.

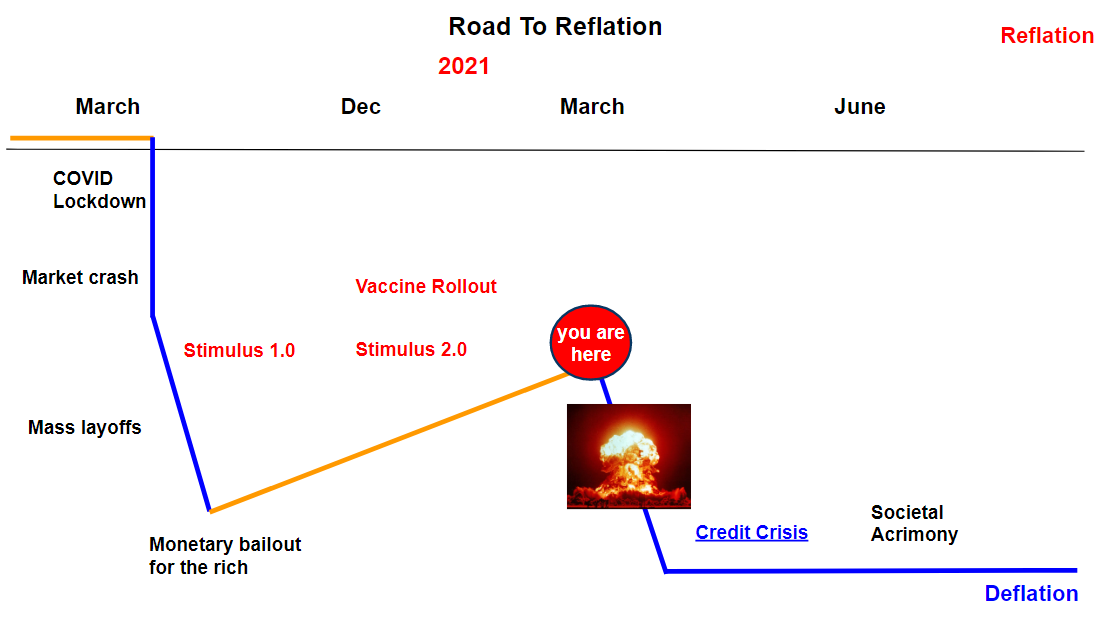

Late last week marked the low for Treasuries. This week, the t-bond market attempted to rally several times despite a deluge of inflationary bad news, including the highest inflation rate since 2008. Next week, the new stimmy package is due to get signed AND March is set to have double the record new Treasury issuance:

"Net issuance of Treasury bonds and notes are set to hit an all-time high of $414 billion in March, almost the twice of the previous record"

I think we all see where I'm going with this - T-bond shorts covered today into the jobs report news, which put a bid under Tech stocks:

Recall that Senator Toomey (Pennsylvania) demanded that the Fed relinquish its special bailout powers in the December Trump stimulus bill. Which is why corporate debt - the most levered debt market on the planet - is rolling over hard. This time around, the Fed WON'T be allowed to buy corporate bonds in the secondary market. Which is why Bill Ackman's big short is going to make even more money this time around:

What a difference one year doesn't make.

There are even more morons this time around than there were a year ago. We learned this week that Robinhood is planning their long awaited IPO, just in time for meltdown.

We can see where bears were this week last year. This entire one year rally was human history's biggest bull trap.

History will say that the COVID rally was the blow-off top in a decade+ Tech rally:

When this end of cycle value trap rotation ends, there will be no "winners" in Disney markets, except the usual psychopaths.

Any questions?