Today's investors all believe that as long as they never sell they can never take a loss. Unfortunately, that's not how it works...

What investors "learned" from the central bank assisted v-bottom in 2008 and again in 2020 is that as long as they never panic sell, they will eventually make up their losses. The 2020 losses were particularly short-lived because after March 2020, the Nasdaq entered its blow-off top, over a decade in the making. All of which explains why we are now witnessing mass complacency in the face of economic meltdown. Because that is how central bank moral hazard was ALWAYS going to end. Bulls loading up on stocks going into a depression.

I would remind bulls at this juncture, that Japan's stock market is STILL lower than 1990 and China's market is lower than it was 2008. And yet, BOTH of those central banks are STILL easing. Which puts to rest the Efficient Bailout Hypothesis.

Note that for Japan, the pandemic pullback preceded the melt-up into wave 'C'. It wasn't a bear market, it was merely a correction in an ending bull market.

But, but, but...this is the United States NOT China and Japan. In this country, back in 1929 it took 25 years to make a new all time high, in 1955. If you have that kind of time then finish your homework and go to bed on time.

In the book/movie "The Big Short" there was a period of time in 2008 when the economy and real estate market were clearly imploding but the subprime mortgage market remained well bid. The "CDS" contracts insuring subprime loans actually lost value because the risk premia came out of the market due to investors hungry for yield. This was the point in time when Michael Burry and a few others were the lone unwavering bears in the subprime market.

That's where we are NOW.

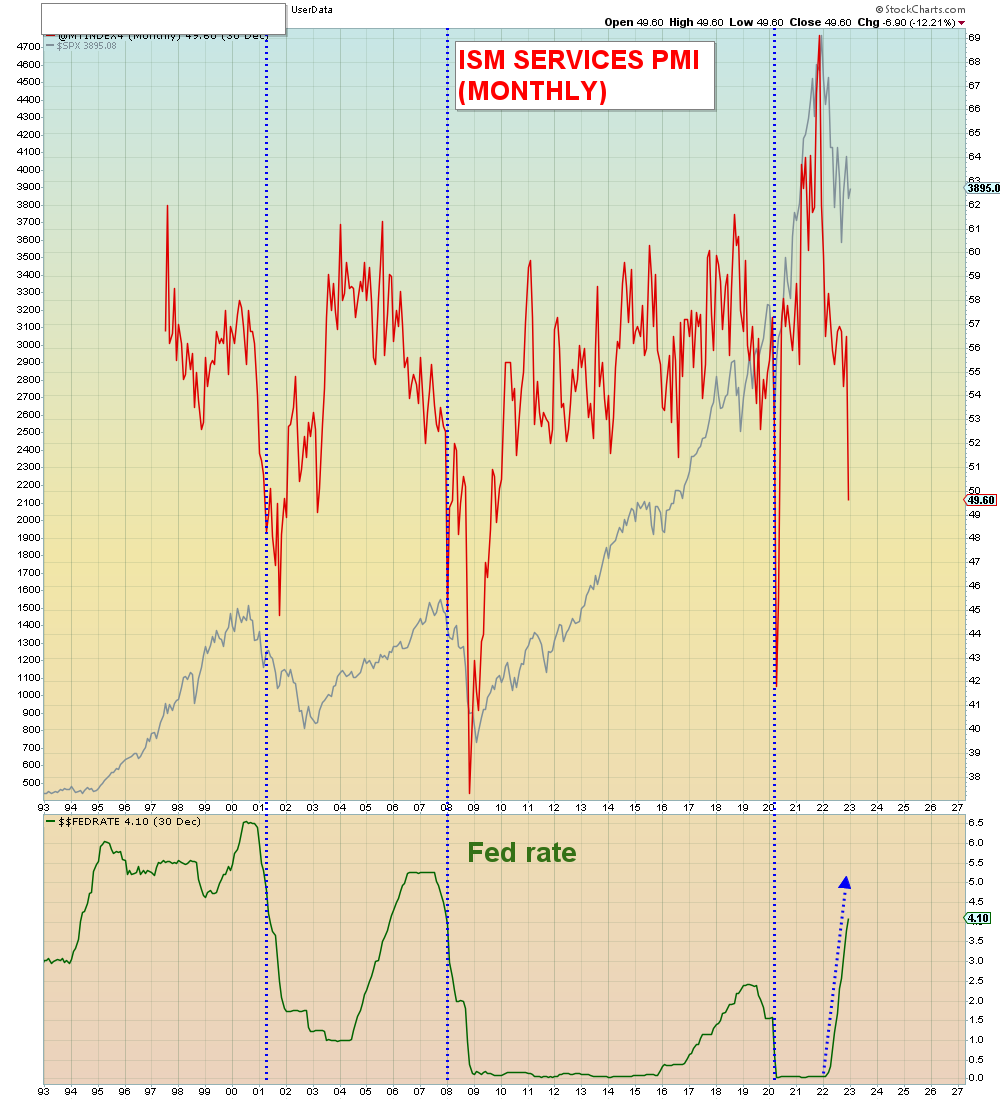

The economy is imploding and the real estate market is seeing collapsing sales - a precursor to lower prices. However, global risk markets are rallying.

The only traders who have capitulated are the bears, as we witnessed by the epic collapse in the VIX a week ago. Another place we saw bearish capitulation was in high yield spreads which are highly correlated with the stock market. The Fed is not going to rescue markets when markets are signaling that everything is A-OK.

FYI, in the past decade each time we saw the high yield spread blow out, the stock market was down at least -20%. .

Not only is the Fed not going to rescue markets, they are going to keep tightening which is what they said this past week. Three separate Fed members (Bullard, Mester, Brainard) said that the Fed rate must now go ABOVE 5% and stay there until inflation comes back down. Recall, that the Fed's target rate has been moving higher for over a year now. It should be called the moving target rate.

What we are witnessing is a massive bullish circle jerk into the abyss.

Clearly, the bear capitulation shows that being "right" on the market is not the same as being a good trader. In order to survive volatile markets one must spread their bets across asset classes and learn to take profit in stages instead of all at once. Be that as it may, the great irony of markets is that the greatest risk arrives when the majority of bearish participants have turned bullish. So unfortunately, for this event to be spectacular, bear capitulation was required.

Which gets us to the next order of business, bull capitulation. We can surmise that it would take a major meltdown to cause panic in this market. So that's what we should expect.

What I've noticed is that the "January Effect" has been very pronounced in recent years. The January Effect means that stocks that were dumped for tax loss purposes in the prior year get bought back in the new year. However, this effect now gets pulled forward into the fourth quarter.

Below, we see that EM stocks took massive losses in 2021 and 2022 and have now enjoyed a 25% rally. The same size rally they had in 2020 pre-pandemic. However, the biggest rally culminated in Q1 of 2021. We also see that U.S. consumer sentiment followed the same pattern. Each time peaking in Q1.

What's happening is that rebounding markets are dragging social mood higher.

In summary, today's investors have "diamond hands". But, it's their intestinal fortitude that will be system tested.

And it will shit a brick.

At which point all economic predictions for 2023 will be wrong, by a minus sign.

But don't forget, no one saw it coming.

October 2022: