Don't look down.

"U.N. Secretary-General Antonio Guterres said the report by the Intergovernmental Panel on Climate Change revealed “a litany of broken climate promises” by governments and corporations, accusing them of stoking global warming by clinging to harmful fossil fuels.

“It is a file of shame, cataloguing the empty pledges that put us firmly on track toward an unlivable world”

I used to worry about climate change. It was at the top of my list of existential worries. But since the pandemic, I finally realized all of this risk is outside of my span of control. The pandemic caused the largest collapse in carbon output in our lifetimes. It was temporary, but it showed the potential for what can happen when a species is preoccupied solely with personal preservation. After all, the pandemic was relatively innocuous. The U.S. states that had the lowest vaccination rates, the worst healthcare, and non-existent social distancing measures all fared just fine. By any account Alabama should have imploded. But they're still fat and happy. We were warned that our consumption-oriented way of life was ending, so what did we do, we went on a biblical scale consumption binge.

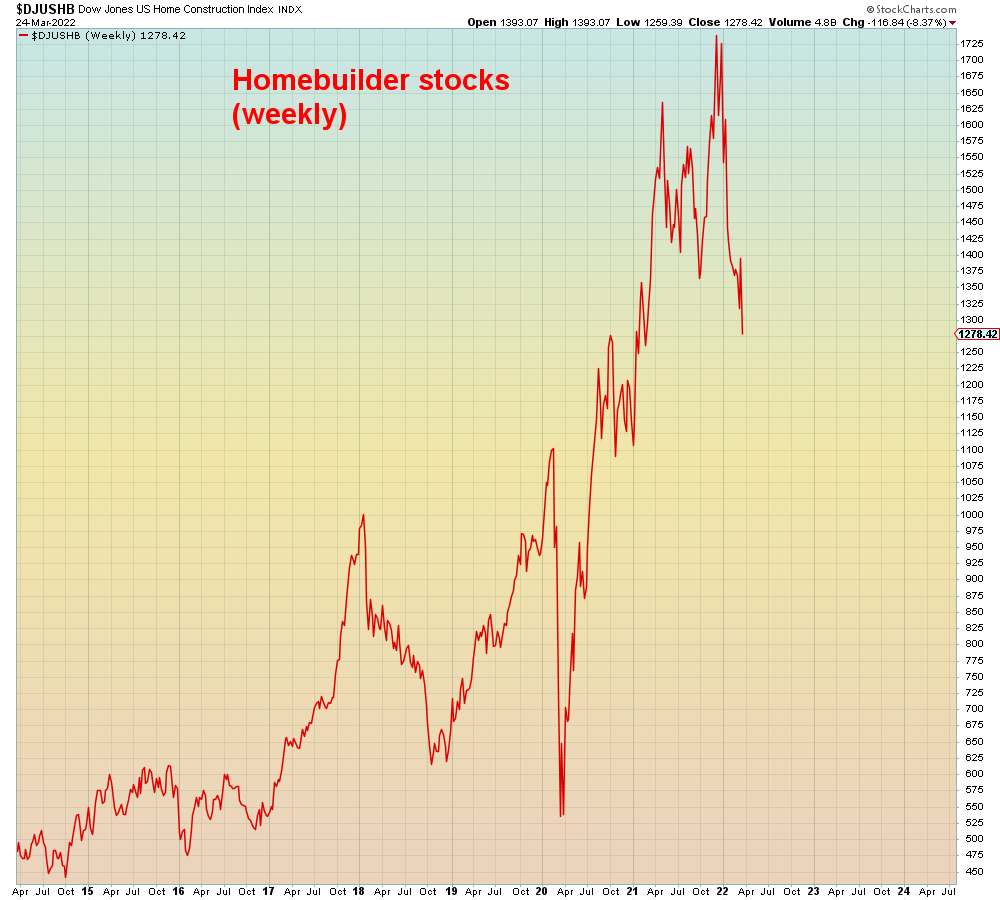

The pandemic and associated lockdown drove a consumption preference from services to durable goods. This consumption shift combined with the supply chain disruptions, caused inventories to become depleted. As a response retailers began double ordering and they abandoned just in time inventory techniques. This accelerated the "hyperinflationary" hysteria that fueled inordinate above-trend demand. As we see below, it was A MASSIVE consumption binge that is only now starting to abate as evidenced by recent declines in trucker freight rates.

You don't have to be a genius to see that durable goods consumption went above trend. However, in economics there is a concept known as reversion to the mean. Which holds that forays above the trend are followed by forays BELOW the trend. Looking at 2008 as by comparison, it's certainly not hard to believe.

Meanwhile, during this hyperinflationary consumption orgy, the Fed was busy inflating their asset bubble to record levels across every risk asset class on the planet. So now they are slamming on the brakes at the fastest rate in history, which we see below via the thirty year mortgage % change. Of course this is all the PERFECT recipe for total economic collapse. And the first order effect will be financial collapse and credit crisis, both of which already started in Q1.

"The housing market has gone into a savagely unhealthy stage. Everyone should embrace higher rates to cool off this madness and hope inventory rises," Logan Mohtashami, lead analyst at HousingWire, tells Fortune. "Let higher rates do their thing."

Aiding and abetting this disaster in progress, are all of today's financial pundits who are convincing people to ignore all risk. They have succeeded in convincing the masses that they can ride out a global depression, by hiding in stocks. These pundits have universally been fooled into believing that inflation is the biggest long-term problem facing stocks. None are more deluded than the Fed themselves who are now moving into what I call "Stage 2" global meltdown:

“Given that the recovery has been considerably stronger and faster than in the previous cycle, I expect the balance sheet to shrink considerably more rapidly than in the previous recovery, with significantly larger caps and a much shorter period to phase in the maximum caps compared with 2017-19.”

Below we see via momentum stocks, this was the level of decline at which the Fed pivoted to a dovish stance in 2018. Then in 2019, the Fed cut rates 3 times AND expanded their balance sheet due to the repo market dysfunction.

This time, they're going for FULL meltdown.

In summary, what's coming is what I call B.S. reduction. There is far too much hot air on this planet right now and most of it is emanating from proven psychopaths.

What this all points to is hard landing at the zero bound. A non-existent monetary interest rate buffer to offset the fastest demand collapse in world history.

Japanification.

Which means ZERO economic growth long term.

And a stock market that can be RENTED, but never OWNED. Because one thing this society will learn the hard way is in the end we are all just renters anyways.