Those of us on the periphery of this mass delusion don't "exist" from a statistical standpoint. The mainstream of current thought is dominated by Wall Street hustlers, Ivy League academics, ad-sponsored pundits, and all of their blind followers desperate to believe that failure at the zero bound can always get bailed out when it implodes.

On any given day the statistical probability of a "Black Swan event" is de minimis. Which is why pundits who wake up every day and have to infotain their audience, always give the same optimistic message - statistics are in their favour. In a world of statistical "independence" the odds of waking up to explosion are low. Which is why pundits never connect the dots or correlate risks. Because to do so would doom their cozy consensus. In their world all risks are independent of one another.

In the real world however, financial risks compound over the course of the cycle. The longer the cycle the greater the accumulation of leverage. All financial risk assets reach a correlation of 100% during global meltdown. This is Minsky hypothesis 101.

Add in the fact that 0% interest rate policy has institutions desperately hunting for yield at the end of the cycle and we now recall why AIG was selling insurance to Goldman Sachs on self-exploding CDOs back in mid-2008. Because they assumed they could at least make the quarter. Which after all is the only thing salesmen care about. Conflict of interest is rampant and it's clear that no one on Wall Street is willing to ever say "sell". Closet indexing is rampant and hedging is totally obsolete. There is no "upside" from going against consensus.

We have reached a juncture now wherein obligatory false optimism has merged with the pathology of denial. The best thing I can say about today's bullish financial pundits is that they are useless.

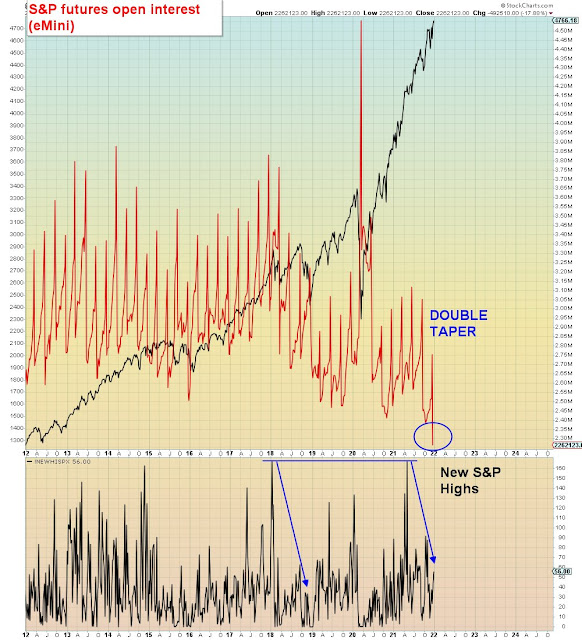

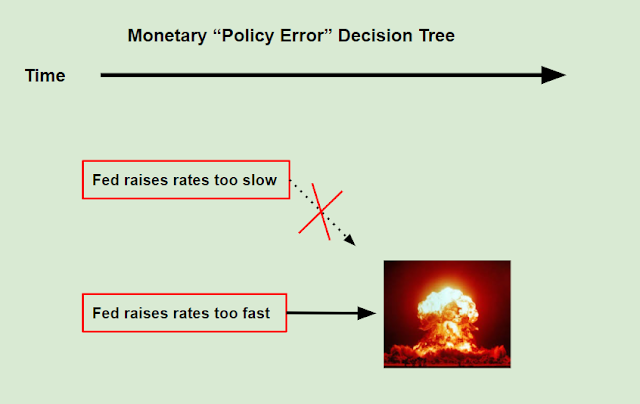

We learned this week that the Fed is set to once again accelerate their liquidity reduction. Back in November they began single taper. In December they began double taper. Now according to Fed minutes they soon plan to start downsizing the Fed balance sheet at an accelerated rate. This "news" of course came as a total shock to the market. Why? Because the Fed had previously indicated that taper was a pre-cursor to interest rate increase. However, now they plan to raise rates AND REDUCE long-bond liquidity at the same time. Which proves they are now just as concerned about runaway Tech stock inflation as they are about the runaway price of eggs. An oversight that is at the core of their policy error, and yet not one pundit today discusses that part of the policy problem.

BOTH Japan and China have already learned the hard way not to mess around with asset bubbles at the zero bound. Why? Because when they explode these bubbles have much greater economic impact and policy-makers have much less buffer to support the economy. This is a lesson that today's over-confident buffoons STILL have not learned.

Of course this current cycle of "inflation" should have been familiar by now, because it's literally the exact same sequence of events that followed Trump's election and tax cut in 2018. Back then, the Fed used fiscal expansion as a backstop to begin aggressively dialing back monetary heroin. However, then as now, gamblers were already as high as a kite and therefore they got monkey hammered in Q4 2018.

I call this cycle the stimulus Ponzi cycle, and it's as dumb as it sounds.

I make no predictions going into tomorrow's jobs report, only to say that the ADP report on Wednesday was 2x consensus at 800k jobs. An NFP that size on Friday would explode the Tech sector.

And what could be more biblical than a jobs report exploding the casino and thereby revealing all of the criminality-as-usual lurking below the surface.

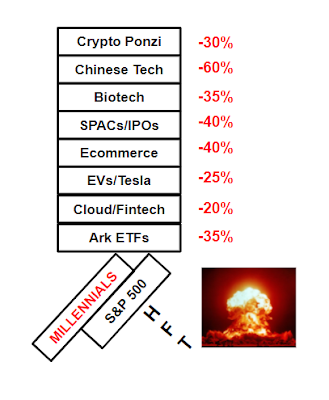

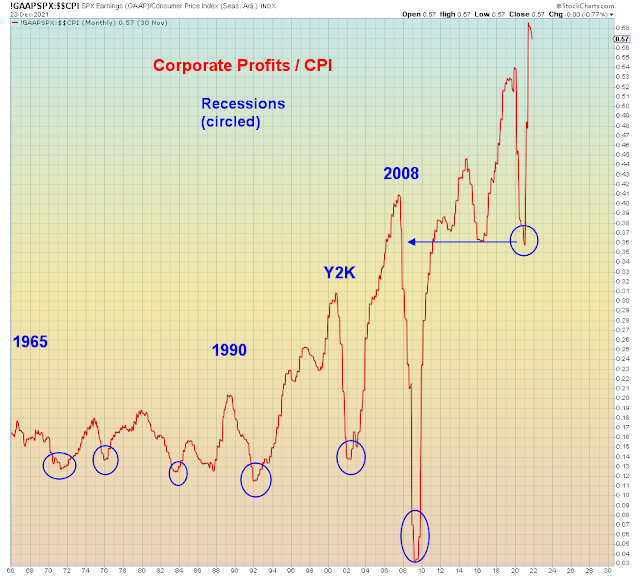

This chart exhibits the full extent of delusion at this juncture.

There is now a widely held belief that no matter how large a dislocation the Fed causes they can always bailout the casino. Which is why now despite the Fed embarking on a campaign of accelerated tightening, speculators are still maximizing risk allocation. It was inevitable after serial bailouts that the day would come when investors would double down on meltdown. This is a hard lesson the Chinese and Japanese have already learned.

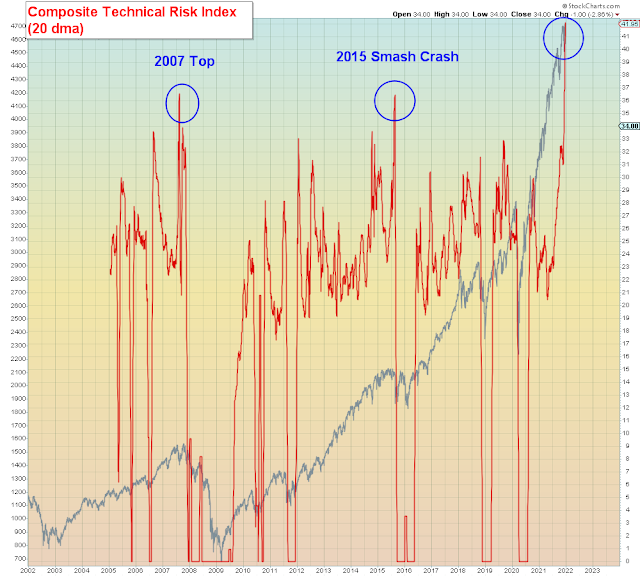

This chart showing the divergence between oil stocks and airlines indicates we are on the cusp of a Lehman Moment. One in which the Fed is too preoccupied with inflation to realize the meltdown has already started.

The divergence between the S&P 500 and consumer sentiment is the widest in four decades. The last time it was this wide was in December 2007 at the beginning of recession. It's the greatest example as to how today's pundits are totally clueless as to the true condition of the underlying economy.

Too many people now believe the stock market IS the economy.