As an antidote to ludicrous bull shit, I am now upgrading this debacle to Financial Armageddon. It won't be the end of the world, but it will feel like it for those who don't see it coming...

Following last week's strong but not "too strong" jobs report, we are now inundated with commentary saying that it was a "Goldilocks" report. Wasn't Goldilocks a fairy tale?

It's bull shit like this that energizes me to blog twice in a handful of days, something I haven't done in a long time. I am now of the mind that this is all coalescing into the biggest clusterfuck in modern history. Because when you layer on this kind of late cycle buffoonery you are inviting a level of societal rage that few can comprehend. To go into the worst financial crisis since 1930 invoking fairy tales is a bad look for the financial services industry.

First off, contrary to popular belief, the longer this inflationary debacle takes to resolve the MORE risk gets added to the bonfire. Why? Because in the inflationary paradigm, it makes sense to INCREASE liabilities on the assumption that wages are rising in lockstep. Imagine if you were conditioned to believe you would receive a 7% raise every year. You would load up on debt. Hence we just learned that credit card debt AND interest rates have sky-rocketed to record levels. And at a rate of change we've never seen before. In other words, debt inflation is very real.

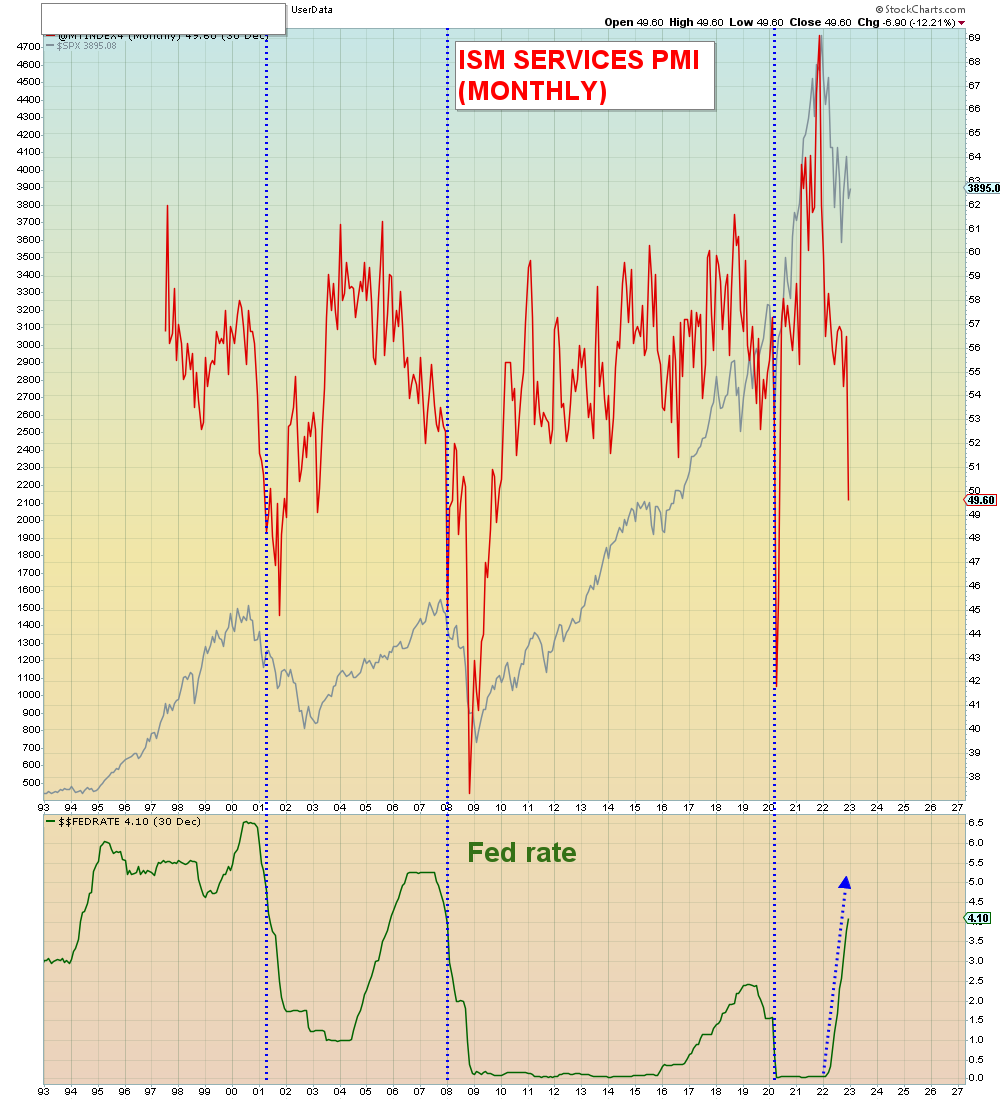

The Fed conundrum is that they can't ease UNTIL financial conditions tighten, otherwise they will create runaway inflation. However, investors won't capitulate because they've been conditioned by the Fed to expect a bailout. Both sides are locked in what I call a moral hazard death spiral. The Fed assiduously cultivated the bailout mentality for 14 years and now they can't get out of it.

Meanwhile, even as financial conditions are NOT tightening, bank lending conditions ARE tightening.

We've NEVER seen such a lethal disconnect such as this before:

All of which means that the inflationary hoarding mentality will make this event 10x worse.

Notice the Rydex ratio of cash balances as a ratio to all bullishly positioned asset balances.

This is the inflationary hoarding mentality at work. Retail investors have been told that they will lose money to inflation in perpetuity:

With all of that in mind, now imagine if you will, back in 2010 in the aftermath of the Global Financial Crisis, someone telling you the following fantastical story:

In the span of a decade there would be an asset bubble that would dwarf 2008 in magnitude. It would arise out of a global pandemic and it would span every asset class, including crypto currencies. What are crypto currencies you would ask, and you would be told they are thousands of digital Ponzi schemes with trillions of dollars in market cap and ZERO net worth. And they are fully legal and accepted without question even in 401k retirement accounts. Because they are considered safe havens from inflation.

So far, so good: a bigger housing bubble than 2007, a bigger Tech bubble than Y2k and something called a crypto Ponzi bubble. All of which asset inflation causes economic inflation to explode to the worst levels in 40 years. So what do central banks do? They extreme tighten at both ends of the yield curve at the same time. Until one by one the dominoes start falling. Starting with crypto Ponzi schemes, junk IPOs, pot stocks, electric vehicle bubble stocks, then moving on to global housing markets, autos, and mega cap Tech stocks. Until everything is imploding at the same time, but central banks are STILL tightening. By the end, all of the asset markets are imploded while liabilities remain at all time high in a deflationary depression.

The story continues that China, which drove the world out of recession in 2008, is only finally emerging from a Maoist-inspired total lockdown three years later, their economy decimated. So they throw the doors open to the world and watch as their virus death toll explodes out of control among their totally unprotected populace, as their economy final implodes.

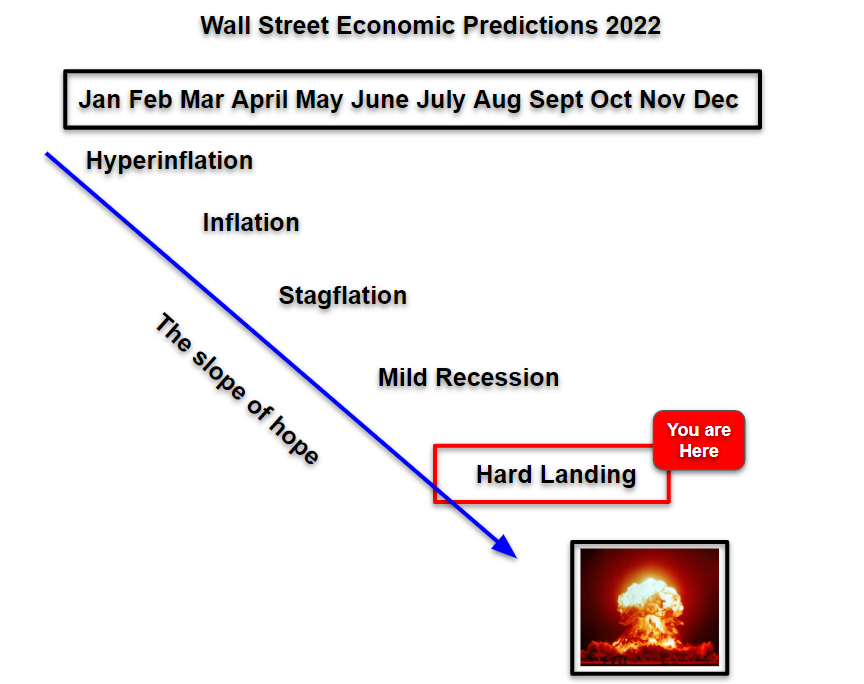

Meanwhile, the pundits of the day are telling the masses to expect a soft landing because the Fed has magical powers to bailout everyone from disastrous financial decisions caused by cheap money, using more cheap money. Ignoring the fact that if they could do that, 2008 would never have happened.

And they lived happily ever after.