mor·al haz·ard

"Lack of incentive to guard against risk where one is protected from its consequences"

Wall Street has converged on the seamless bailout hypothesis. What could go wrong?

It's a very sad day when all of investing has boiled down to begging for central bank bailouts. The entire bullish thesis now rests upon central banks capitulating against inflation.

The consequence of the 2008 Wall Street bailout and subsequent continuous monetary bailouts is that central bank invincibility is no longer questioned. Even in a high inflation scenario such as the one we face, the inevitability of higher markets is largely unquestioned.

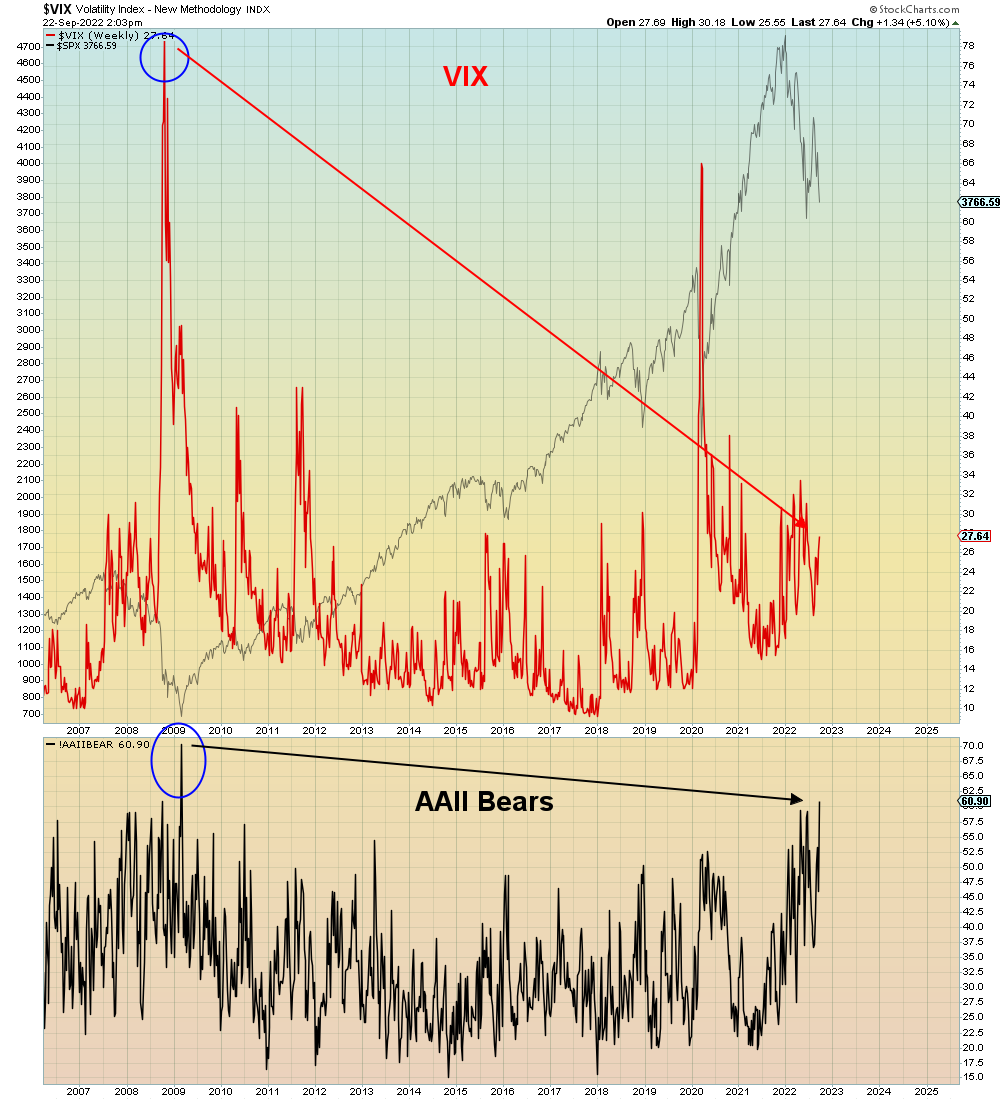

Over the course of 2022 as the market has stair stepped lower, Wall Street has slowly and surely downgraded their price forecast to a "worst case" consensus level of 3000. Which is a 40% total decline and roughly 15% from the current level. That point of view is now shared by Bank of America, Morgan Stanley, JP Morgan/Dimon, Gary Shilling, and the once uber-bearish Jeremy Grantham, who now finds himself with plenty of company. The outlier is John Hussman predicting a 50-70% decline. Michael Burry does not give price targets.

This article lays out the "bull case" of a fast -20% decline followed by a certain Fed bailout and 50% rally. In doing so, the article inadvertently lays out the 1929 scenario of a ~45% initial decline followed by a 50% rally. Which by the way, would still leave the market 10% BELOW the all time high. Basic math now being beyond the capacity of this society. In other words, the bull case and the bear case are largely the same now. Which means that a TRUE bear case precludes a seamless bailout scenario. Which I will discuss further below.

Going the exact other way, Peter Schiff expects hyper-inflation due to a Fed pivot that reinflates the everything bubble. He asserts that today's central banks lack Volcker's fortitude to deflate markets. What he doesn't understand is that the bond market is not going to allow rampant inflation. Real yields as measured by the nominal yield - CPI are ALREADY the lowest in U.S. history. According to Schiff they are about to go much lower. We are to believe that the Minsky deleveraging moment can be deferred forever while market rates sky-rocket. Sure. It's tremendously ironic that in 2022 inflationists have finally been proven right after 40 years of continuous deflation. However, in this year the dollar has sky-rocketed meaning their trades have imploded anyways.

Fed governor Chris Waller astutely laid out the Fed's dilemma last week - which is that shelter costs in the U.S. as determined by rents, are going to continue to keep CPI elevated for months into the future. Each month only a subset of leases expire and are rolled over to the new higher rates. Therefore, older lower rents will inexorably rise.

"The inflation statistics use a six-month average when calculating rent growth. Asking rents and rents on new lease contracts—which do reflect contemporaneous rental market conditions—have been rising at a fast pace for more than a year. These increases have fueled shelter inflation so far this year, and they should continue to do so for at least the next six months"

The Fed is in a sense lucky, because if they measured inflation based upon the cost of carry for homeowners, the current inflation rate would be FAR higher than it is currently. The combination of house prices and interest rates has raised owner-occupied carrying costs by 100% in the past year. You read that right. That fact has priced new homeowners out of the market and placed even more pressure on rents. In other words, the Fed itself is STILL a key source of inflation by raising shelter costs.

The Fed used their balance sheet to inflate the housing market and now they are using interest rates to bring it down. It's two policy errors for the price of global meltdown.

All of which from an investment standpoint leaves just the now universally anticipated "accident" scenario followed by bailout. We can surmise that the bar is now VERY high for what would force a Fed pivot. Something on the order of a 1998 Russian Default/LTCM meltdown. The problem is that such an event would immediately tip the world further into global depression. In other words, trapped bulls will realize far too late that they bought a false promise of seamless bailout.

Any blind man can see that U.S. consumer sentiment is at an all time low whereas in 1998 it was at an all time high.

Subtle difference.

All of which means this market is tradable but no longer investable. There will be large trading rallies followed by large declines. So far, we've seen small trading rallies followed by new lows.

This roller coaster scenario is what Japan and China have already experienced at the zero bound. And what the U.S. experienced in the 1930s.

Arguably gold is a long-term hedge against inflation and monetization of deficits. However, we must go through the deleveraging phase first which will be highly deflationary. I have no long side conviction in gold at this juncture.

In summary, the KEY point Wall Street never admits is that you can't always put the toothpaste back in the tube.

Position accordingly.