Everyone loves asset bubbles, right up until the time they explode with extreme dislocation. Anyone who speaks against them is as popular as a gambling counselor in Las Vegas. This society is now totally desensitized to fraud. Which is all fun and games until someone loses an everything. What this all sets up is the worst case scenario for an end of cycle obscured by rampant speculation and obligatory bullshit. But no one sees risk anymore because in 2022 all of America's organized crime syndicates are now corporate. To question "the system" is heretical...

"As the end-game approaches, it becomes a matter of imperial self-preservation to breed a special-purpose ruling class—one that is incapable of understanding that the end-game is approaching. Because, you see, if they had an inkling of what's going on, they wouldn't take their jobs seriously enough to keep the game going for as long as possible"

This society has survivor bias on cycle high steroids. History will say that global central banks created the largest asset bubble in history and morally challenged pundits just went along for the ride, because it was the path of least resistance. And more importantly, it was the MOST LUCRATIVE. In 2021, Zerohedge perfected the ad-sponsored circle jerk. Congratulations are in order. There is no market for pissing on a parade, so they too gravitated to the cheerleading model. Which is why today's financial pundits take absolutely zero responsibility for how many people get obliterated by all of today's financial scams. In the first quarter came the Gamestop pump and dump scheme which drew in hordes of newbie investors. What most people don't realize about Gamestop is that ultra-wealthy investors came in at the top and shorted it massively, obliterating latecomer newbies. Bill Gross made $10 million on the short side, but only large investors with prime broker access could borrow the shares. Most of the retail suckers were on the long side of the bet getting wiped out. I never heard a thing about that in the press, it was all a triumph for the little guy.

In the second quarter 2021, billionaires Elon Musk and Mark Cuban touted a joke crypto currency called Dogecoin. Once again, newbies piled in late and got decimated. Those two scams and the myriad copycats that followed all year padded broker revenues, especially Robinhood the Candy Crush front-end to Citadel. Of course late in the year they announced that revenues were collapsing as they were running out of fools to monetize.

Wall Street dumped record junk into the market all year long. That was met with a shrug.

Two decade high inflows to stocks. Who cares.

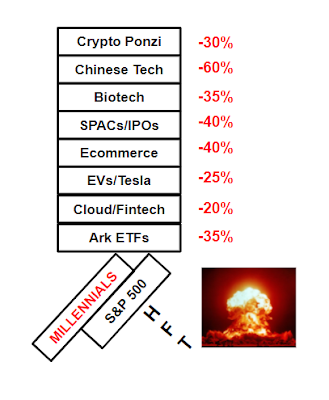

Cathie Wood CNBC celebrity, down -45% on the year. Big deal.

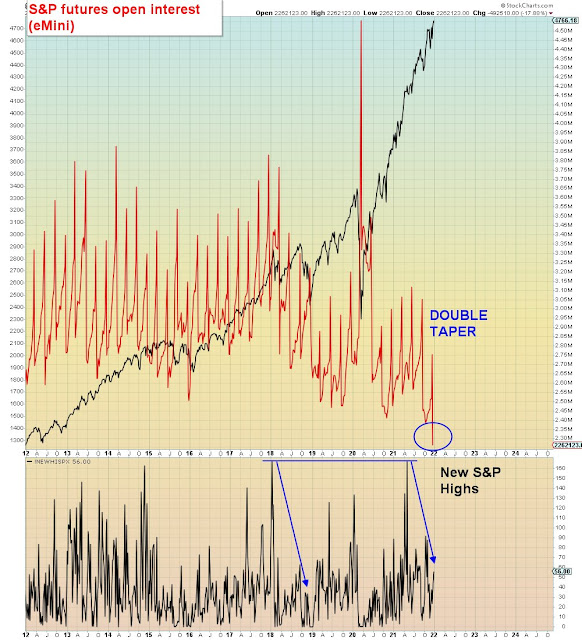

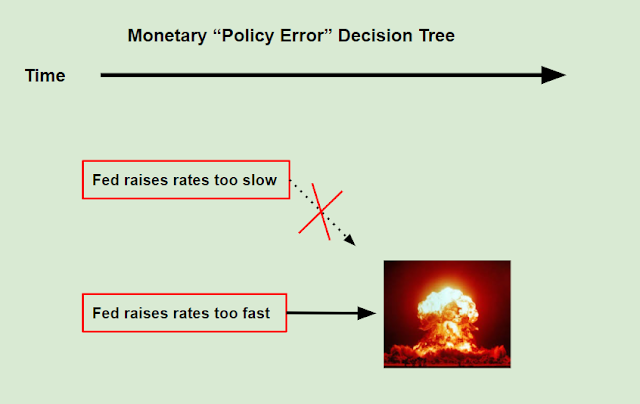

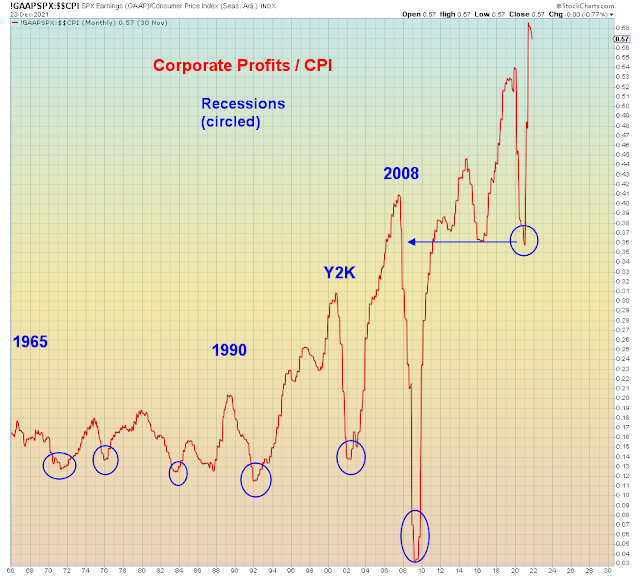

Today's pundits know full well the Fed created this asset bubble, and now they're unwinding stimulus at a double pace. How many are warning about that risk? None.

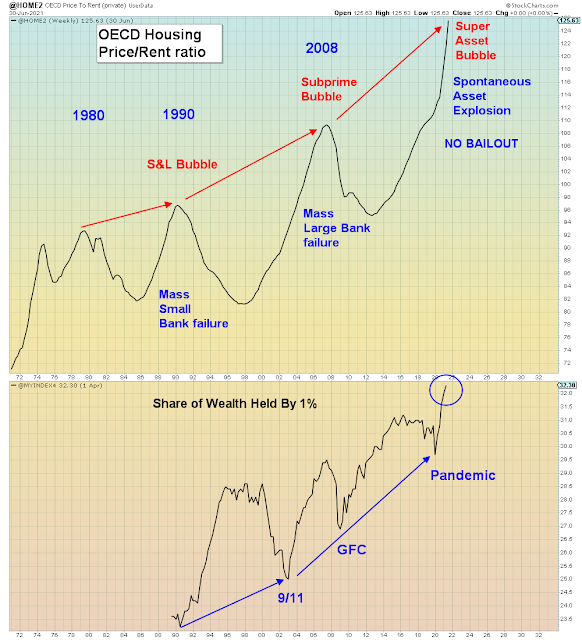

The red hot housing market peaked a year ago in January as far as new homes sold. That same event heralded the peak in the 2007 housing bubble. Back then the Fed had 6% interest rate buffer to cut to offset the economic dislocation. This time they have 0% to cut. Yawn.

None of that can compete with the celebration of excess taking place right now.

Unfortunately, it all lands in 2022, which is the worst case scenario. Why? Because when a bubble crosses a tax year then it locks in prior gains for tax purposes while still exposing capital to massive loss.

This was the lesson NOT learned from Y2K which is that tax losses can be carried FORWARD, but not backward. There were thousands of DotCom paper millionaires back in that era. Most of them exercised their shares and then held onto them instead of selling them, because they wanted to pay the lower long-term capital gains rate. However, the exercise itself is considered a taxable event by the IRS and it's taxed at the difference between the current market price and the strike price. That sets up the liability. What happened back then is that employees exercised in 1999 and in 2000 they got wiped out when the bubble collapsed. Then the IRS handed them a bill for a few hundred thousand dollars. They went from being a paper millionaire one year to being bankrupt the next. It's happening all over again right now with 2021's stable of record unicorn IPOs.

But who is warning about this? NO ONE.

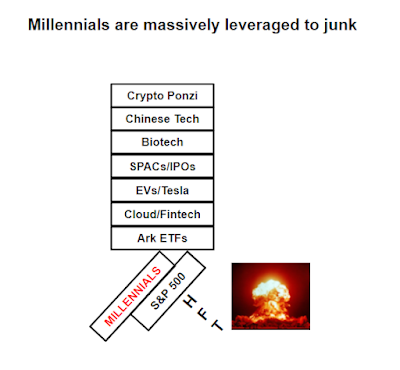

We have a generation now in the Millennials who are simultaneously exposed to Tech stock risk, housing market risk, $1.7 trillion student loan risk (which is 2x subprime), $2.5 trillion in crypto risk (which is 3x subprime), IRS sticker shock, the healthcare crime syndicate which is the #1 cause of bankruptcy and end of cycle job risk. All at the same time.

And who is warning about this?

NO ONE.

Fucking pathetic.

We're putting an entire generation at risk because our society has the morality of a used car salesman.

Half of young people ALREADY feel like they're drowning, and the other half are about to come along for the ride.

Below we see how the casino finished up in 2021:

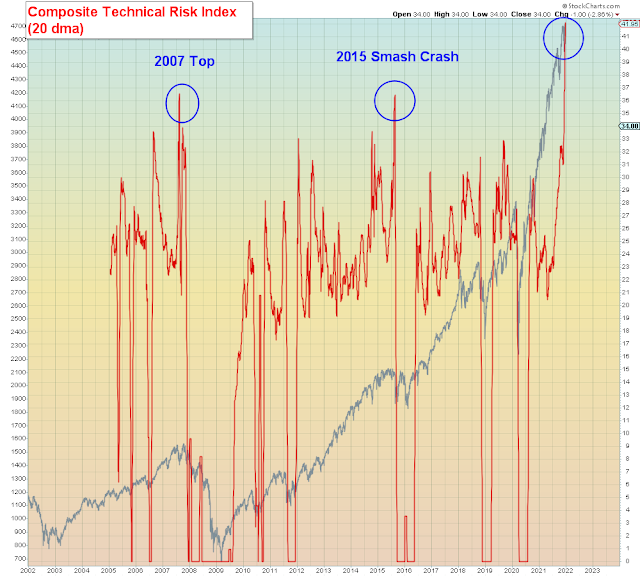

Here we see in the top pane that weekly Nasdaq new highs peaked back in February, had a lower peak in November and ended last week (last year) at the lows of 2021 (vis-a-vis an S&P all time high).

In the second pane we see that Interactive Brokers Daily active trades also peaked back in February, a lower peak in November and then ended December at the pre-2021 level.

The Bitcoin trust, same idea. It already gave up MORE than its entire 2021 gain mid-year, does anyone believe it won't happen again?

It's ALL ONE MARKET now massively levered to a generation on the verge of explosion. And ALL of today's older paper millionaires are massively leveraged to a generation they threw under the bus.