To begin, let's review the year to date, using the chart above as reference. The equal weight shows that the YTD break-even has been a key pivot point for stocks all year long. The year began with tremendous optimism towards China. The country that infected the world with pandemic was finally emerging from the pandemic by exiting all lockdown protocols. Chinese stocks, led by Hong Kong, vaulted off of the November 2022 lows and reached their peak of 2023 at the end of January 2023, as marked "China rally" above. That was it. The high of the year for Chinese stocks. The next thing you know, China RISK OFF imploded global markets and sparked a U.S. bank run.

As we all know, several large regional banks failed at the March low, but the FDIC found buyers for the largest ones and fully bailed out the smaller banks. Crisis solved. However, in May of this year, the FDIC wrote a memorandum stating that the FDIC Deposit Insurance Fund (DIF) is at risk of depletion, and they will not be able to fully bail out uninsured depositors (aka. > $250k per account) going forward. Their proposal is to bailout above the $250k limit ONLY if the deposit is a working capital aka. "payroll" bank account for a business. What they call "targeted" coverage. Nevertheless, the main takeaway is that of course nothing has changed since the Spring bank run. Except that risk has increased exponentially.

Here are some highlights of their report, which you can read yourself:

"Trends in uninsured deposits have increased the exposure of the banking system to bank runs"

"Technological changes may increase the risk of bank runs. The speed with which information, or misinformation, is disseminated and the speed with which depositors can withdraw funds in response to information may contribute to faster, and more costly, bank runs"

"From year-end 2009 through year-end 2022, uninsured domestic deposits at FDIC-institutions increased at an annualized rate of 9.8 percent, from $2.3 trillion to $7.7 trillion"

For comparison, the Deposit Insurance Fund equals $117 billion.

Notably, the report only casually mentions the ongoing threat of massive bank unrealized losses due to the bond market collapse. During the pandemic, banks had a massive inflow of new deposits arising from the various stimulus programs, so they did the easiest thing with the money which was buy long-term bonds. Since interest rates have exploded higher, those bond portfolio values have collapsed, leaving a ticking time bomb on bank balance sheets, as you can see below:

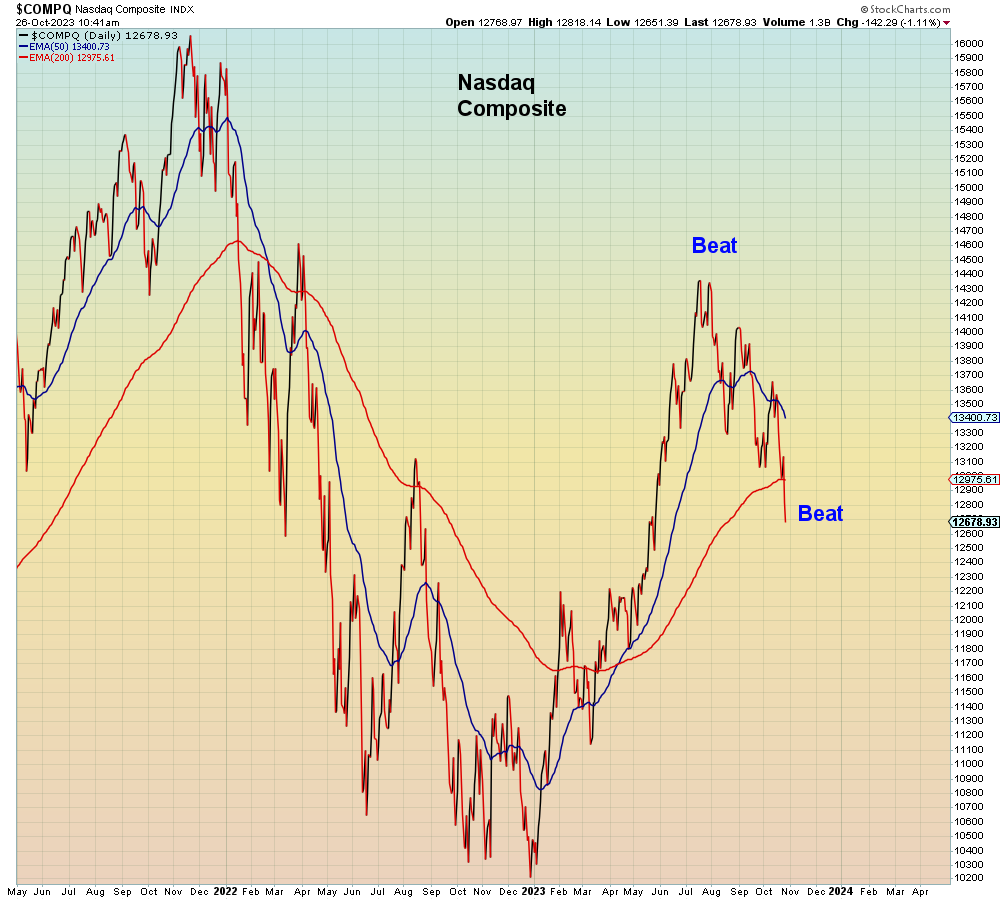

Going back to the first chart above, the second rally of the year was driven of course by the Artificial Intelligence Tech blow-off top. We can view the Tech rally from the perspective of a three year topping process that began back in early 2021 with the peak of the "Work from home"/ ARK ETF / IPO SPAC junk. The second peak was in late 2021, at Thanksgiving, which is something I point out on Twitter all the time because the Nasdaq all time high was in the days prior to Thanksgiving.

Interestingly, the 8 day moving average of the ISEE call/put index this week, was the highest since the Nasdaq all time high.

Here is where it all comes together:

AI leader Nvidia released their earnings on Tuesday night but the stock imploded on Wednesday. Their earnings and sales handily "beat" expectations, including a 200% year over year increase in sales. The problem is that the stock is already up 400% year over year. The second problem is that going forward, they forecast much weaker sales out of China (which accounts for 25% of their total revenue), due to the recently-imposed U.S. semiconductor export restrictions.

In other words the leading sector and the one that made new highs this fourth quarter is about to experience a drop in sales. Because what Nvidia didn't say - and no Wall Street analyst thought to mention - is that Nvidia will not be alone in being affected by export restrictions to China.

This is going to affect ALL U.S. semiconductor companies.

The article of the week has to be this one explaining that hedge funds are now record crowded into Tech stocks, with TWICE the weight in Tech that they had at the beginning of the year:

"Megacap growth and technology stocks accounted for 13% of the aggregate hedge fund long portfolio, twice their weight at the start of 2023"

However, as popular positions gain momentum, there is a growing risk of crowding, which reached its highest in the 22 years since Goldman started tracking the funds"

This week through Wednesday caps Tech's largest four week run % gain to a new all time high since Y2K.

What does this have to do with banks?

As the Nasdaq oscillator shows, they're as overbought as they were at the beginning of this year when China risk off imploded global markets.

In summary, the lesson learned is don't ignore what's going on outside of your own little world, because the FDIC has already said that next time there's not enough bailout to go around.