Recap: October capped off the largest three month decline since March 2020. So far, no sign of panic or capitulation. Whenever the market gets oversold it bounces, and then goes lower. This has been the pattern since the July top. Here we see that the market is in a clear down-trend, with each rally of shorter duration. There was an oversold bounce at the last FOMC pause in September. On Wednesday of this week, the Fed paused rates for the second meeting in a row, for the first time since they started raising rates. This is the scenario bulls have been waiting for all year long.

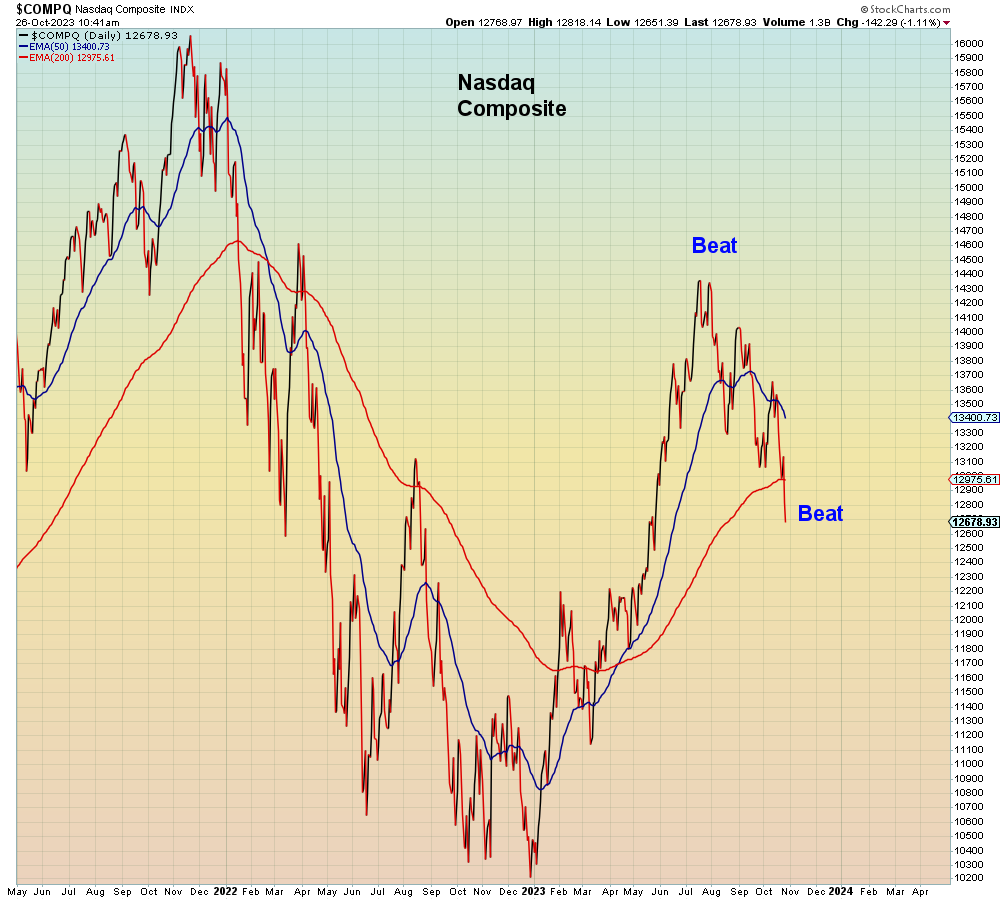

The Nasdaq is in a similar downtrend and currently clinging to the 200 day moving average.

Today after the close, we get Apple earnings. As I pointed out in my last blog post, Tech earnings have so far been met with heavy selling. Including beats. But Apple is expected to post another earnings decline, so that should be better?

"There are four forces working against Apple in the December quarter: An unfavorable comparison, a strong dollar, iPhone supply issues, and a cautious consumer"

Bulls inform us that it's bullish we avoided a recession and it's also bullish that the Fed has ended rate hikes. However, for the bulls, now every economic data point is a potential landmine that could set-off another round of Fed tightening. For example, Friday's jobs report.

Meanwhile, earlier this week the BOJ further widened their yield band and said that the 1% level is now merely a "reference" point. Which means that if U.S. economic data runs weak, the yield gap between U.S. and Japanese rates should continue to close, trapping bulls in collapsing carry trades.

In other words, both the "too hot" scenario AND the "too cold" scenarios are now fraught with delusional risk.

In summary, the average stock almost took out the last October lows during the past month, but the cap weighted averages shown above remain significantly above the lows.

Which means that now the bet is whether or not markets collapse between now and the end of the year.