The widespread belief that this is the 1970s deja vu has ensured this will be the hardest landing since the 1930s. Sadly investors are now trapped in Jackass Utopia...

Mass confusion reigns supreme. Case in point, this week Wharton Professor of Finance, Jeremy Siegel, pounded his fist that the Fed is over-tightening:

"It makes absolutely no sense to me whatsoever, way too tight,"

Back in late May of this year Siegel was still asserting the Fed was way behind the curve and inflation would remain high until 2024:

May 2022:

“We’re going to have high inflation throughout this year and into next year, and I don’t really see a slowdown until 2024,” Siegel said. In fact, the official inflation figures are understated"

In other words, Siegel and the majority of other pundits who have been pounding the table on hyperinflation all year are the reason why investors are now TRAPPED in their imploding Jackass Utopia.

Of course, Siegel's most recent opinion is correct - the Fed is way overtightening.

The housing market is essentially shut down now as mortgage rates are almost at 7% this week vs. 3% a year ago.

Who refinanced a year ago and now wants to pay $20k additional interest per year on a $500k mortgage? No one.

"Some of the biggest players in the real estate industry, including RE/MAX, Redfin and Wells Fargo, have announced layoffs in recent months totaling thousands of jobs. Industry analysts are projecting the cuts could eventually be on par with what was seen during the housing crash of 2008"

The latest fantasy is that there is no subprime this time around and no supply glut. Any blind man can see that in-process supply (lower pane) is higher now than in 2008. As far as subprime goes, it's all been hidden behind the veil of the shadow banking system which emerged from the ashes of 2008. Instead of banks making subprime loans, specialty mortgage companies make subprime loans using money borrowed from banks. This way banks can pretend they are lending to solvent entities.

Then there is the Fed-induced Emerging Market currency "Doom loop", now that the entire world is being forced to over-tighten in lockstep with the Fed.

Nevertheless, Fed bailout remains a predominant fantasy. Unfortunately, the Volcker gambit ensures that Powell will not be deterred by an EM meltdown.

At this point in 2008 the Fed was ALREADY easing:

None of this risk is priced in yet, especially when it pertains to the soaring dollar and soaring bond yields:

"Fourth-quarter S&P 500 earnings will face an approximate 10% headwind from the stronger dollar, in addition to other issues like soaring input costs"

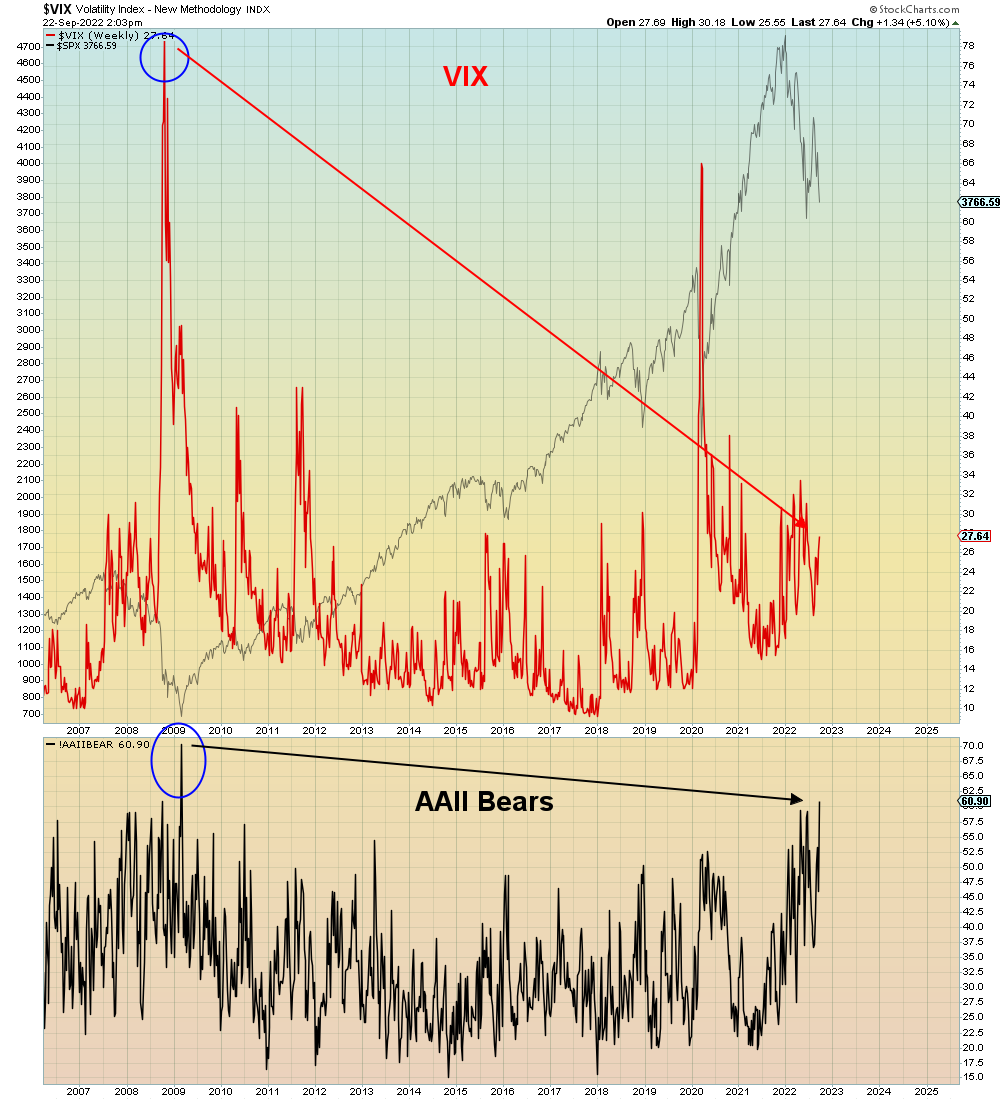

The equity risk premium which measures the stock market yield vs. Treasury bond yields has collapsed down to 2008 levels. Signaling "More Bear Market to Come":

“There is no alternative” (TINA), has completely evaporated with the rise in interest rates"

"The Equity Risk Premium has contracted since the market peaked back on Jan. 3. Using history as a guide, this is highly unusual, since it typically needs to widen by +425 basis points, on average, before bear markets come to an end"

The S&P 500 is now testing the 200 week moving average, which historically has been a critical bear market level. Below that level, the last two bear markets accelerated both in % decline and duration. And then investors were informed far too late that the economy was officially in recession. Which is similar to now when economists are pretending the economy is not already in recession.

Below we see that from the Y2K top it took until 2013 to break out to new all time highs. Well over a decade of lost returns.

To now believe that Powell's Quixotic Volcker gambit will succeed at the zero bound is a fool's errand of the highest order.

The market is on the cusp of worst three quarter return for the Nasdaq since 2008.

The market is technically oversold, therefore violent brief rallies are to be expected. However, the largest part of the March 2020 decline took place AFTER the market was oversold. In addition, investors should beware that the market was limit down in March 2020 when the Fed restarted QE. File that under careful what you wish for.

As we see below, GDP and interest rate predictions have completely reversed since the beginning of the year. MASS complacency is borne of mass confusion.

In summary, the Volcker gambit is a disaster. The ubiquitous belief that this is the 1970s deja vu will ensure this is the hardest landing since the 1930s.

Indeed.