Today's pundits never tell the full truth because they're afraid of scaring their audience away. So instead they equivocate and spread mass confusion. They NEVER weigh one risk over another and come down on the side of full bearish. Full bullish for over a decade is fine. But full bearish is never acceptable. Which is why the public have been led to believe they can ride out any amount of economic dislocation in stocks. Yet they never question these fairy tales because they're now addicted to baby talk. They have an overwhelming need to be lied to continuously so they can avoid financial PTSD. Hence they will be fed financial pablum until their centrally managed financial Disney World explodes with no warning.

At this latent juncture, the Fed is totally out of control. Six months ago they believed inflation was transitory, yet now they believe this is 1978 all over again. Powell desperately wants to be the new Volcker - a central banker who was vilified at the time, but later venerated for having the intestinal fortitude to "stamp out inflation". Because what could be worse than inflation?

Total global asset meltdown that's what. You see, what all of today's pundits have in common is that they don't understand the rules of Japanification. First and foremost a central bank must never over-tighten and cause an out-of-control asset crash. Why? Because they don't have the monetary tools to get it back under control.

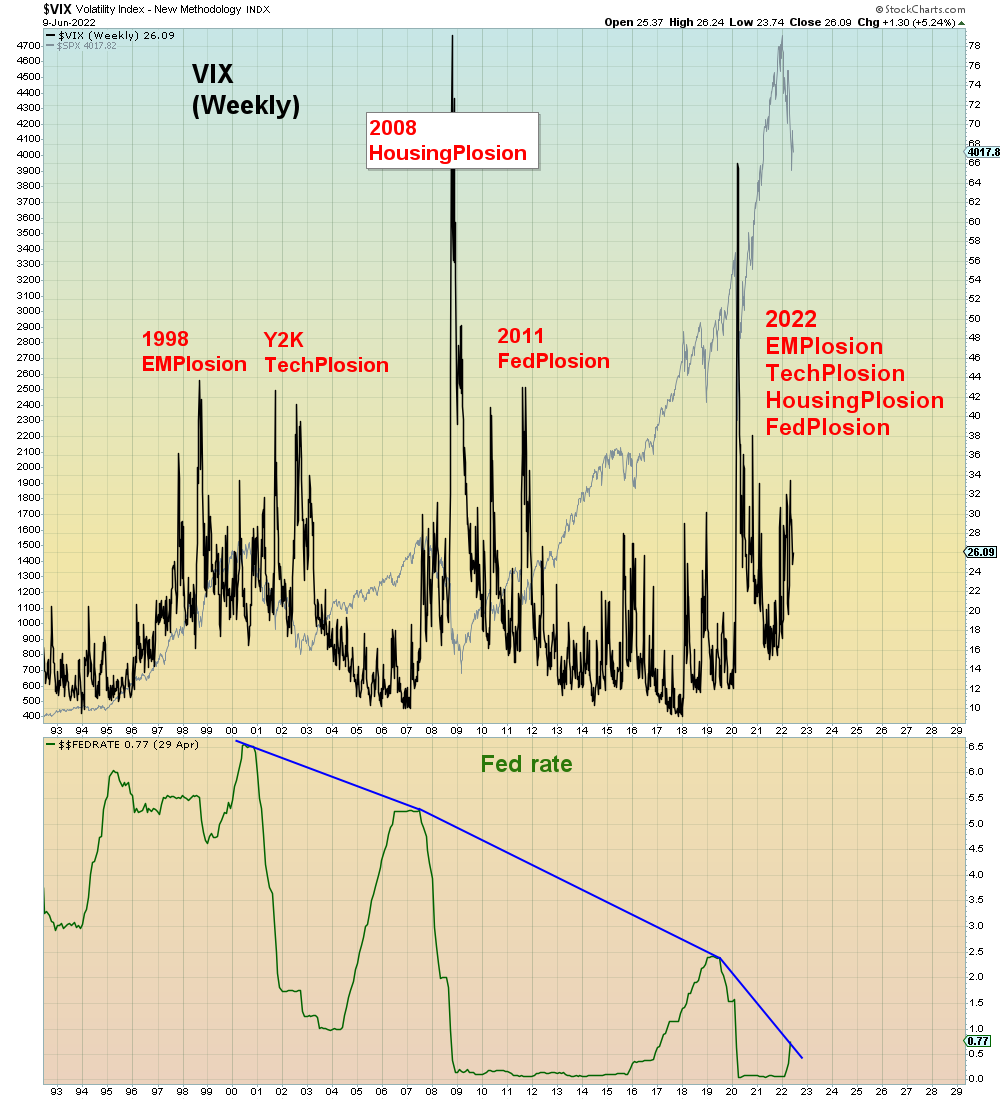

The Fed currently has .75% dry powder. Likely going up another .75% to 1.5% on Wednesday. Still, that's not nearly enough to offset a financial meltdown. In 2000 and 2008 it took 5% interest rate reduction to halt the recession. So all the Fed has now is their balance sheet. But balance sheet expansion only works if markets are not in total meltdown mode. It worked great in 2020 because the Fed bought in size early in the crash and aggressively increased their bond buying on a daily basis. That's why it only took six months for the market to reach a new all time high. Conversely, back in 2008 the Fed made the EXACT SAME policy error they're making now by focusing on inflation instead of the market meltdown. So what happened then - stocks entered Death Valley and took four months to find a LOW much less a high. Then it took SIX YEARS to make a new all time high. Again, that's with the help of a 5% rate reduction. This time around, there will be a bigger crash followed by a far weaker financial and economic recovery. And there will be tremendous societal rage when the stoned zombies are awakened from their narcoleptic coma.

Here is another problem that NONE of these acid trippers have figured out - you can't properly measure "inflation" as a one year rate change coming out of a pandemic when commodities collapsed to a five decade low. Any blind man can clearly see that oil is LOWER than 2008, so how could inflation be the worst since 1980?

Gas prices adjusted for wages (lower pane), are currently LOWER than half the years SINCE 2008.

The greatest source of inflation is due to corporate profiteering. Something the Fed has no control over.

Here we see corporate profits over wages:

Adding to this epic buffoon festival, it's only fitting that the financial stress index is now positively correlated with consumer sentiment for the first time in history. Why? Because as the economy implodes, stoned gamblers have been conditioned to front-run collapse. On the presumption of imminent bailout.

As things get worse, their complacency increases.

No surprise, gamblers are now trapped by moral hazard. They've been well trained to double down on risk and wait for their bailout. Sadly, no one has told them this time it's not coming. The Fed has mistaken their complacency as a sign to continue tightening.

The irony can't be overlooked. Both sides totally misreading the other, NONE bright enough to figure it out.

ALL of this insanity should be very obvious, however nothing is obvious in an Idiocracy that believes printed money is the secret to effortless wealth. It should have been obvious a long time ago after the Dotcom collapse and the housing crash both PROVED that we can't continually borrow our way out of a debt crisis by further lowering interest rates each time. Eventually that gambit fails at the zero bound, as Japan and China have found out the hard way.

They've learned their lesson. Which is why no surprise BOTH Japan and China are in easing mode right now. China, also because they are driving their economy straight into the ground using their patented "ZERO Covid" policy. The most populous country in world history is attempting to have zero cases of COVID. It doesn't get any more idiotic than that. Which is why we will CONTINUE hearing about serial lockdowns and re-openings until their economy EXPLODES bringing ALL Emerging Markets down with them. Which is the next event "no one" sees coming.

All of which explains how the Fed now finds themselves tightening monetary policy at the fastest pace in three decades in a confirmed bear market AND a nascent recession. When for most of the past decade they were continually SUPPORTING markets during expansion and bull market.

TOTAL INSANITY.

It's all fun and games until someone loses an everything.

And NEVER gets it back again.