What all bulls need to learn the hard way is that in Ponzi markets there is no strength in numbers...

A head and shoulders top is now clearly visible in Semiconductor stocks, Internet stocks, and the World ex-U.S.

As we see via semiconductors below, the left shoulder which took place in Q1 2021 marked the Gamestop pump and dump and the top for Emerging Markets, IPOs, SPACs and Ark ETFs. During that selloff the hedge fund Archegos exploded.

The head took place in late Q4 2021 and marked the top for all of the major U.S. averages. That was the beginning of the global bear market. As we see below, the first leg back down to the neckline saw the largest breadth collapse in Nasdaq history (bottom pane). And the bear market low saw the FTX explosion.

Which brings us to the right shoulder. What I call "System Test 3.0".

The high yield spread which is a proxy for risk appetite is highly compressed as it was pre-pandemic crash.

The left shoulder for internets goes back to March 2020.

The left shoulder for the World ex-U.S. is the same as it is for the Internets above. March 2020.

My Geometric index equal weights the largest cap Tech stocks in the market. On the left shoulder these stocks were consistently above the 200 dma. On the right shoulder, they are consistently below the 200 dma. They have become consistently more overbought on Momentum (MACD) all the way down.

These are basic facts that bulls are ignoring.

The Adani crisis started on the right shoulder and is only the very beginning of meltdown for Indian markets.

Bitcoin became extreme overbought on the left shoulder, now it's imploding again on the right shoulder.

Bulls never gave an explanation as to why markets rallied into the pandemic lockdown.

This time, they will have even less explanation as to why markets rallied into a global depression.

In summary, only someone with zero commonsense could trust these markets. Hence, they are largely unquestioned.

The bullish thesis is that all younger people will get wiped out due to their misallocation of capital, to the sole benefit of older generations doubling down on their Ponzi investments. In other words, no generation in U.S. history has been fooled as often as this one...

It took ~15 years but over time retail investors have totally forgotten the pain of 2008. After the 1930s, the generations that endured that pain NEVER forgot, even decades later.

Today's financial media is wholly derelict in their duties, as they have been for decades amid an ever-growing debt bubble heading for inevitable disaster. The individual investor has now been throw to the wolves of Wall Street. What was Occupy Wall Street a decade ago is now trust the fairy tale of the never-ending financial/economic cycle - the belief that the pandemic bear market lasting one month corrected the longest bull market in history.

Below is what the ratio of bull market to bear market would look like if that were actually true. The 2009-2020 bull market would be ~130x longer in months than the bear market that followed:

Gen-Z is now totally under the bus. Two years ago the Gamestop pump and dump frenzy brought record newbies into the market where they were unceremoniously obliterated.

The media called it "The democratization of markets". They even made a Netflix documentary about it called "Eat the Rich". It turns out the rich were not the ones who got eaten. It was a totally false narrative and yet largely unquestioned.

Millennial investors are in the 30-45 age range and they are now trapped in the housing market. They didn't believe all of the stories that emanated from 2008 about the risk of housing bubbles, so they went ahead and made the same mistake a mere 10 years later.

So far, global housing prices - with some regional exceptions - are holding up, but sales volumes have collapsed. A precursor to major price decline.

Soon the combined impact of $2 trillion student loan debt, epic housing collapse, stock market wipeout and mass layoffs will land on them like a ton of bricks.

The good news is that younger people who get wiped out by this global Ponzi collapse can recover from this debacle and eventually get themselves back on track financially. Time is on their side. The older generations who SHOULD know better than to trust Ponzi markets, don't have that kind of time.

So far retirement gamblers are doing the exact same thing GEN-Z dunces did - they are "HODLING" meaning holding on with the belief that markets will come back. They look around and see other generations making the exact same mistakes they made in Y2K and 2008 and just assume they alone will be spared the consequences of the pandemic bubble.

Which is where it gets interesting:

As things go on the domestic side of markets - a case of survivor bias, so it is on the global markets. A massive case of survivor bias. There is this recurring false belief that U.S. markets are a safe haven from global dislocation.

Global central bank tightening has been collapsing Emerging Markets since 2021 while capital retreats to the safety of the U.S. The belief is that they will continue to implode to the benefit of the U.S. We saw this same cycle play out between 2018 and 2020. And it all imploded in this EXACT same timeframe.

It's the "It can't happen to me" trade on a global scale:

Ironically, just as the financial media were lying to newbie investors two years ago during the Gamestop debacle, so too are they lying to older investors right now.

Why? Because in the end media bulls and Wall Street analysts will be spared the consequences of their specious advice.

But, at some point it's not the liar who is the problem, it's the person willing to believe the liar who is the real problem.

The end of cycle fool's rally is ending, as it appears the last fool was finally found. Since the start of the year bullish pundits have been rounding up useful idiots to feed into the Dow Jones hopper, however the almighty Dow Jones Illusional Average has now given up six weeks of gains in three days. Amid record retail investor inflows...

Over the course of the past year, the bullish thesis has shape shifted from hyperinflation to inflation, stagflation, soft landing, and now no landing, meaning no inflation AND no recession, the delusion du jour. You have to be brain dead to believe it, hence it's now Wall Street consensus:

The "No landing" fantasy was fabricated in order to allay investor concerns that an ever-more hawkish Fed will implode the economy, as they have every other time in history. So, the *new* fairy tale is that Fed over-tightening can bring down inflation while the economy continues to grow robustly. It's abundantly clear by this level of end of cycle denial that the latest uptick in social mood has completely fried the brains of today's financial punditry.

Nevertheless, one must ask the critical question, why is Fed tightening causing the economy to reaccelerate at the end of the cycle? The main reason is because investors are front-running the Fed, causing financial conditions to ease. Consider that financial conditions have now gone nowhere for the past year, despite the fact that the Fed has raised rates MORE than they did back in 2007. However, the problem is that wages are lagging inflation, meaning "real" (inflation-adjusted) wages are negative. Therefore, consumers are increasing their debt load in order to keep up with inflation. This is manifesting in sky-rocketing credit card balances AND delinquencies. So sure, this is an "inflationary" moment, however it is far from sustainable. The inflation mentality has led consumers to increase debt, on the belief that they can grow their incomes at a pace that will offset the rising debt burden. But that's not what is happening.

Financial markets are ignoring what's happening in the underlying economy:

Ironically, this same sequence of events played out in 2008: An end of cycle rally attended by an uptick in consumer sentiment, and a Fed totally concerned with inflation. A massive policy error, and then an unforeseen collapse.

"On the morning after Lehman Brothers filed for bankruptcy in 2008, most Federal Reserve officials still believed that the American economy would keep growing despite the metastasizing financial crisis"

The transcript for that meeting contains 129 mentions of “inflation” and five of “recession.”

What does all of this have to do with casino gambling? Pretty much nothing, since money has to go somewhere hence there will always be a bullish investment hypothesis on offer, no matter how moronic. Investment managers do not get paid to sit in cash.

Another popular investment hypothesis championed by Tom Lee of Fundstrat is that fundamentals no longer matter, all that matters is the flow of funds. There is only one problem with that theory - it's not working. Not for lack of trying mind you:

"Individual investors have been snapping up stocks at the fastest pace on record as U.S. equity markets have charged higher to start the year. Over the past month, retail investors funneled an average of $1.51 billion each day into U.S. stocks, the highest amount ever recorded"

It turns out that if you pay a trillion dollars for a brick, its valuation doesn't increase, unless you find someone else who is even dumber. Generally speaking, these are not the types of people who are sitting on piles of cash.

As of Tuesday's close, the Dow has given up all gains for the year.

Meanwhile, this decline is still tracking the Feb/March 2020 crash week by week. The difference being, that one was attended by global bailout whereas this one is attended by global tightening.

Which means that investors will get to experience the excitement of real investing without a Fed safety net. Which will test the predominant hypothesis that printed money is the secret to effortless wealth.

Central banks bailed them out of pandemic, so they went ALL IN at the end of the cycle. THE END.

I've been recalcitrant in my blogging lately. Bullish malaise has apparently comatized even the most bearish of bloggers. Something about collapsed volume and volatility will do that. However, next week is the anniversary of the pandemic crash three years ago AND the start of the war in Ukraine one year ago. So, it would be highly ironic if all of this widely ignored risk all exploded in the same timeframe. They didn't see it last time, and clearly they are clueless this time around as well. Three years ago next week, at the start of the crash, the weekend Barron's lead story claimed "It's STILL A Bull Market Everywhere You Look". It was already too late to get out.

Feb. 21st, 2020:

Since the Fed hiked rates by 1/4 point at their meeting two weeks ago, the economic data has all run on the side of hot. And yet gamblers have been totally unperturbed by rising rate risk. To paraphrase Zerohedge: rising rates means rising recession risk, rising crash risk, and therefore rising chance of rate cuts. To get the rate cuts, you have to first get the rate hikes, the recession, and the crash. Meaning the bullish hypothesis is the same as the bearish hypothesis. Crack dosage being the only difference.

I would remind everyone at this juncture that it wasn't emergency rate cuts in March 2020 that saved markets and it wasn't the restart of QE - those were both limit DOWN events. What saved markets is when the Fed panicked and took over the Treasury bond market. Something that is so far off the radar right now, there is not the slightest inkling that it will happen. Whereas back in 2020, the Fed was already in rate cutting mode and QE mode, due to the Repo crisis.

In other words, the exorbitant Fed bailout that took place three years ago is the reason why inflation is running too hot today, and it's also the entire premise of the bullish hypothesis. We all agree a bailout is inevitable, but from what level?

Not this one.

This week's CPI ran hot, but that also didn't faze markets. Year over year, CPI dropped from 6.5% to 6.4%. That's after 18 1/4 point rate hikes in one year - more than took place in the three years leading up to the 2008 GFC. As we see below, back in 2007 when the Fed pivoted, the CPI shot up 4%. If that were to happen now, the CPI would blow through 10%.

Which means the Fed can't pivot until there's a crash. Which fortunately is the bullish hypothesis anyways.

Everything the Fed is doing right now is making T-bonds more attractive relative to stocks. They're actively raising rates which compresses the forward P/E multiple, they're slowing GDP growth and profit growth, and yet stocks remain record overvalued relative to bonds. Why? Because the inflation premium is still in the market. We are a binary event away from repricing that assumption out of the market, at which point it will be the end of the cycle and stocks will be bidless.

All because investors believed that THIS Fed could keep interest rates, demand, profits, equity multiples, stocks, housing prices all at record highs.

While bringing inflation down.

For the first time in World history.

Chart gallery:

Today's technicians are TOTALLY clueless. This right shoulder is a mess compared to the left shoulder.

Aussie disconnect deja vu of Feb 2020:

Dax deja vu

In summary, the most bullish thing I can say is that as of this moment, it's still a bull market everywhere you look.

We have now reached the lethal juncture predicted by hedge fund manager Hugh Hendry - the stock market is now inversely correlated to the economy. The worse the reality of the economy becomes, the greater the anticipation of imminent dramatic bailout...

The UK has both the worst performing economy in the G20 and the best performing stock market in the world.

Where to begin...

Worst week for stonks since December. First down week for the Nasdaq in 2023.

This week, Gallup surveyed Americans and found that the greatest percentage feel their finances have imploded year over year since 2009:

In the same week we got that news, Fed futures have started to price in a 6% Fed rate by September. But then we found out that may be "too low".

No one questions this insanity. Monetary policy operates on a lagged basis, so traders will learn far too late the Fed has already over-tightened on interest rates. Their balance sheet is a whole other story. No one questions that at the current rate of run-off the Fed balance sheet will take FOUR YEARS to return to the pre-pandemic level. Meanwhile, interest rates are 3x higher than pre-pandemic.

Below, I call this the moral hazard death spiral:

Investors keep front-running Fed bailout, and therefore the Fed must keep raising interest rates imploding the economy. Monetary policy is lagged, therefore the dunces at large don't question it.

Consider that at a 6% target rate, we now have the highest bullish sentiment since the market's all time high in December 2021.

I ask the bulls, why did you wait for 6% to get so bullish?

What was wrong with 3%?

But many ask, why would this death spiral all of a sudden end now? Why can't death spirals last forever?

That's a good question - Can the market keep stair stepping lower or does it reach an acceleration point and explode?

For that we must rely upon Elliott Wave Theory, so here's the short lesson on EWT: Basically, the fundamental tenet of EWT is that markets are driven by emotions - greed and fear. Sure there other factors involved in market performance, however, at the extremes greed and fear are the dominant forces.

Many people believe that as long as retirement investors keep ploughing money into stocks regardless of valuation, then the market will just keep going higher. Like a Ponzi scheme in over-drive. There's only problem with that theory, it didn't work in 2022. 401k investors remained on auto-pilot and the market went down -20% at the lows.

EWT is not complicated, and it's not financial voodoo as most fundamentalists call it. On the other hand, guessing where corporate profits will be a year from now when the majority of corporations have suspended forward guidance due to "lack of visibility", is a fool's errand of the highest order, hence it's standard practice. It gets far less reliable when the market is negatively correlated to the economy.

Therefore, according to EWT, we look for indications that speculative froth is running high. On crack. And about to implode. And then we look for technical confirmation in the form of pattern recognition. Which is something that today's technicians assiduously avoid. Why make it so easy? Why not leave room for imagination and speculation?

Do we have any indication that speculative froth is running high?

"A speculative frenzy after Fed Chairman Jerome Powell spoke last week helped drive record trading in call options Thursday"

But the record volume in call options on stocks last week may also be the sign of a medium-term peak in speculative behavior"

RECORD speculative frenzy. CHECK.

Next, we look around for some technical indicators that point to momentum rolling over.

For example, Microsoft peaked three years ago THIS WEEK ahead of the pandemic. And we see it made a massive reversal this week as well:

Here we see semiconductors rolling over at the neckline which was formed beginning in January 2021, during the first meme stock pump and dump.

Emerging Markets are sticking to the annual rollover schedule that has been in place since 2018:

In summary, if you believe Jim Cramer, you are doomed.

And, you deserve your certain fate.

That is Darwin's Law and it's the only way we will raise societal IQ.

When enough people believe a lie, then it becomes the truth. For a while...

The reason the Madoff Ponzi scheme went on so long is because investors never questioned it. They enjoyed their outsized returns and therefore didn't ask questions. Prior to 2008, there was never a mass exodus from the fund so there was no prior "discovery" of insolvency. The inbound money from new investors was always sufficient to pay out the few people who exited his fund. In addition, his fund did not trade on an exchange so there was no way to know its true price and therefore no way to know that the Net Asset Value was zero.

A similar dynamic is taking place in today's Ponzified stock market. No one questioned the outsized returns, so it has remained solvent. Due to the aging population there hasn't been a mass redemption event since 2008. In March 2020, retirement investors held on through the panic phase which only lasted a few weeks. Unlike Madoff's fund however, it won't take a mass redemption to reveal this market's true underlying value. All it will take is an illiquid market and margin calls to discover "true value". The sequence of events leading up to this juncture have essentially created a bidless market, because stocks are now massively overvalued relative to bonds, due to the inflationary mentality. When inflation turns to deflation and recession, then stocks will be MORE overvalued relative to Treasury bonds.

The chart below shows the "Equity Risk Premium" (ERP) which is the yield on stocks minus the yield on Treasury bonds. Here we see that in past bear markets/recessions the ERP rose because stocks fell faster than profits AND interest rates fell as well. However, this time interest rates have been rising and profits are now falling. Which means that stocks have become MORE overvalued during this decline. Which is why David Rosenberg says stocks could easily drop -30% from these levels:

"The stock market bottoms 70% of the way into a recession and 70% of the way into the easing cycle"

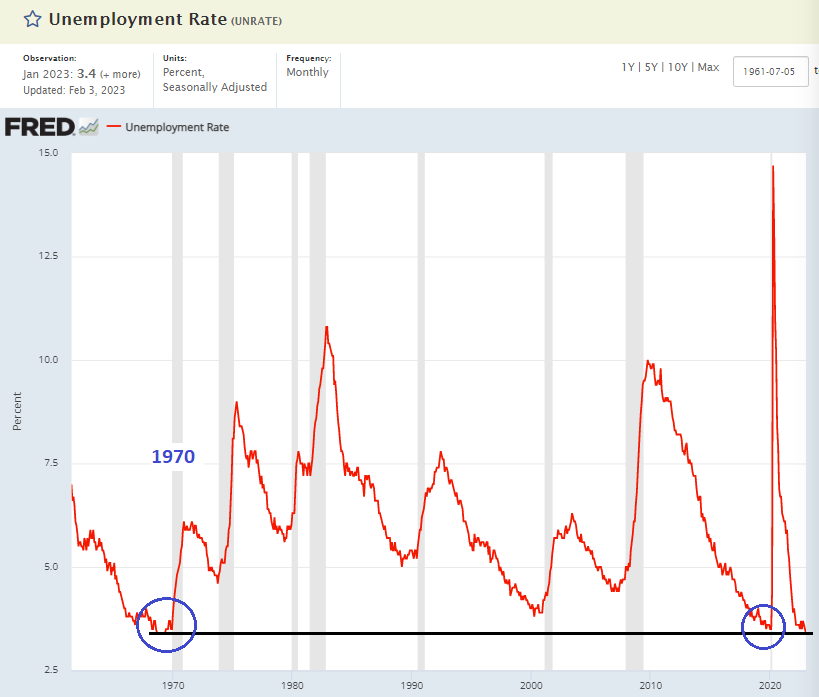

"Recessions don't happen when the unemployment rate is at a 53 year low".

However, it just so happens that TWO recessions took place when unemployment was at a record low. One was exactly 53 years ago in 1970 and the other was three years ago in 2020. In my last post I showed that in an inflationary economy, the jobs market is lagged by so much that it rolls over well AFTER recession has started. Currently, due to pandemic mass layoffs and early retirements, job openings relative to job seekers are still at an all time high.

More importantly, REAL wages are deeply NEGATIVE. So you don't need a lot of unemployed people to start a recession, all you need is a lot of broke people.

Of course the problem with saying that stocks will go down a specific 30% based upon historical baselines, is that it's an impossible prediction to make. Until we get down there, we won't DISCOVER how many Bernie Madoffs have been going into business since 2008. So far, we've seen the spontaneous explosion of hedge fund Archegos in 2021 which was over-leveraged to Chinese Tech stocks. In October 2022 FTX Crypto exchange spontaneously exploded due to the Crypto decline. And just recently Indian conglomerate Adani went into full scale meltdown during a global rally. If Ponzi schemes can implode in a massive rally, imagine what is waiting for these markets on the other side of a global crash. People will be shocked at the level of criminality that has accumulated in these central bank Disneyfied markets.

In summary, from a long term investor's standpoint, there has never been a worse time in modern history to be fully invested in stocks. If someone is in their 20's then sure they will recover. But for anyone over the age of 40, this event will be cataclysmic to their retirement plans.

When my wife asked me recently what should everyone do, short the market? My response was no, most people should never short anything. What they should do is spend less and save more. Because that's what the Chinese and Japanese do now that their Ponzi markets have exploded.

For most people - especially passive investors - that is the ONLY true retirement now.

Not betting their life savings on Ponzified markets.

This will be the first RISK ON recession in world history...

Here we see the Baltic Dry Index and Global Dow. Every other time the BDI was at this level, global risk markets were selling off.

This week, global stocks are back near their all time high.

Which means we are VERY LATE in the Ponzi cycle and all warnings have been totally ignored.

The standard narrative for the past year is that the Fed kept interest rates too low for too long which caused rampant inflation. This narrative is totally unquestioned and yet a total fabrication. During the 2008 Global Financial crisis, the Fed lowered interest rates from 5% to 0% and kept them at 0% for SIX YEARS. In March 2020, the Fed lowered interest rates by 1.5% to 0% and kept them there for two years. Subsequently, they have raised interest rates to 4.5% which is 3x the pre-pandemic level. If interest rates were causing inflation then why hasn't inflation come back down to the pre-pandemic level? It's because in the meantime, they have only brought their balance sheet down by a minor amount (see chart below).

This massive policy error has caused markets to remain in RISK ON mode throughout the end of the cycle. Which has never happened before in market history. Usually the prospect of rate hikes and a recession have caused markets to de-risk and de-leverage. Not this time. Throughout the past year, investors have been continually buying every dip in order to front-run what they view as the inevitable bailout. However, the irony is that THEY are the reason why the Fed can't stop raising interest rates. They are the reason this will be a depression instead of a recession. Granted, they were conditioned by Fed bailouts.

In other words, via misallocated capital, investors have created their own illusion of solvency which is now totally divorced from the economy. Friday's blowout jobs number caused the bond market to finally price in a 5% rate by May. Pundits can rationalize the seasonality of that massive jobs print all they want, but the fact remains that the Treasury market is starting to believe the Fed when they say that interest rates are going higher. However, risk markets are STILL in total denial.

As a measure of misallocated risk capital, here we see the high yield spread is HALF the level it's usually at when the leading indicators are at this level.

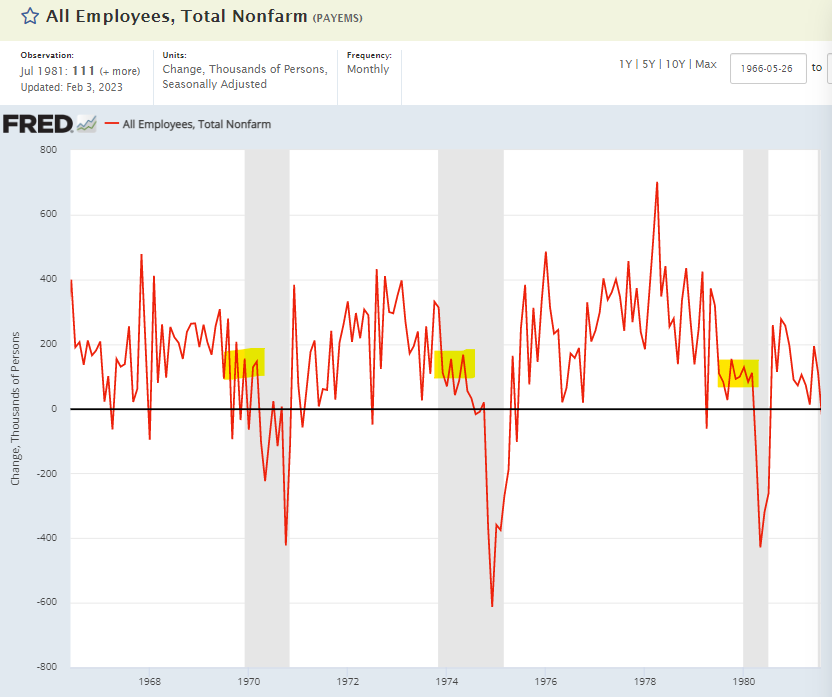

Those who believe the U.S. can't go into recession when the jobs market is still strong, don't know their history. During the inflationary recessions of the 1970s, the jobs market always rolled over long AFTER recession had already begun:

1970-1980:

Sky-rocketing credit card debt and interest rates shows that consumers for now still maintain an inflationary mindset. However the belief that this can continue indefinitely is totally fantastical.

Credit card carrying costs:

The rest of the world is making the same massive mistake of keeping risk markets elevated via their bloated monetary balance sheets while imploding their economy.

This week, Europe's market round-tripped back to the all time highs of a year ago right before the Ukraine war:

All of which means that bulls are now trapped by their own greed and hubris.

The dominoes have been falling for two years now since the February 2021 melt-up which imploded IPOs, SPACs, Meme stonks, and Emerging Markets.

This is a two year head and shoulders top as indicated by "Momentum stocks" which is a basket of the top performing stocks.

The Adani meltdown is merely a symptom of a much larger problem:

The TOTAL Ponzification of markets. Meaning ALL return is dependent upon the next greater fool willing to provide return to exiting investors.

Soon ALL risk markets will be in Adani mode at the same time. Which will be a clusterfuck of unprecedented proportion causing dislocation and panic we have not seen in our lifetimes.

Yet.

Oil stocks rolled over hard this week. Oil is already down -40% from the March 2022 highs (not shown). Clearly late cycle Energy stocks are rolling over later in the economic cycle than they did in the last major recession:

In summary, we are very late in the Ponzi cycle. And all warnings have been ignored.

"Shares crash, hopes are dashed. People forget it's bullshit"