The reason the Madoff Ponzi scheme went on so long is because investors never questioned it. They enjoyed their outsized returns and therefore didn't ask questions. Prior to 2008, there was never a mass exodus from the fund so there was no prior "discovery" of insolvency. The inbound money from new investors was always sufficient to pay out the few people who exited his fund. In addition, his fund did not trade on an exchange so there was no way to know its true price and therefore no way to know that the Net Asset Value was zero.

A similar dynamic is taking place in today's Ponzified stock market. No one questioned the outsized returns, so it has remained solvent. Due to the aging population there hasn't been a mass redemption event since 2008. In March 2020, retirement investors held on through the panic phase which only lasted a few weeks. Unlike Madoff's fund however, it won't take a mass redemption to reveal this market's true underlying value. All it will take is an illiquid market and margin calls to discover "true value". The sequence of events leading up to this juncture have essentially created a bidless market, because stocks are now massively overvalued relative to bonds, due to the inflationary mentality. When inflation turns to deflation and recession, then stocks will be MORE overvalued relative to Treasury bonds.

The chart below shows the "Equity Risk Premium" (ERP) which is the yield on stocks minus the yield on Treasury bonds. Here we see that in past bear markets/recessions the ERP rose because stocks fell faster than profits AND interest rates fell as well. However, this time interest rates have been rising and profits are now falling. Which means that stocks have become MORE overvalued during this decline. Which is why David Rosenberg says stocks could easily drop -30% from these levels:

"The stock market bottoms 70% of the way into a recession and 70% of the way into the easing cycle"

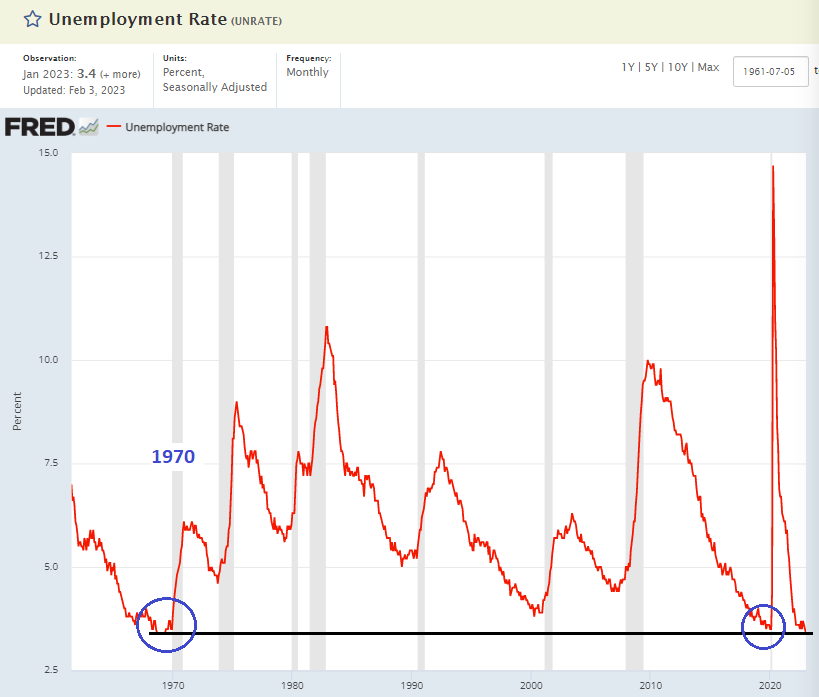

Also, on the topic of "fundamentals", this week when asked if she saw a recession on the horizon, Treasury Secretary Janet Yellen replied:

"Recessions don't happen when the unemployment rate is at a 53 year low".

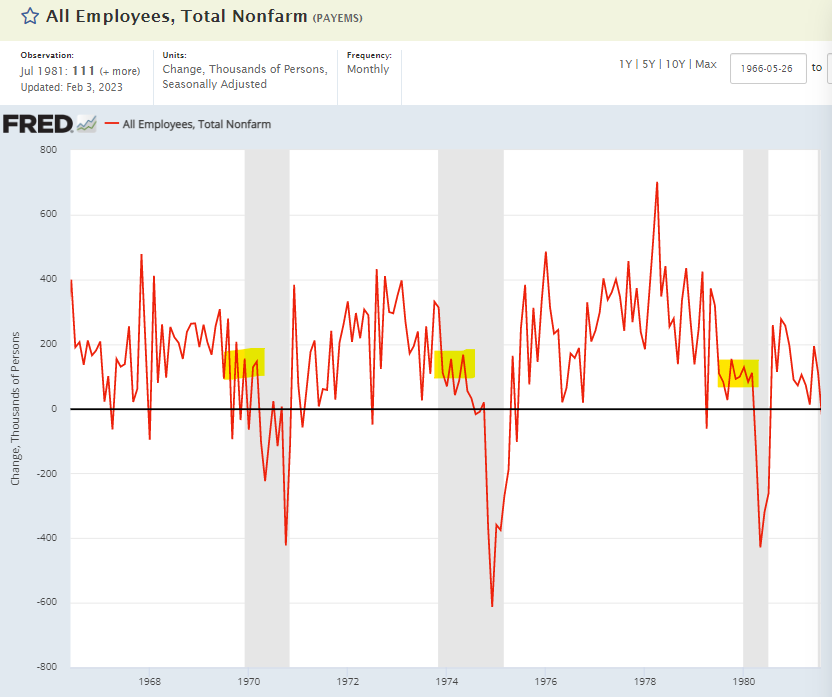

However, it just so happens that TWO recessions took place when unemployment was at a record low. One was exactly 53 years ago in 1970 and the other was three years ago in 2020. In my last post I showed that in an inflationary economy, the jobs market is lagged by so much that it rolls over well AFTER recession has started. Currently, due to pandemic mass layoffs and early retirements, job openings relative to job seekers are still at an all time high.

More importantly, REAL wages are deeply NEGATIVE. So you don't need a lot of unemployed people to start a recession, all you need is a lot of broke people.

Of course the problem with saying that stocks will go down a specific 30% based upon historical baselines, is that it's an impossible prediction to make. Until we get down there, we won't DISCOVER how many Bernie Madoffs have been going into business since 2008. So far, we've seen the spontaneous explosion of hedge fund Archegos in 2021 which was over-leveraged to Chinese Tech stocks. In October 2022 FTX Crypto exchange spontaneously exploded due to the Crypto decline. And just recently Indian conglomerate Adani went into full scale meltdown during a global rally. If Ponzi schemes can implode in a massive rally, imagine what is waiting for these markets on the other side of a global crash. People will be shocked at the level of criminality that has accumulated in these central bank Disneyfied markets.

In summary, from a long term investor's standpoint, there has never been a worse time in modern history to be fully invested in stocks. If someone is in their 20's then sure they will recover. But for anyone over the age of 40, this event will be cataclysmic to their retirement plans.

When my wife asked me recently what should everyone do, short the market? My response was no, most people should never short anything. What they should do is spend less and save more. Because that's what the Chinese and Japanese do now that their Ponzi markets have exploded.

For most people - especially passive investors - that is the ONLY true retirement now.

Not betting their life savings on Ponzified markets.