Many new traders wonder why the market would be up in a week when there is a triple rate hike AND confirmed recession. When traders buy weekly put options on the anticipation of bad news then the market makers on the other side of the trade hedge their long put position by shorting the market. This causes the market to dip ahead of the bearish event. However, once the event passes, then a combination of time decay and price movement causes those expiring options to lose value. Market makers reduce their hedges by buying back stock. This creates a feedback loop towards the end of the week as the stock buying pushes more of the put options out of the money. Ironically, bearish option traders create the rally.

However, it's not a long-term phenomenon. It has its greatest effect during central bank meetings, monthly opex (third week), and of course the end of the month during window dressing.

As we see, this three month pattern is very similar to the one ending in March. That was a bull trap, and I suspect this is a bull trap as well. When the March rally ended, the market fell -20% in six weeks.

If the cycle repeats then the market will be in confirmed bear market territory.

For all of the fake excitement over Amazon earnings, that stock has the same form it had the last time it imploded.

This week, despite Fed tightening, yields broke to new lows:

The global Dow, fourth lower high:

Metals and mining stocks, a very similar bounce, this time off of key support:

No sign of capitulation

March and July are the only two up months for the Nasdaq in 2022.

The summer rally is very likely over. Now comes the month that has seen the biggest crashes since 2008 (pandemic aside).

In summary, the U.S. is in confirmed recession ahead of Europe, China and the rest of the world.

Which means that hot money will now exit U.S. markets at the speed of yield collapse.

Back at the market top in 2007 Wall Street was making all manner of excuses for investors to stay the course. They are doing the same thing right now. Trying to keep the sheeple from bolting...

"When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance"

THIS is how the era of continuous monetary bailouts and extreme moral hazard was doomed to end - with an Idiocracy now questioning the definition and even the possibility of recession while the walls are closing in on them from all sides.

This chart shows that the two quarter moving average of GDP decline now exceeds Y2K, which was an "official" recession.

Most young investors are of the belief that the 2020 v-bottom recovery was typical - a four week recession and bear market followed shortly after by new all time highs. CNBC and Zerohedge pundits apparently don't have any recollection earlier than December 2018 which was the last time the Fed successfully "pivoted" from tightening to neutral and the market took off. The difference of course is that this time the economy is now in a confirmed recession. Stock valuations are higher now, the housing market is imploding, the car market is imploding, and inflation is at a 50 year high. Meaning consumers are TOTALLY tapped out. Which is the message coming through this quarter's earning announcements, however CNBC and Wall Street have done a great job of putting lipstick on the pig. The mantra of the day is: "Not as bad as feared". Meaning the company "beat" collapsed expectations. Bearing in mind that most of the guests on CNBC are money managers who have to put money somewhere. So all they care about is which stocks will go down the least in a recession. Apparently they've forgotten the lesson from Y2K.

Back in the Y2K bubble, first the profitless junk stocks imploded. When that happened money rotated to the mega cap stocks: Microsoft, Intel, Cisco, and Dell on the assumption they were Tech safe havens. As a result those stocks became massively overvalued as growth slowed. And then those "safe havens" imploded. The same thing is happening now.

Meanwhile, mega cap Tech stocks remain top holdings in every portfolio.

Apple is an excellent example of Wall Street smoke and mirrors. We were told the company "beat" earnings expectations, but profit was down -11% year over year. If you take into account CPI however, REAL profit was down -20% year over year.

In other words, it was a very bad quarter and the company is using inflation to hide how bad it was.

Despite lowered expectations vis-a-vis last quarter, Microsoft missed, Google missed and Facebook missed. Amazon took expectations down to rock bottom ahead of the quarter, and Apple covered up a year over year profit collapse with the assistance of media con artists.

"AAPL did not disappoint...easing concerns that supply chain snags and a shaky economy would ravage the tech giant’s sales"

Sure.

The CPI is hiding economic collapse in broad daylight.

Here we see real wages have collapsed -3%, the most in 20 years and more than 2008. It's fortunate that so far GDP is only down -1%. Clearly consumers are digging into savings.

There are eight weeks until the next FOMC. In the meantime, the economy will be weakening as the lagged impact of these most recent rate hikes takes effect. Meanwhile economic reports which operate on a lag will continue to show elevated inflation and economic activity while the real-time indicators are collapsing. During this lag period, Wall Street will be doing everything possible to paper over collapse with their standard end of cycle chicanery.

Pundits are already telling people that inflation has peaked and it's time to pile back into the market:

“When the Fed gets out of the way, you have a real window and you’ve got to jump through it. … When a recession comes, the Fed has the good sense to stop raising rates,” the “Mad Money” host said. “And that pause means you’ve got to buy stocks.”

Here below we can see that when the Fed stopped raising rates and began lowering them in 2007/2008, that was the period of maximum drawdown. We also see that it took the National Bureau of Economic Research a FULL YEAR to declare official recession. By that time the market was down -50%. When the Fed met at their fateful Lehman meeting in September 2008 they had no idea the economy had already been in recession for nine months.

Going into the steepest part of the decline, only 5% of Wall Street recommendations were sell:

In summary, this is a BULL TRAP of biblical magnitude.

One thing I agree with Cramer on is that the Fed is likely done hiking rates. Which means they are now going to "pivot" at a 2.5% Fed funds rate. In other words, Wall Street’s best case scenario is actually the worst case scenario. Non-normalized rates in a deep recession.

How the age of MORAL HAZARD was always going to end. With investors believing that global depression was their last buying opportunity.

I'm experimenting with a new type of blog post focused solely on market technical analysis. No major rants and no Econ data. That way I can show more charts and cut down on Twitter spam.

What we're looking for is a second overbought bull trap which will lead into the final meltdown phase.

The SPX is back to overbought and upper trendline:

The pandemic marked the apex of the largest bubble in world history - Globalization. Investors lured by the promise of virtual prosperity are now trapped between recession and inflation. Which means there is no economic or financial bailout this time around. All that's left is lethal denial. Unfortunately, what the sheeple STILL haven’t learned is that Wall Street’s entire business model is predicated upon monetizing denial…

The pandemic super bubble was the first global bubble in history. It was inflated by the largest coordinated global fiscal and monetary stimulus, without any comparison. The problem is that it was far too much stimulus. Coming out of the pandemic many pundits claimed that the pandemic unemployment programs were creating inflation. There is only one issue with that theory - those programs ended almost a year ago (September) which is when inflation accelerated. It turns out the biggest accelerators of inflation were corporate profits, commodities, and the housing bubble. The prime beneficiaries of Quantitative Easing. Once again, it was socialism for the rich which was driving inflation, not the middle class. Something to keep in mind when this hyper bubble explodes. Because this time there will be no bailout for the wealthy.

No bailout means there will be tremendous de-leveraging of the corporate sector in this impending recession. A lot of investors don't seem to know that after the pandemic, Congress removed the Fed's *special* bailout powers.

"Toomey said the deal achieved his four goals: to sweep out $429 billion in unused CARES Act funds allocated for Fed lending and repurpose the money, to shut down the four lending facilities, to forbid the reopening of those facilities, and to ban future clones of the program"

The pandemic was the first time in U.S. history when corporate debt actually grew during recession. Bulls are therefore betting this will be the SECOND recession in a row with no deleveraging. Sure.

From a valuation standpoint, during the pandemic stocks reached a record over-valuation relative to GDP. A ratio called the "Buffett indicator". As we see, prior to the pandemic stocks were bubbling back up to the Y2K record over-overvaluation level. And then the pandemic caused a breakout above that prior peak valuation. A return back to a 1:1 market cap/GDP ratio would imply a -50% drop in stock prices ASSUMING GDP does not collapse. Which is an asinine assumption. Given the attendant collapse in GDP, stocks could easily fall -75%.

That said, central banks will do everything possible to prevent true valuation. Which is why I say that stocks will ultimately become dead money, because they will not reflect proper valuations. Which is something the Japanese and Chinese have already learned the hard way.

The problem of course is that Nouriel Roubini has acquired a bearish reputation, hence he is called "Dr. Doom". Which is why many people ignore his warnings. He has always been right of course as to where this monetary orgy was heading, but it took the pandemic blow-off top to coalesce all of the risks he has warned about for years. Meaning it took a pandemic sugar rally to convince the masses to fully buy into virtual prosperity.

Make no mistake, the magnitude of this meltdown will ensure that anyone deriding Dr. Doom in the days to come, will have ZERO credibility.

In summary, U.S. gamblers are now addicted to VIRTUAL prosperity. Japanese investors were the first to learn the hard way not to trust printed money illusions. Next Chinese gamblers learned the hard way. Japan's market peaked in 1990 and China's market peaked in 2008.

What today's Fed pivot zealots don't understand is that after Y2K and 2008, when the Fed began cutting rates, the market STILL went down. The pivot was not the end of the bear market, it was the beginning.

It's very hard to make the u-turn from boom to bust, when you don't see it coming...

We're receiving glimpses of this impending horror story, but only pieces at a time. We hear about this economic implosion or that one, but no one wants to put the pieces together to assemble the impending disaster. Which makes for a con man's paradise. One in which a public wanting nothing to do with the truth finds ample con artists willing to meet their inflated demand for bullshit.

This week it's highly likely the Fed will tighten at the fastest pace since 1980 in the exact same week we get confirmation of recession. Q2 GDP Now is currently at -1.6%, the same as final Q1 GDP. The very definition of recession.

Which is why policy-makers are now attempting to redefine the standard definition of recession from two quarters of negative growth to "whatever we want it to be". As in something wholly subjective that will contain the growing sense of panic. The fact that this is an election year will in retrospect be viewed as a key factor burying a lot of people. Just as 2008 was a critical election year featuring all manner of inflated bullshit right up until the Lehman meltdown.

Fortunately for policy-makers, investors are now fully conditioned to believe that recession is a buying opportunity which is why complacency is rampant. In the same week we are witnessing what will likely become the greatest economic policy error in modern history, the Fed's Financial Stress Index just reached an all time low. With a stress index like that, who needs enemies?

Two quarters of negative GDP and a flattened yield curve, but recession is not inevitable yet. The 2s/10s yield curve has successfully timed every recession in the past 30 years.

Government economists have successfully timed ZERO recessions.

Do you know what would make a recession LESS likely? RECORD tightening during a period of extreme economic uncertainty. Because what could go wrong?

Ok, so the Fed is hellbent on burying everyone.

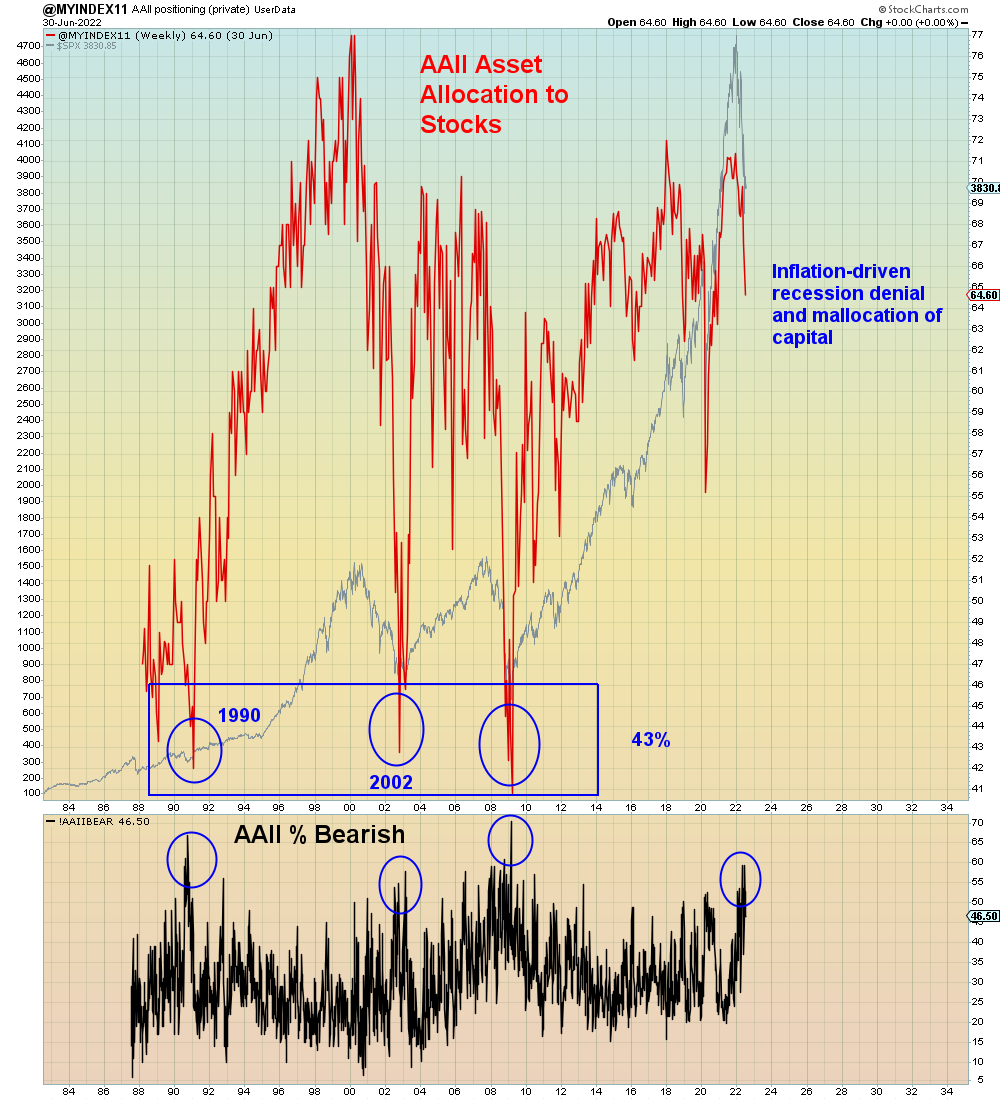

We are told that investors have "capitulated", however there is no sign of that anywhere other than in subjective sentiment surveys. The money has to go somewhere. And in an "inflationary" environment the last place it goes is cash. People don't want to buy stocks, but they are told they have to. Otherwise, they will lose to inflation.

Similarly, from a consumer sentiment standpoint, retail sales unadjusted for inflation remain high even though consumer sentiment is at record lows. People are conditioned to buy and to borrow as much money as possible. Why? Because an inflationary environment favors the borrower. Prices go higher and inflation-adjusted liabilities go LOWER. Unfortunately, in a deflationary environment, it's the opposite - prices go lower and inflation-adjusted liabilities go HIGHER. Which is the scenario we are now about to enter - an inflationary collapse. Which is arriving just as most people have been TOLD to believe that inflation is NOT transitory.

And amid all of this chicanery, economists cling to their linear economic models, which in no way can make the u-turn from inflationary boom to deflationary bust. Linear economic models are useless at the end of the cycle. However, that doesn't stop economists from using them. Today's economists are on the cusp of losing ALL credibility.

So it is that we learn about the housing market imploding. The Tech sector having mass layoffs, the car market seeing a spike in repossessions, AT&T customers not paying their bills anymore, commodity markets imploding, and yet it all adds up to soft landing.

Which gets us to the latest most popular investor narrative - rate hikes this year followed by rate cuts next year to mitigate recession. Unfortunately that fairy tale implies a 5% Fed Funds rate by the end of 2022 from 1.5% today. There has never been a recovery from recession at anything less than a 5% Fed rate EXCEPT the pandemic which required fiscal and monetary QE at a combined level of 15% of GDP. Yes, you read that right.

NONE of which risk is priced into stocks right now. What IS priced into the stock market is a soft landing. In a run of the mill recession, stocks decline 20% which is where they are now. In a deleveraging recession such as 2000 and 2007, stocks decline 50% or more.

Which means that what we've seen so far in markets is the denial phase. Which will be followed by the investor panic phase. And finally the Fed panic phase.

One other UNPRECEDENTED risk that NO ONE mentions is that regardless of investor sentiment and Fed rate hikes, the Fed will be draining liquidity at record levels for the indefinite future via Quantitative Tightening.

Never mentioned.

Now, consider the fact that the U.S. is doing better than the rest of the world. Europe, China, and Emerging Markets are imploding in real-time.

And there's your bull shit market. If that's your thing.

"As the endgame approaches, those still nominally in charge of the collapsing empire resort to all sorts of desperate measures—all except one: they will refuse to ever consider the fact that their imperial superpower is at an end, and that they should change their ways accordingly...Because, you see, if they had an inkling of what's going on, they wouldn't take their jobs seriously enough to keep the game going for as long as possible."

I've been too bullish. Like many investors, far too focused on markets. What's happening under the surface of the Disney markets is far more dire than what's happening on top. This "Everything" bubble is a multi-pronged attack on the middle class. We are witnessing the final meltdown of the U.S. middle class at the zero bound.

The greatest risk isn't even currently acknowledged by anyone in the mainstream media - monetary policy failure at the zero bound. This Volcker gambit has no chance of succeeding. Not only does it wrongly assume the Fed will have sufficient rate cut powder it ALSO ASSUMES the middle class is as strong now as it was in 1980 when the middle class was at its apex of power. Whereas, now the U.S. middle class is at the lowest share of GDP in history. No unions, no labor protections, no pension plans, no job security. All strip mined and fed into the stock market and out to the Cayman Islands. A multi-decade crime spree capped off by a COVID-driven monetary sugar rally. Because we are to believe a pandemic improved the economy.

This belief in the enduring strength of the serially laid off and underemployed "consumer" is the greatest fantasy underlying this era. The magnitude of this disaster far exceeds the ability of central banks to "fix" when it explodes. Ironically, the stock market's durability to date has been covering up the carnage taking place below the surface. As is end of cycle inflation. Sales VOLUMES are collapsing, but prices are staying high. For now. This is how every bubble crash begins - buyers and sellers move further apart. At first sellers are reluctant to lower their asking prices. But then the market slows down to a point at which they have to sell. And then the race to the bottom begins.

I call this period the apex of criminality. The full weight of super cycle criminality is now arrayed against the general public. From the S&L Crisis in 1990 to the DotCom bubble in 2000, the housing bubble in 2007, and on to now, we have witnessed serially greater widely accepted corruption in financial markets. Bernie Madoff's Ponzi scheme was a rounding error compared to the losses in Ponzi crypto markets - less than one hundredth in size. And yet there is STILL no regulation around Crypto currencies. It's fucking ridiculous. However, on an even larger scale albeit more insidious, today's economic "soft landing" predictions are totally driven by conflict of interest. No one on Wall Street wants to be outside of the consensus. On Wall Street, the people who make these forecasts are called "the sell side". And the people who are to believe these predictions are "the buy side". Except Wall Street doesn't believe their own hyperbolic bullshit, which is why THEY are all sitting in cash right now. Not their clients however.

Throughout this time, the public has come to believe that all of this is now just "corruption as usual". Robert Prechter of Elliot Wave International informs us that ignoring and embracing malfeasance is common in boom times. However, when boom turns to bust, social mood turns dark and what was generally accepted during the good times is generally rejected during bad times.

Given that there were NO major prosecutions on Wall Street arising from the 2008 subprime meltdown, this time we will see a level of public rage that is hard to fathom. Basically, the industry that got bailed out by the middle class in 2008 is the one that is now leading to their final destruction.

History will not be kind.

From a markets standpoint, getting the T-bond market and the stock market under control will be the Fed's top priority. However, in the meantime, most other markets will collapse to levels currently unthinkable - I am of course referring to cryptos, housing, commodities, muni bonds, corporates and Emerging Markets.

When that happens, confidence will collapse like a cheap tent.

Even zombified down -60% the stock market will in no way convey the full extent of the economic damage.

Ultimately there will be far more "value" in other types of investments than the ones directly manipulated by the Fed. When the BOJ zombified the Japanese stock market, the public abandoned it en masse. They found far greater value in markets that were not manipulated by central planners.

In summary, the contrarian view at this juncture is NOT for a rally. The contrarian view is for monetary failure at the zero bound.

And no, they don't see it coming.

To today's experts now looking in the rearview mirror, this is a "six sigma" Black Swan event that is outside of their purview. Their entire baseline is wrong.

NOTE: Past performance is no guarantee of future results.

At times like this, what everyone wants to know is "How soon is inevitable?"...

So far, this year is evolving eerily similar to 2008. The year started with inflationary hysteria, and it's ending with unforeseen deflationary collapse. Then as now, forecasters were continually behind the curve. Their predictions were outdated the moment they were printed. What follows is a comparison of 2008 risks vs. now:

First, on a relative comparison of this monetary asset bubble. Put it this way, Crypto losses in 2022 are MORE than the entire size of the subprime mortgage market equaled in 2007: $2.15 trillion vs. $1.3 trillion.

The size of the 2021 IPO market in total IPO count and subsequent collapse is vastly larger than every other year in market history including Y2K.

Which is why this week when we learned that Goldman Sachs "beat" earnings expectations, that meant their profits DECLINED -48% year over year. Following their own standard Wall Street model of lowering earnings expectations so it always looks as if companies are beating expectations even when profits are collapsing.

Criminality is built right into the standard valuation model.

And of course the current housing bubble features the largest two year price increase in U.S. market history. By any valuation measure - price/income, price/rent, price/CPI this bubble is larger than the one in 2007.

Not just in the U.S. but across the developed markets world (Europe, Canada, Australia) are all RECORD overpriced with central banks RECORD tightening.

I've been writing a lot about policy error lately so I will give the summarized version now. It's shocking to me that not one pundit has raised the risks of the Volcker gambit taking place right now. That is by FAR the greatest risk in conjunction with Fed-induced EM meltdown.

"The odds of a 1 percentage point hike were at 83% early Thursday, but later dropped to about 45% following comments from Fed Governor Christopher Waller:

"We don't want to make snap policy decision based on some knee-jerk reaction to what happened in the CPI report"

That's EXACTLY what they did last month. The CPI report came out on the Friday before FOMC, and they leaked to the WSJ a .75% rate hike over the weekend. They totally panicked.

However, instead of Fed-induced depression all we hear from pundits (and the Fed) now is that rates will go up this year and down next year. And it will all end in a "soft landing".

By the way, we were told the same thing back in 2008:

Which gets us to the related topic of recession denial which today has reached epic levels. Wall Street is going to bury a lot of people, which is what they do best.

"The current recession exists purely in the imagination, not in the real world"

The Fed as always is laser focused on stale data months old at this time. They are totally ignoring the bond market and the flattened yield curve. The difference between now and 2008 is that year over year CPI "inflation" is higher now than it was back then. However, nominal prices of commodities are LOWER now than they were back then. Either way, it's the same result. Far more focus on inflation than recession.

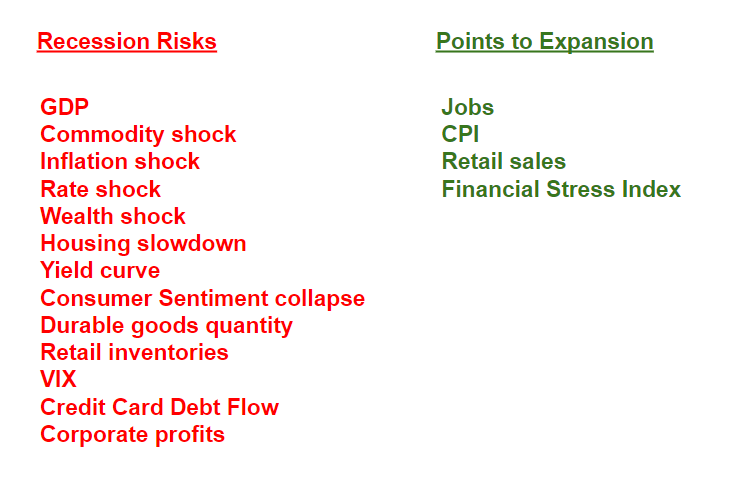

I put together this comparison list of current factors pointing to recession vs. factors currently pointing to expansion. What you notice is that the expansion list is mostly comprised of lagging indicators. Whereas the recession list is driven by real-time market indicators. Except GDP, which forms the very basis of economic growth and is likely ALREADY in confirmed recession. In other words today's experts are ignoring their OWN definition of recession as I write. Similar to 2008 when the economy entered recession NINE months prior to Lehman. But the Fed thought the economy was still growing.

One big difference between now and 2008, is that back then the banking dominoes were already falling - New Century Financial, Bear Stearns, Countrywide, Washington Mutual, Fannie/Freddy, AIG etc. etc.

This time, the dominoes are sovereign nations. Led by Russia and China. China pulled the WORLD out of recession in 2008, this time around they are leading the world into recession.

Ironically, COVID started in China and they are handling this crisis worse than every other country on the planet. They are STILL in lockdown mode two years later. The wealthy are leaving China like rats on a sinking ship:

"Scarred by Shanghai’s chaotic lockdown under the Covid-Zero policy that has made China a global outlier, Hu is joining what investment migration consultancy Henley & Partners estimates is a cohort of 10,000 high-net-worth residents seeking to pull $48 billion from China this year — the second-largest predicted wealth and people outflow for a country after Russia"

China's GDP growth rate is now predicted to be 3.4%, however it has been a moving (lower) target all year. Similar to the U.S., crash is happening faster than analysts can change their models.

Which gets us to positioning. We learned this week that professional fund managers are the most bearish since 2008. Which, we are to believe is bullish because it means they have "capitulated". The term everyone is using.

The problem of course is that there is now a massive divergence between Wall Street and Main Street. The latter of which has remained far too complacent and over-positioned in stocks:

Final bagholder transfer of ownership is now complete.

A necessary and sufficient condition for final collapse.

In summary, the S&P 500 peaked in October 2007 and then exploded a year later in October 2008.

This past year, the S&P peaked in December 2021. Therefore, if anything this current disaster is AHEAD of schedule.

But, you don't see headlines like this one at the bottom, you see this at the top. Because that's what this is, the second denialistic top prior to the second and bigger crash.

Deja vu.

“We have seen very robust, significant activity for about the last 18 months that’s continuing here into the third quarter. So, really a record sales run for us”