Ahead of near certain 4x tightening of liquidity at both ends of the yield curve AND the fastest bond crash in world history, the Fed stress index is STILL NEGATIVE.

Does anyone really believe the Fed will double tighten on the long end and the short end at the same time in two weeks? Of course, all the zombies do, but given the Fed's proven skill at imploding markets, some amount of caution may be in order. Fed tightening has preceded every recession since WWII. There were only a handful of times the Fed tightened and it DIDN'T cause recession and so therefore this clearly is one of THOSE times again.

As I pointed out on Twitter, global markets have crashed ahead of the last four FOMCs. Similar to January, we are now in the earnings blackout period which means no stock buybacks. And we are soon entering the Fed blackout period which means no more Fedspeak.

I've been fairly reticent lately as my rage has been subsiding the closer we get to the inevitable explosion. For the zombies unfortunately, it will be the exact opposite. A very rude awakening from their narcoleptic coma, followed by mass rage on a scale I am not adequately describing right now.

One could not possibly envision a set of circumstances more dire than these ones: Non-stop hysteria over rising prices, followed by a collapse in EVERYTHING at the same time. And then global credit crisis.

Below, in this chart we see via banks and U.S. total debt that the cycle was ending prior to the pandemic. However, the epic pandemic stimulus tacked on two more years of debt-fueled mass consumption:

The Fed is at the furthest policy extreme from market bailout, in HISTORY:

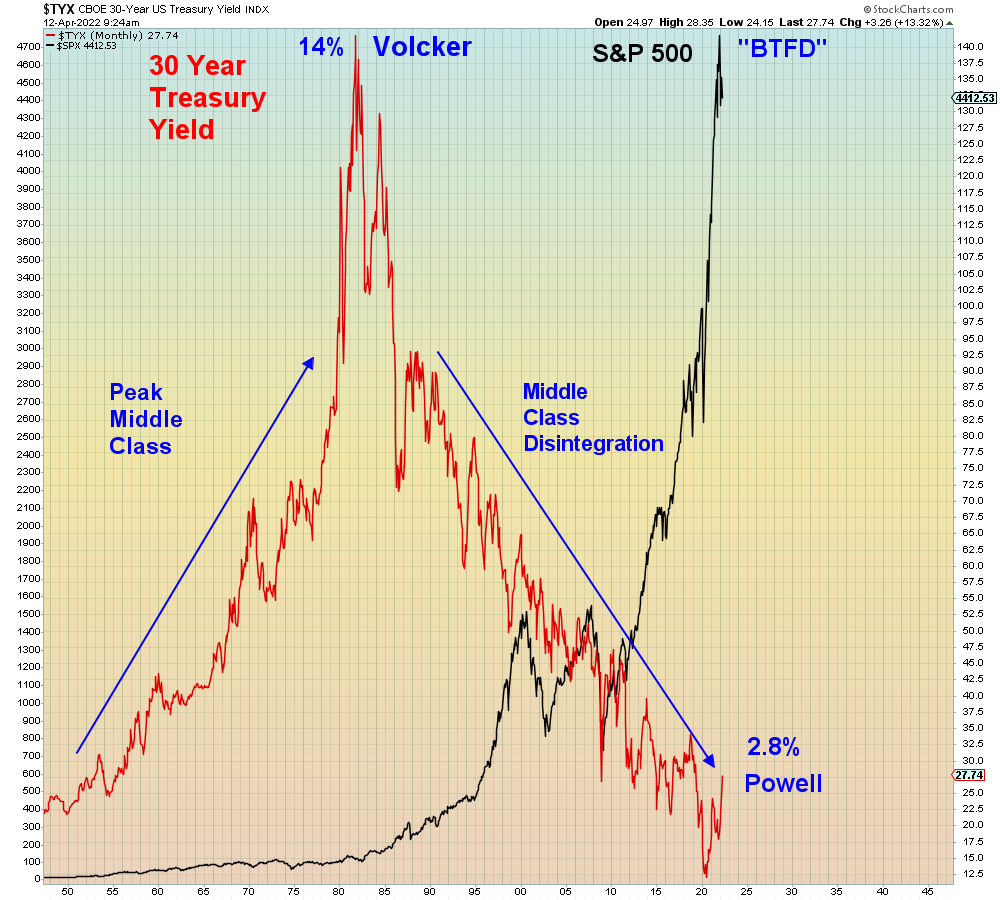

What can you say about a society that NEVER learns that cheap debt is dangerous? What can you say about policy-makers always incentivizing the masses to borrow as much money as possible ahead of recession? First they tell people that prices can only go up and then they bury them under a mountain of debt.

AGAIN.

Recall that Fed chief Greenspan exhorted borrowers to take out Adjustable Rate Mortgates (ARMs) in 2004 and then he raised interest rates 17 times in a row. Everyone who took his advice got financially obliterated.

This is the ZERO bound version of 2008. The one in which the Fed can't lower rates from 5.25% to zero. And therefore the one in which bailouts fail and the losses fall where they may.

Which will be a rude awakening for the bailout class to be sure.

In summary, we are living in Disney World now. The masses have been thankfully relieved of the burden of reality, as they receive their daily infotainment enema via subscription delivery. One thing that BOTH the left and right have mastered is mind control.

To date, the herd has been the inertia behind this slow motion disaster. Unfortunately, no amount of bullshit can protect them from what comes next. Which is why I plan to keep a safe distance when their Disneyfied illusion collapses. Because they will quickly come to realize they have emulated personal failure and they have perfected a dead end way of life.

Above all else, the thundering herd believes in the strength of numbers. They deem what is "right and wrong" solely based upon what other people are doing. And in doing so they have sacrificed their mental health at the altar of competitive conformity and consumption addiction.

They will soon learn that some things should never be sold.