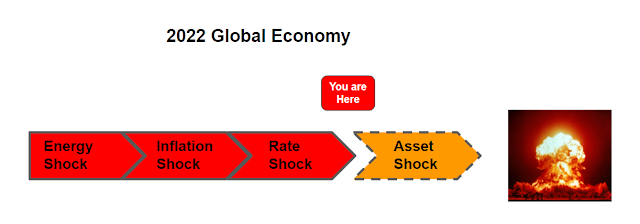

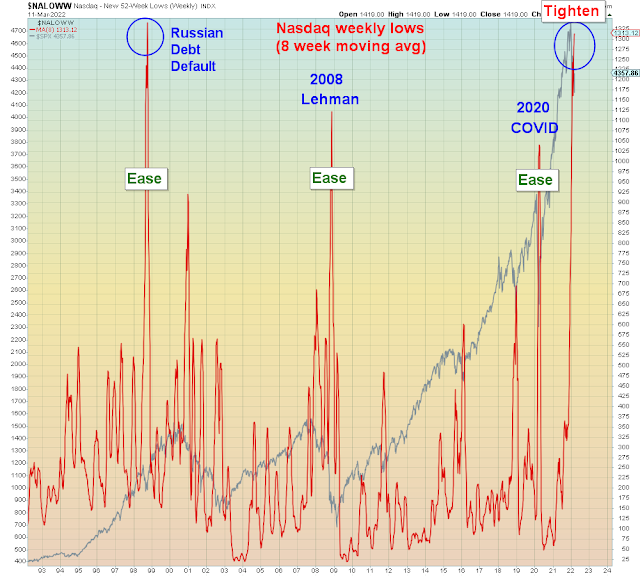

What we are witnessing is a commodity driven liquidity collapse. Higher oil and commodity prices are forcing the Fed to accelerate their tightening plans. Of course they are using the wrong tool for the wrong problem. Rate hikes are a demand side solution, whereas the sanctions-driven commodity shortage is a supply side problem. The end result of this failed gambit will be a demand collapse in conjunction with a global supply glut. This is total economic mismanagement driven by the ubiquitous assumption that markets won't rationally respond to inflated prices. The overwhelming consensus at this latent juncture is that prices of everything, especially risk assets will keep climbing while the Fed tightens liquidity at the fastest pace in decades. Where this is all headed is inevitable deflationary asset collapse as illustrated below:

"Whipsawing commodity prices and eye-watering margin calls are forcing traders to reduce their activity, driving liquidity out of markets and exacerbating price swings, according to some of the world's biggest trading houses."

Consumers are now getting squeezed from every direction: Durable goods, home prices, interest rates, food prices, car prices, commodity prices. Today's pundits should know better than to believe in this mass delusion. Sustained inflation is always and everywhere a monetary phenomenon and yet the Fed is now tightening as fast as possible. Supply side "inflation" in a rate hiking cycle is not sustainable.

Unfortunately, there is no one to warn the sheeple because the prospect of a global deflationary asset crash is not an option. It's not something that today's pundits could even mention since they would have an exodus of subscribers. What we have instead is mass groupthink on a record scale.

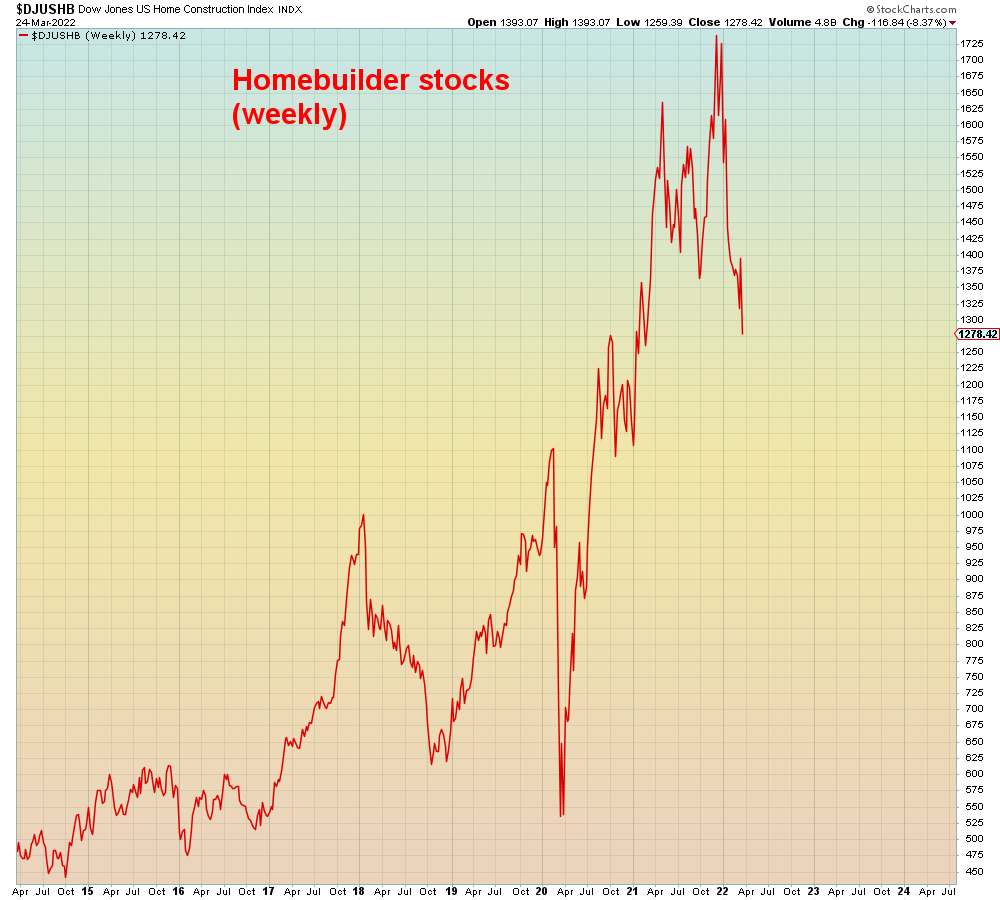

Exhibit A of impending disaster is today's over-heated housing market. Home prices in my neighborhood have gone up 30% in just the past year alone. These sky-rocketing home prices are causing massive distortions in supply and demand. Buyers have been told that home prices and mortgage rates can only go higher, so they are panic buying homes. Demand has been further accelerated by so-called robo buyers. These are hedge funds that are buying up homes across the country and packaging them into collateralized debt obligations (CDOs) in a repeat of the 2008 housing crisis. Except instead of packaging the mortgages, they are packaging rental properties.

For their part home builders are responding rationally by building as many homes as possible to meet "demand". All of which is creating the perfect conditions for a massive end-of-cycle supply/demand mismatch.

In summary, the conditions are now in place to create human history's biggest supply glut. Industry desperately wants us to keep buying and pretend it can't happen. The purpose of the stagflationary hypothesis is to convince as many people as possible that these prices will continue rising forever. Unfortunately, an inflationary consumption binge followed by a deflationary asset collapse is the worst case scenario for the economy.

It should come as no surprise that the "stagflationary" 1970s was followed by the biggest recession in post-WWII history in 1980. When newly appointed Fed Chairman Paul Volcker pulled the plug on inflation, it was called the "Saturday Night Massacre". Ironically, today's amnesiacs who believe this is the 1970s all over again, are creating the same deep recessionary conditions - this time in a liquidity trapped environment where interest rates can't go lower. How do you incentivize people to buy homes and big ticket items if the cost of debt in real yield terms is sky-rocketing?

You don't. Which means last ones out, don't get out.